Monetary Policy and Trade Wars

US interest rates have remained unchanged for an extended period, a situation not expected to shift before September. A slightly higher US inflation reading, increasingly reflecting the impact of tariffs, is dimming prospects for more aggressive rate cuts in the United States, despite pressure from the Trump administration on the Federal Reserve. Conversely, Japan shows no immediate signs of rate hikes. Furthermore, the risk of stagflation in Japan is growing, particularly with the imposition of 25% tariffs by the United States.

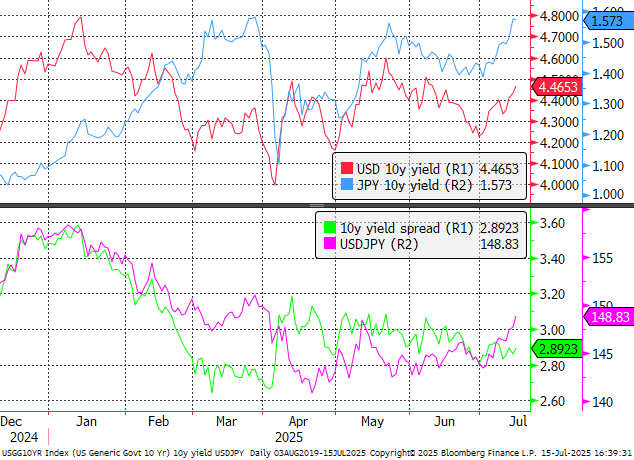

While Japanese yields are rising, this is not due to expectations of higher rates but rather diminishing confidence in the country's fiscal stability. In contrast, US yields are increasing due to the lack of near-term rate cut prospects. The yield spread has recently stabilized. Source: Bloomberg Finance LP

It is worth noting that Japan recently announced a stimulus package of ¥900 billion, which will significantly increase borrowing needs and could threaten fiscal stability. Trump's tariffs are also expected to exert pressure for a weaker yen, aiming to boost the competitiveness of Japanese exports.

