The Japanese yen is starting the new trading week with significant gains. The reason behind the JPY euphoria today is the better-than-expected GDP data, which came in well above market expectations. Indicators of Japan’s economic strength signal upcoming changes in monetary policy, which is expected to be further tightened. At the same time, the U.S. dollar has shown remarkable weakness in recent days.

Yen reacts to GDP and easing trade war concerns

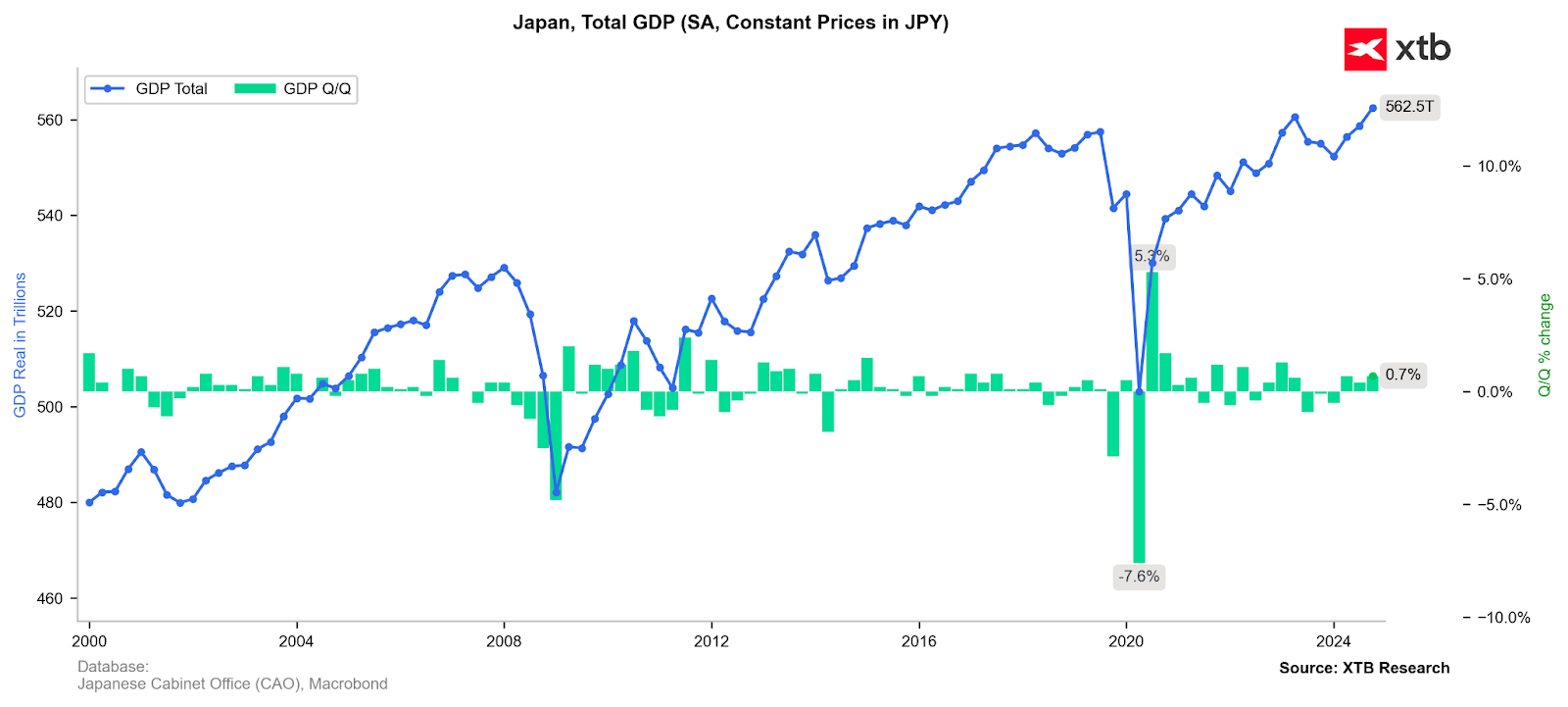

Japan’s GDP grew by 2.8% YoY in Q4 2024, exceeding the 1% forecast and up from 1.7% in Q3 2024. Seasonally adjusted annual growth stood at 1.2% YoY, beating expectations of 0.6%. Quarter-over-quarter growth reached 0.7%, up from 0.4% previously, and well above the 0.3% forecast. Strong GDP figures ahead of the spring wage negotiations could encourage the Bank of Japan to take a more hawkish stance.

