Wheat prices have risen for a third consecutive session after the U.S. Department of Agriculture (USDA) downgraded its outlook for the market in response to the deteriorating condition of U.S. winter wheat crops. The key question for investors is whether weaker U.S. supply can provide lasting support for wheat futures.

The USDA forecasts that U.S. farmers will harvest just 32.1 million acres of wheat in 2026, marking the smallest harvested area in 149 years and the lowest since 1877. Wheat futures have climbed to around $6.00 per bushel since the beginning of July, rebounding from a nearly four-month low reached on June 29 after USDA reports showed lower wheat inventories and a smaller planted area.

The USDA also reported that U.S. wheat stocks totaled 920 million bushels as of June 1, below market expectations. Between February and April, oil prices increased by 58% while fertilizer prices surged by 66%, significantly raising agricultural production costs and providing additional support for wheat prices.

A key date for the market is August 21, when the 60-day suspension of certain sanctions on Iran expires. Failure to reach a lasting agreement could once again increase the risk of disruptions in the Strait of Hormuz, potentially supporting wheat prices through higher energy and transportation costs.

Although fertilizer prices have partially retreated, production costs remain elevated, and farmers do not expect profitability to improve quickly. Investors will also closely monitor the July wheat futures settlement on July 14, which may reveal how much of the current geopolitical risk premium remains embedded in futures prices.

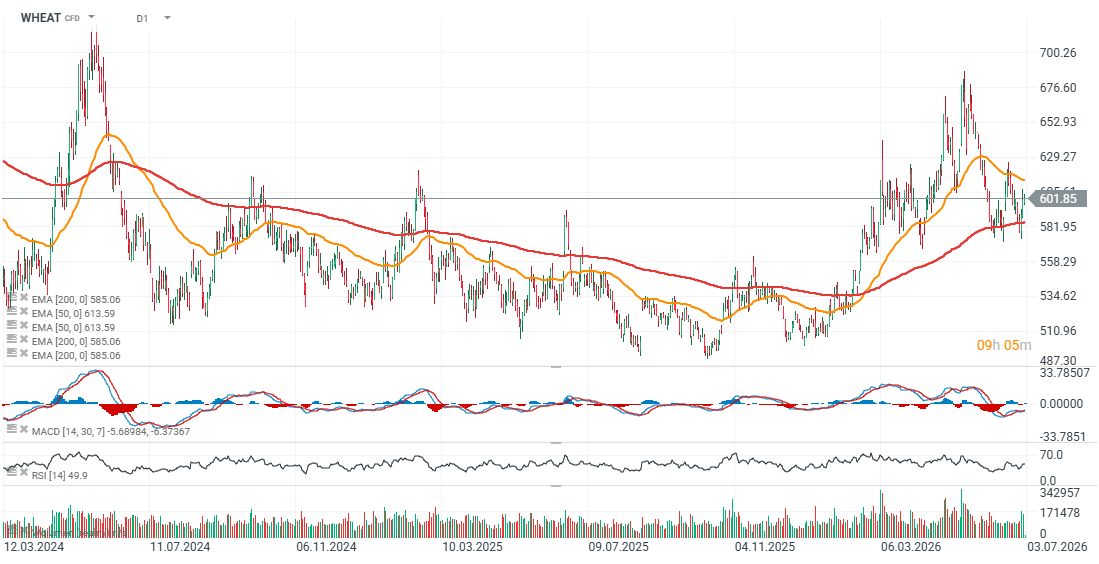

WHEAT Chart (D1)

Looking at the daily chart, CBOT wheat futures successfully defended the 200-day Exponential Moving Average (EMA200), shown by the red line, around the 580–585 cents per bushel area. Strong buying interest at those levels pushed prices back above 600 cents per bushel, leaving the contract roughly 15% below the recent local high near 690 cents.

Over the past three trading sessions, the market has recorded strong buying-dominated volume, suggesting that demand has become increasingly aggressive after the recent rebound.