Investors Withdraw from the Yen

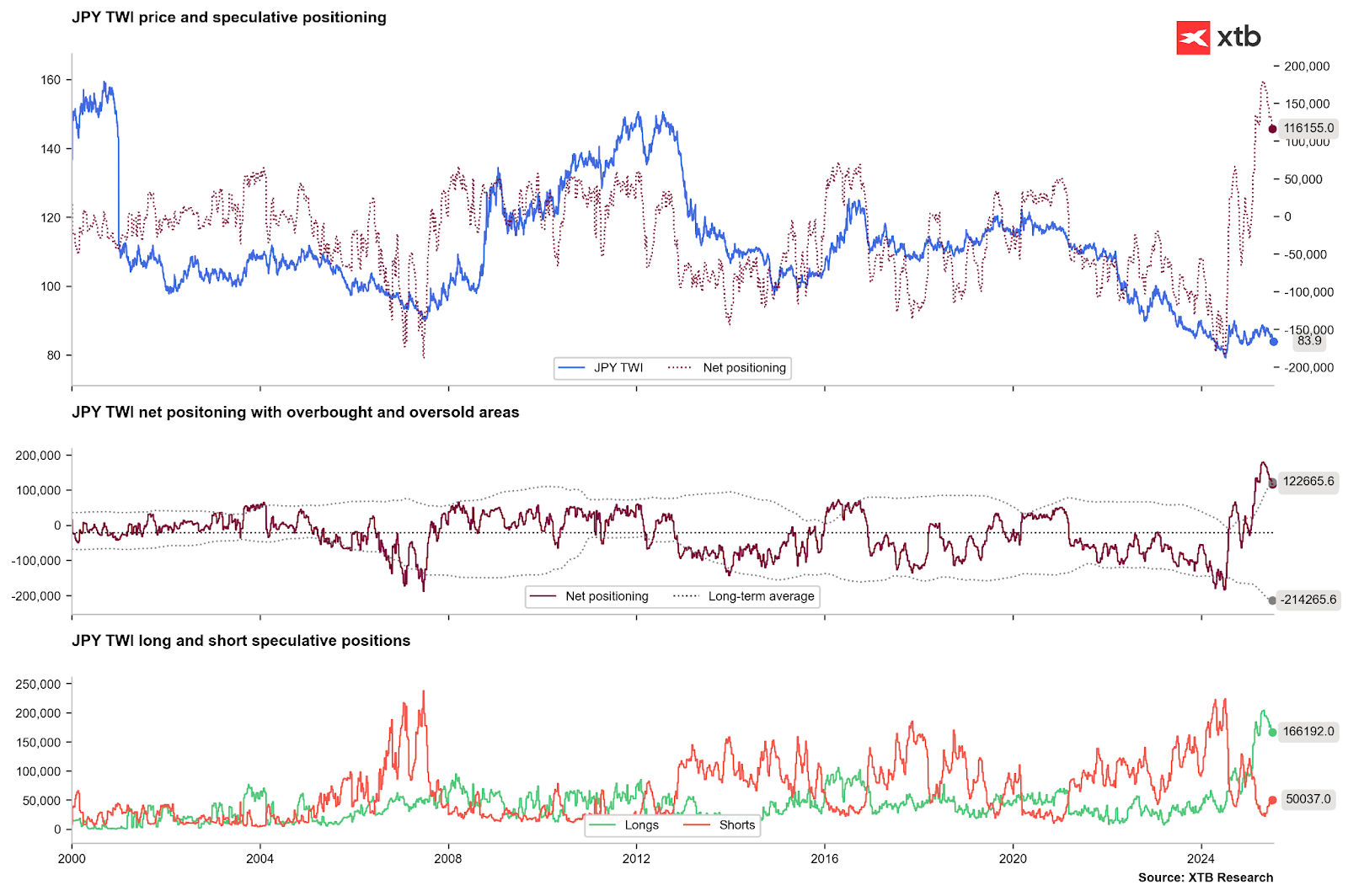

Amidst a reversal from the US dollar and in anticipation of Fed rate hikes, we observed a record increase in long positions on the yen. It also appeared that investors would close carry-trade transactions at an unprecedented pace. Recently, however, there has likely been a return to borrowing in yen, especially in anticipation of its weakness.

There has been a clear reversal of long positions and an increase in short positions. Source: Bloomberg Finance LP, XTB

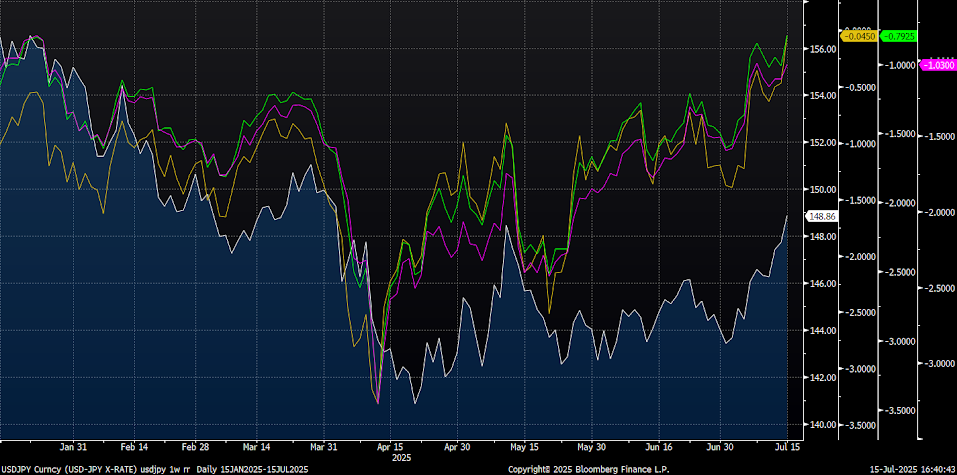

We are also observing a significant shift in the options market. The difference between out-of-the-money (OTM) call and put options is rising to its highest level since 2022. Currently, the price advantage of put options is only marginal. Similar movements were observed in 2022 when the pair experienced very strong gains. Source: Bloomberg Finance LP

