Wall Street enters the last Monday of the month, which also marks the start of a week characterized by elevated market sensitivity. At the same time, three key factors are converging: the geopolitical situation involving Iran, expectations for earnings from the largest technology companies, and Wednesday’s Federal Reserve meeting. Such a combination typically does not create a single dominant market driver, but rather an environment where markets react more quickly to incoming information and show significantly lower tolerance for deviations between expectations and actual data.

The most immediate factor remains the situation around Iran, where reports suggest possible attempts at de-escalating tensions. Media coverage points to proposals that could include a temporary easing of the conflict and postponing more direct nuclear negotiations in exchange for opening the Strait of Hormuz. Any signal of stabilization or escalation has a direct impact on commodity prices and overall geopolitical risk sentiment, translating into short-term moves across financial markets.

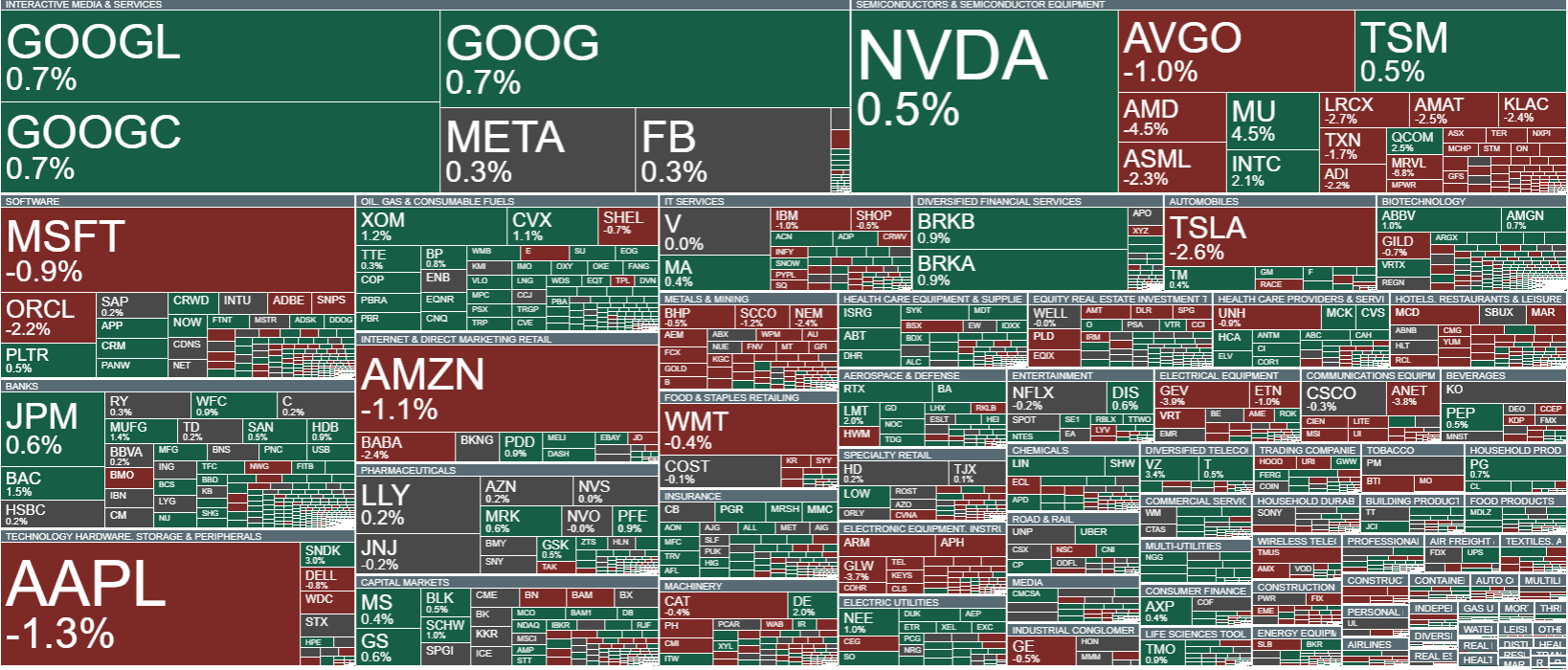

The second key focus is earnings from the largest technology companies, which currently act as the main driver of equity market sentiment. This week, results will be reported by Microsoft, Meta, Amazon, and Google. Expectations for the sector are extremely high, as investors are no longer focused solely on earnings beats, but primarily on whether the scale of growth confirms the artificial intelligence narrative. According to consensus, the technology sector is expected to deliver very strong profit growth, significantly outperforming the broader market, alongside continued revenue expansion and margin improvement, despite massive investment spending in AI infrastructure. In such an environment, even solid results may not be enough if they fail to match elevated expectations, while any disappointment could trigger sharp valuation adjustments.

The third major factor shaping sentiment is Wednesday’s Federal Reserve meeting. Fed decisions and communications have a direct impact on global financial conditions, as they determine the cost of capital and expectations for future monetary policy. The key question at this stage is whether the central bank will maintain a cautious stance on inflation and economic growth or signal greater flexibility going forward. For the technology sector, which is highly sensitive to interest rates, even subtle changes in tone can have a meaningful impact on valuations.

Overall, this creates a week in which three independent forces are acting simultaneously on markets. On one hand, geopolitical risk related to Iran influences commodity prices and overall risk appetite. On the other hand, the earnings season for major technology companies tests the credibility of the artificial intelligence growth narrative. The third component is Federal Reserve policy, which shapes global asset pricing through the cost of money. In such an environment, markets are unlikely to move in a single direction and instead react dynamically to shifting expectations, with volatility driven more by interpretation of information than by the data itself.

