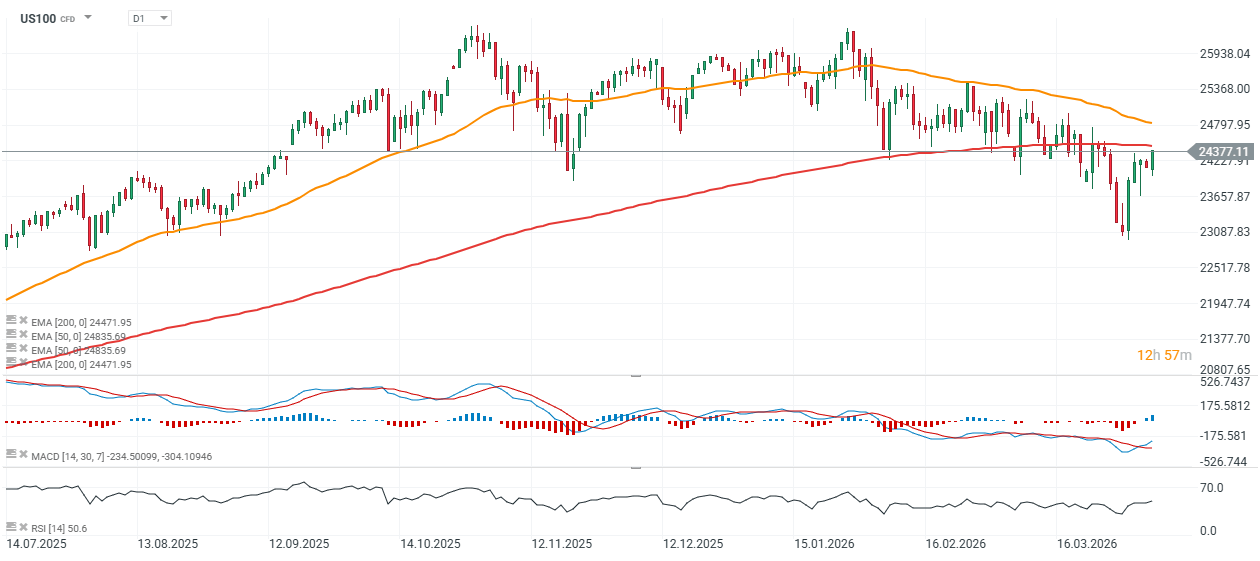

Nasdaq 100 futures (US100) are up more than 1% today, trading at their highest level since March 26, around 24,380 points. The benchmark is gaining after media reports indicated that Iran is engaged in negotiations over a potential 45-day ceasefire in the Middle East.

- According to Reuters sources, Iran has rejected a proposal to reopen the Strait of Hormuz in exchange for a ceasefire and has refused to comply with any imposed deadlines or negotiate under pressure. At the same time, sentiment on Wall Street appears to be gradually stabilizing, largely driven by expectations of a constructive outcome from Washington–Tehran negotiations, potentially leading to the reopening of tanker traffic.

- Donald Trump set a deadline of 2:00 AM CET for either de-escalation or significant strikes on Iranian infrastructure. So far, both sides appear to maintain relatively hardline negotiating positions. Iran has also threatened retaliatory attacks on infrastructure across the Middle East, including assets linked to the United States.

- Meanwhile, Citrini released a report suggesting that the datasets used in macro and oil market analysis may overlook a substantial portion of actual tanker traffic through the Strait of Hormuz. According to the report, many vessels operate with transponders switched off or deliberately misreport their data.

- Brent crude has declined from around $112 per barrel at the start of Monday’s session to below $108 in the late morning, indicating a partial unwinding of the geopolitical risk premium.

What to expect from the ISM data?

Beyond geopolitics, investor attention is shifting toward US ISM Services data, scheduled for release at 3 PM GMT. February’s ISM reading was the highest since 2022, suggesting that exceeding the previous print may be challenging given the Middle East conflict and rising energy costs.

- 16:00 CET – US ISM Services (March): expected 54.9 vs. 56.1 previously

- Prices Index: expected 67 vs. 63 previously

- New Orders: expected 56.8 vs. 58.6 previously

- Employment: expected 51.0 vs. 51.6 previously

A notable increase in the prices sub-index is expected. The greater the divergence between prices and components such as new orders or employment, the more credible the risk of a stagflationary environment becomes. Elevated fuel prices reduce disposable income, a dynamic historically associated with corrections or bear markets.

Importantly, the prices sub-index does not directly feed into the composite ISM figure, which may increase the likelihood of a larger month-on-month correction in the headline index. On the other hand, a sharp decline appears less likely given stronger-than-expected regional data from the Dallas Fed, Philly Fed, Empire State, Richmond Fed, and Kansas City Fed.

US100 (D1 timeframe)

Source: xStation5

Daily summary: Sense of relief to global markets🎢 OIL prices dip 8%🚨

BREAKING: US ISM Manufacturing - Strong Beat Across the Board

Eurozone PMIs: German Factory Revival Masks Underlying Stagnation 🇪🇺

Wall Street rebounds as Q2 earnings season significantly exceeds investors expectations

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.