Technical Outlook

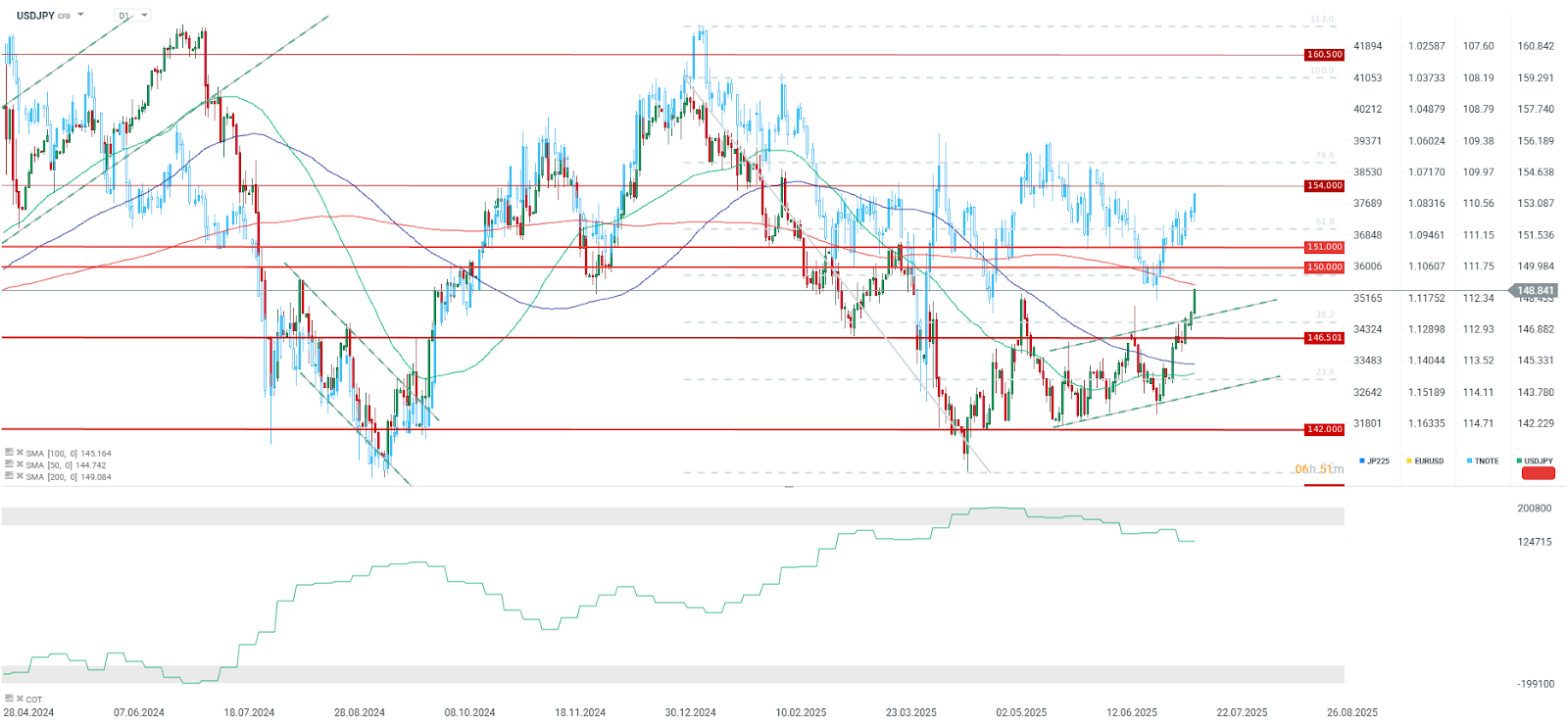

The USDJPY pair is experiencing its third consecutive strongly bullish session, approaching the 149 level and the 200-period moving average, which was last breached in March. Since the beginning of the month, the pair has already surged by 3.5%. The target for the pair, given the current upward momentum, could be the zone between 150 and 151. However, it is important to note that the yen also faces risk from the upper house parliamentary elections this coming Sunday. If yen weakness were to persist, the 155-160 range, where the Bank of Japan last intervened, would be a key area to watch. Conversely, if a pullback were to occur, support is located at the 38.2 Fibonacci retracement level of 147.3.

Economic Calendar: Will NFP Move the Market? (07.08.2026)

Morning Wrap: Oil Rises Again (07.08.2026)

Wheat extends correction, falls to its lowest level since July 10 🚩 Drought, El Niño and the Black Sea in focus

📉 Natural gas tumbles as US EIA inventories rise

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.