Source: xStation 5

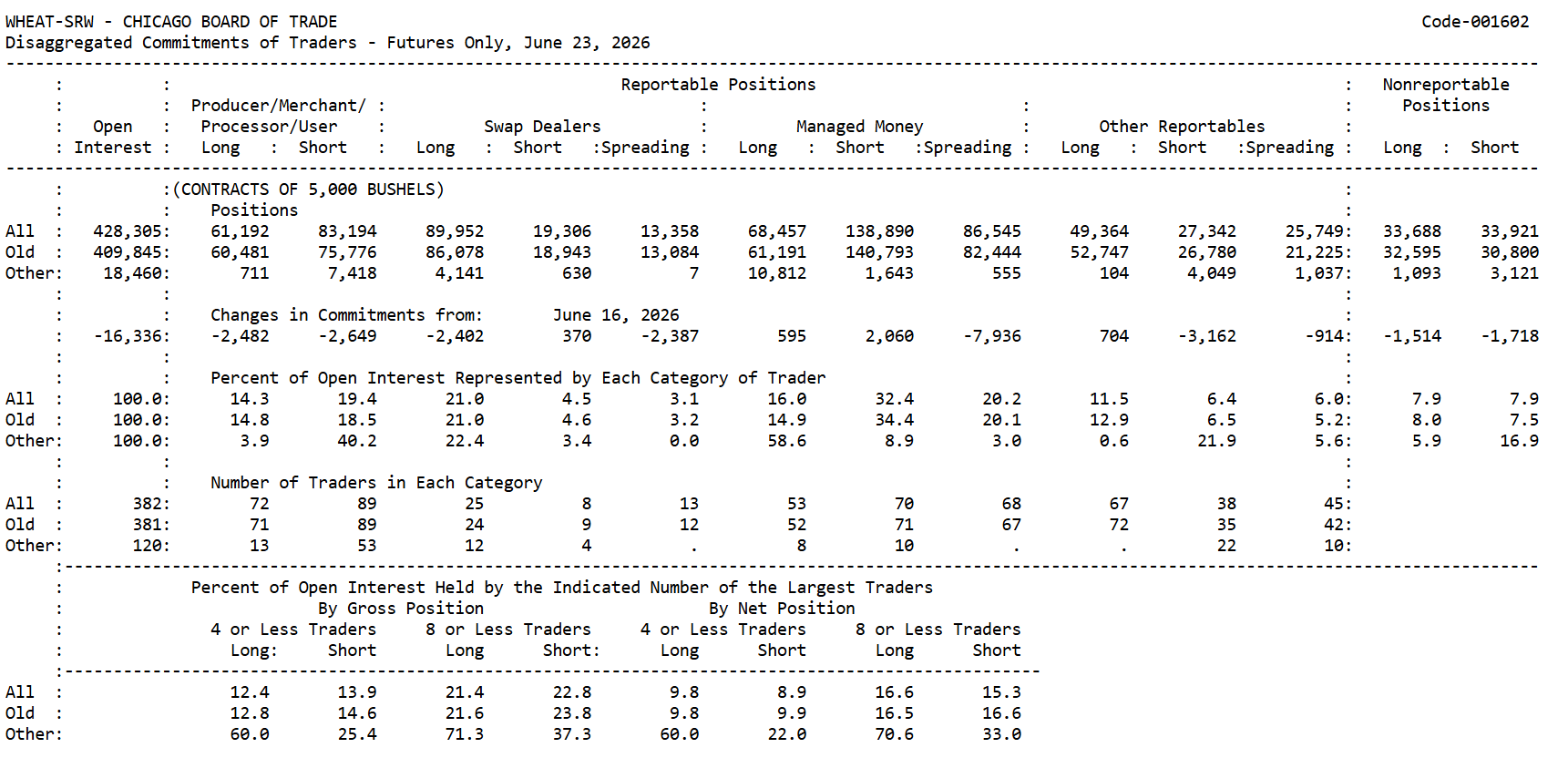

Commitment of Traders (COT) – CBOT Wheat (Report as of June 23, 2026)

Key Takeaways

- Hedge funds remain heavily bearish, holding roughly 70,000 net short contracts despite the recent recovery in wheat prices.

- Commercial participants continue to reduce their short hedges, suggesting that current price levels are becoming increasingly attractive for physical market participants.

- Such a large concentration of speculative short positions increases the risk of a short squeeze if upcoming USDA reports confirm further deterioration in U.S. supply conditions.