- At the same time, investors are increasingly convinced that the threats of a trade war and high tariffs from the new U.S. administration are more of a negotiating tactic rather than a real policy shift as signaled by Republicans and Donald Trump before the U.S. elections.

- Last Friday’s higher-than-expected CPI and PPI data from the U.S. was balanced by the weakest retail sales report since 2020, which unexpectedly plunged by -0.9% MoM in January.

- The market has shifted expectations for the first Fed rate cut from December to September 2024, and the probability of a rate hike this year has become nearly improbable—a stark contrast to just two weeks ago when markets priced in over a 20% chance of a hike, at the peak of trade war fears.

Statements from Fed officials, including Michelle Bowman and Patrick Harker, indicate a cautious approach, with no expected rate cuts in the first two quarters of 2024. However, neither of them has ruled out a rate cut later in the year, instead emphasizing the potential for inflation to decline in the coming quarters, even amid persistently high wage growth and a slightly weaker labor market.

Japan’s Gross Domestic Product (GDP) has long been burdened by weak consumption and a shrinking labor force due to an aging population. However, today’s Q4 2024 data has raised hopes that stagnation may be ending.

-

Annualized GDP unexpectedly surged to 2.8% (forecast: 1.1%, previous: 1.7%).

- Quarter-on-quarter GDP growth reached 0.7% (forecast: 0.3%, previous: 0.4%).

- The main driver of economic improvement was strong capital expenditures by businesses, which significantly increased investments.

- Private consumption also surprised to the upside, rising 0.1%, despite expectations of a 0.3% decline, signaling the first signs of consumer relief after a record inflation surge.

Source: XTB Research

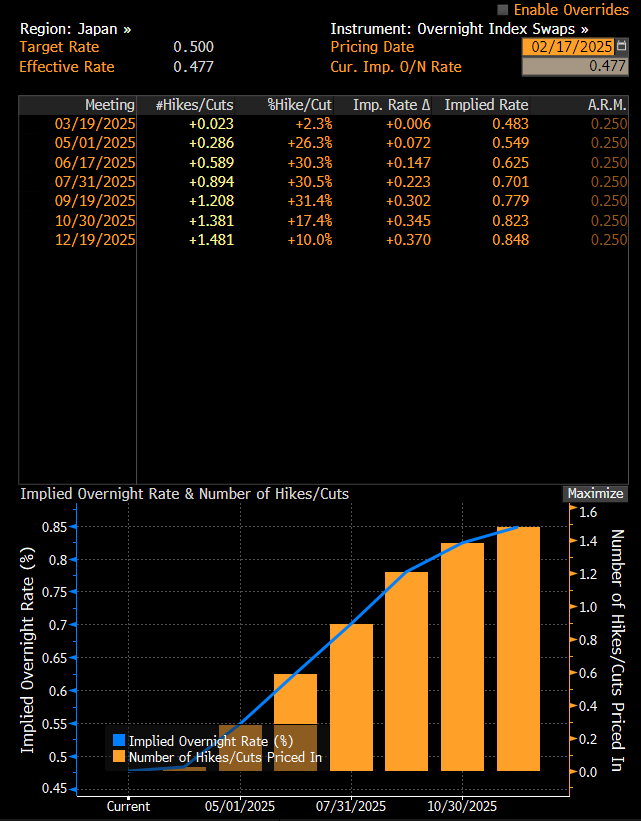

Such a major surprise in GDP figures has led the market to price in earlier rate hikes in Japan, supporting the Japanese yen. Source: Bloomberg Financial LP

Interestingly, however, the options market did not anticipate a decline in USDJPY. A one-month risk reversal hedging strategy even indicated the possibility of a USDJPY rebound. Source: Bloomberg Financial LP