Source: xStation5

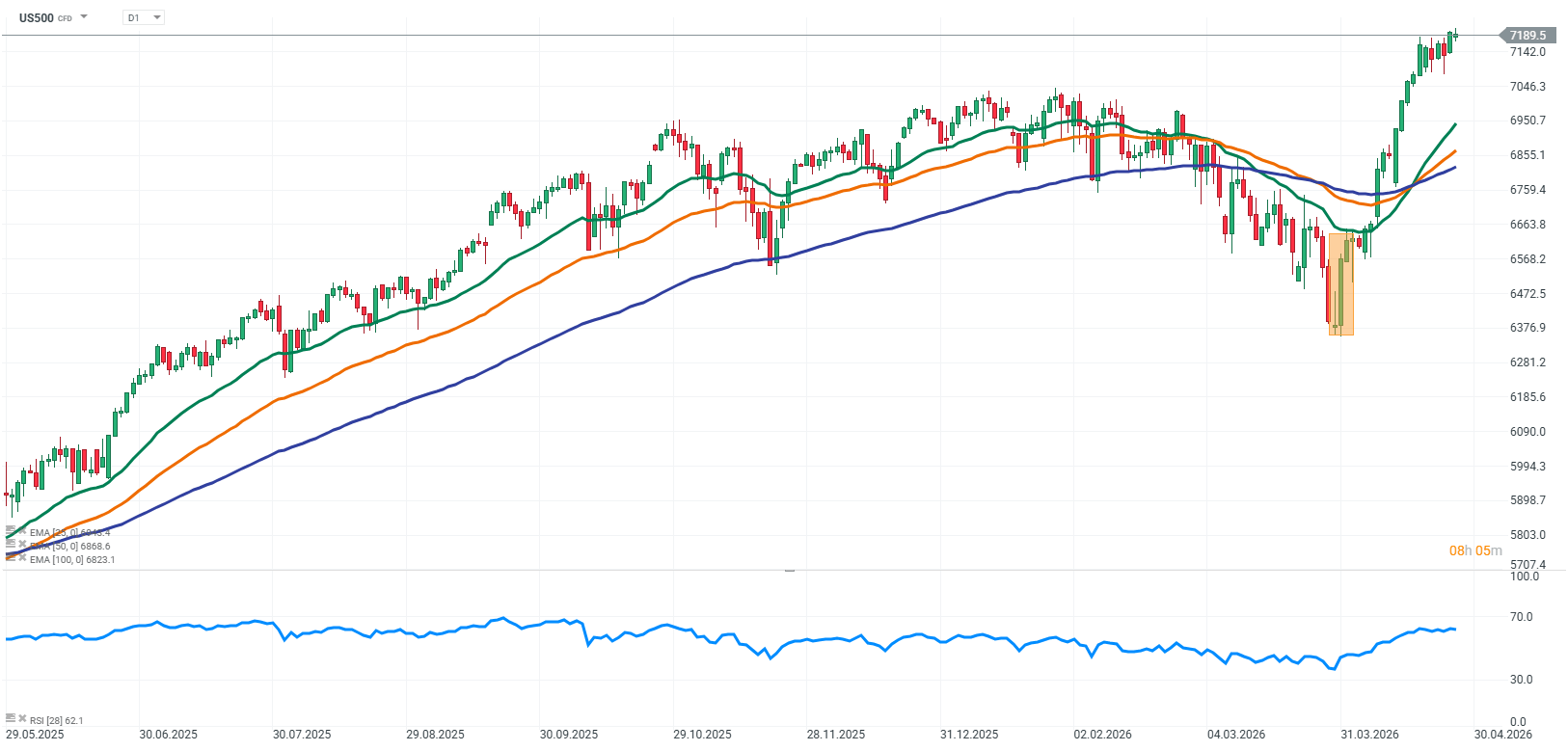

US 500 futures are trading slightly lower today, with markets showing caution despite a relatively strong earnings season that continues to support a broadly positive equity backdrop. Investors are modestly reducing exposure ahead of Wednesday, when results from major technology companies such as Microsoft, Meta, Amazon, and Google will be released, alongside the Federal Reserve decision. As a result, a wait and see attitude dominates, and short term sentiment remains slightly defensive.

Source: xStation5

Company news

Microsoft (MSFT.US) is declining after reports that OpenAI is restructuring its partnership terms and that Microsoft will no longer receive a revenue sharing agreement from OpenAI’s business. Previously, this arrangement was one of the key financial benefits Microsoft derived from OpenAI’s growth. The market interpreted this as a partial reduction in the direct financial upside Microsoft receives from the artificial intelligence boom, even though the overall partnership between the companies remains very close.

Domino’s Pizza (DPZ.US) is falling after first quarter 2026 results disappointed mainly in comparable same store sales, which came in below market expectations. The reading was interpreted as a sign of weaker consumer demand. The biggest disappointment came from the US market, alongside slightly softer international performance.

Verizon (VZ.US) is rising after surprising the market with net positive wireless subscriber additions. In Q1 2026, the company added around 55,000 postpaid subscribers versus expectations for a decline. Verizon also raised its full year 2026 earnings guidance, which investors interpreted as a sign of improving operational trends and effective promotional strategy.

Supermicro (SMCI.US) is announcing the opening of its largest campus to date in Silicon Valley, designed to accelerate delivery of next generation AI data center infrastructure. The expansion is expected to significantly increase the company’s production and integration capacity in servers and AI systems.

Alphabet (GOOGL.US) is in focus after reports that it may cooperate with MediaTek on the production of 8th generation TPU chips.

Daily Summary: Semiconductors Rise in the Shadow of Geopolitical Turmoil

Did SaaS lost too much? Morgan Stanley says yes.

Tech sector catches its breath 🚀

Red Sea, but not the indices : The effects of the Bab al-Mandab blockade.

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.