Hedge Funds Still Do Not Believe in a Sustainable Recovery

The most interesting part of the latest COT report remains the behavior of speculative funds, classified as Managed Money.

Despite wheat prices rebounding after USDA reports showed lower inventories and a historically small planted area, hedge funds have barely changed their positioning. They currently hold 68,457 long contracts and 138,890 short contracts, resulting in a net short position of approximately 70,000 contracts.

Even more importantly, during the latest reporting week, long positions increased by only 595 contracts, while short positions rose by 2,060 contracts.

This suggests that speculative investors still view the recent rally as a temporary correction within a broader downtrend rather than the beginning of a new bull market.

Commercial Positioning Looks Much More Constructive

The picture is very different for commercial participants, including producers and grain processors.

Although commercials also hold more short than long positions, this is entirely normal. Their futures positions primarily serve as hedges against future production rather than outright directional bets.

The important signal lies in the change in positioning.

During the latest week, commercial participants reduced their short exposure by 2,649 contracts. Such behavior is often observed when physical market participants begin to believe that the downside potential in prices is becoming increasingly limited.

Open Interest Continues to Increase

Another noteworthy development is the rise in Open Interest, which increased from 409,800 to 428,300 contracts.

This is an important signal because rising Open Interest during a price recovery typically indicates that new capital is entering the market, rather than traders simply closing existing positions.

In other words, investors are becoming increasingly active ahead of upcoming USDA reports on crop conditions and U.S. wheat supply.

The Market Remains Vulnerable to a Sharp Reversal

The biggest implication of the current positioning is the elevated risk of a short squeeze.

If future USDA reports confirm the historically low harvested area, declining inventories, or worsening crop conditions, hedge funds may be forced to rapidly cover their exceptionally large short positions.

History has repeatedly shown that similar positioning can trigger powerful rallies in wheat futures, even when fundamental improvements initially emerge only gradually.

Hedge Funds Are Far More Bearish Than Commercials

The difference becomes clear when comparing both groups.

| Group | Long | Short | Net Position |

|---|---|---|---|

| Producer/Merchant (Commercials) | 61,192 | 83,194 | -22,002 |

| Managed Money | 68,457 | 138,890 | -70,433 |

Hedge funds currently maintain a net short position that is more than three times larger than that of commercial participants.

They also hold substantially more outright short contracts—almost 139,000, compared with roughly 83,000 held by commercials.

This imbalance does not automatically mean wheat prices must rise, but it clearly illustrates how heavily one-sided speculative positioning has become.

This is where the most interesting divergence emerges.

Fundamentals have started to improve gradually thanks to the historically small planted area, lower-than-expected inventories, and persistently high production costs. At the same time, speculative funds continue increasing their bearish bets.

Such a disconnect between improving fundamentals and extremely bearish positioning has frequently preceded significant price moves in commodity markets.

If future data continue to confirm tightening supply conditions, hedge funds could eventually be forced to reduce their short exposure, a process that has historically accelerated rallies in wheat prices.

What Does This Mean for Investors?

The COT report alone does not provide a clear buy signal.

On the contrary, it shows that speculative funds remain strongly positioned for further downside.

However, the market is simultaneously receiving an increasing number of fundamental signals supporting higher wheat prices.

This combination makes the current setup particularly interesting.

The longer fundamentals continue improving while speculative short exposure remains exceptionally high, the greater the probability of a sharp shift in market sentiment.

Over the coming weeks, investors should pay close attention to upcoming USDA reports on crop conditions and inventories, while also monitoring whether hedge funds begin reducing their record-sized bearish positions.

A meaningful change in speculative positioning could become one of the most important signals for the next major move in the wheat market.

Source: CFTC, Commitment of Traders (COT)

Eryk SzmydFinancial Market Analyst, XTB

Economic Calendar: Big Tech, Tensions Over Iran, and the ECB’s Decision ⏰

Morning Wrap: A New Threat of Conflict in the Middle East 🚨 (23.07.2026)

Cocoa loses 5% amid rising inventories on ICE

Oil gains 3% amid US - Iran escalation and supply disruption on the Black Sea

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.