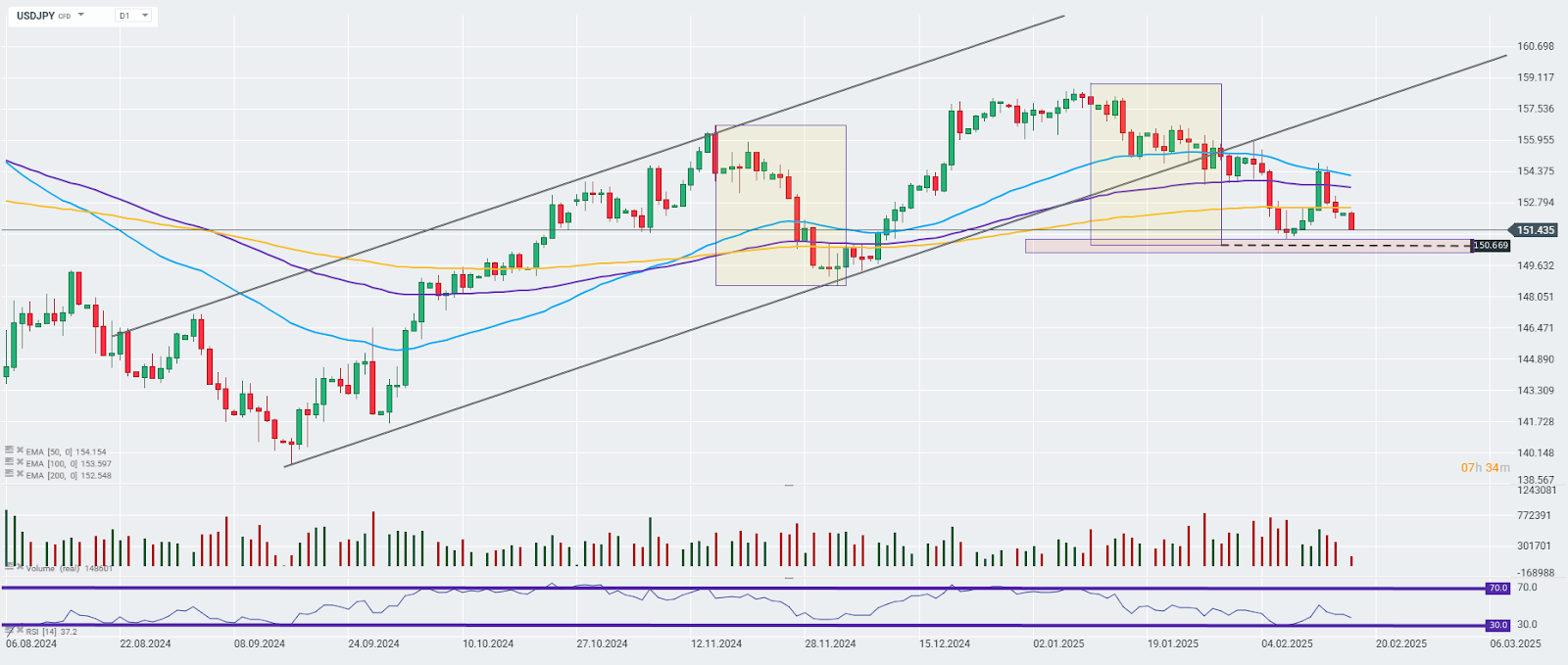

USDJPY Chart

The USDJPY pair is deepening its corrective decline, approaching a critical support zone, which aligns with:

- The local low from February 7

- The lower boundary of the 1:1 decline from November 2024

While the risk of a renewed inflation surge in the U.S. remains, the USDJPY pair is currently reflecting short-term dynamics, suggesting that a rate hike in Japan appears far more likely this year than in the U.S.. As a result, bond yield spreads between the two countries may begin to reverse their long-term trend. Today’s decline stalled at the 38.2% Fibonacci retracement level.

Source: xStation5

Source: xStation5

BREAKING: Eurozone recovery? Positive PMI data tempered by high oil and gas prices

Economic Calendar: Industry’s condition in the shadow of oil prices

Daily Summary: Trump's War Threats Weigh on Markets. Wall Street Sinks into the Red

Economic Calendar: Time for Tesla and Google Earnings (22.07.2026)

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.