September's central bank marathon is almost over - traders have already heard from the Federal Reserve, Bank of England, Norges Bank, Riksbank, CBRT and SNB this week. However, there is one more major central bank left to announce its policy decision this week - Bank of Japan. BoJ will announce its rate decision during the upcoming Asian session. Timing of the announcement is tentative but usually it comes around 3:00 am BST.

What does the market expect?

No change in the level of interest rates in Japan was taken as given for years. There were good reasons for it - inflation in the Japanese economy has constantly undershoot BoJ's target and periods of deflation were not uncommon. However, post-pandemic and war-related acceleration in price growth pushed inflation above target and BoJ has already made some hawkish moves, like widening tolerance band around 10-year target yield. On top of that, new BoJ governor Ueda said earlier this month that there is a non-zero chance that the wage-inflation cycle will be confirmed by the end of this year, what would pave the way for rate increases.

Nevertheless, rate hikes are not expected until the turn of the year. None of the economists polled by Bloomberg expects a decision other than a hold tomorrow. Market sees less than a 10% chance of a rate hike tomorrow and a less than 20% chance of a hike at the October meeting. However, market pricing for a December rate hike is approaching 80%!

Money market pricing does not point to a rate hike at the coming or the next meeting but a 10 basis point hike is fully priced in for the turn of 2023 and 2024. Source: Bloomberg Finance LP

Japan CPI has climbed above the BoJ target amid post-pandemic surge but more persistent wage growth acceleration is yet to materialize. Source: Macrobond, XTB Research

Japan CPI has climbed above the BoJ target amid post-pandemic surge but more persistent wage growth acceleration is yet to materialize. Source: Macrobond, XTB Research

What's next for USDJPY?

Change to the level of interest rates looks highly unlikely and so does any change to the yield curve control mechanism, given that it was altered at the latest BoJ meeting in July. However, the message accompanying the decision will be crucial. If Ueda doubles down on his remarks about the possibility of a wage-inflation cycle materializing soon, could see JPY gain and hawkish BoJ bets in money markets increase further. On the other hand, failure to build upon those remarks may hint that they were made with a sole purpose of supporting yen and it could lead to JPY weakening.

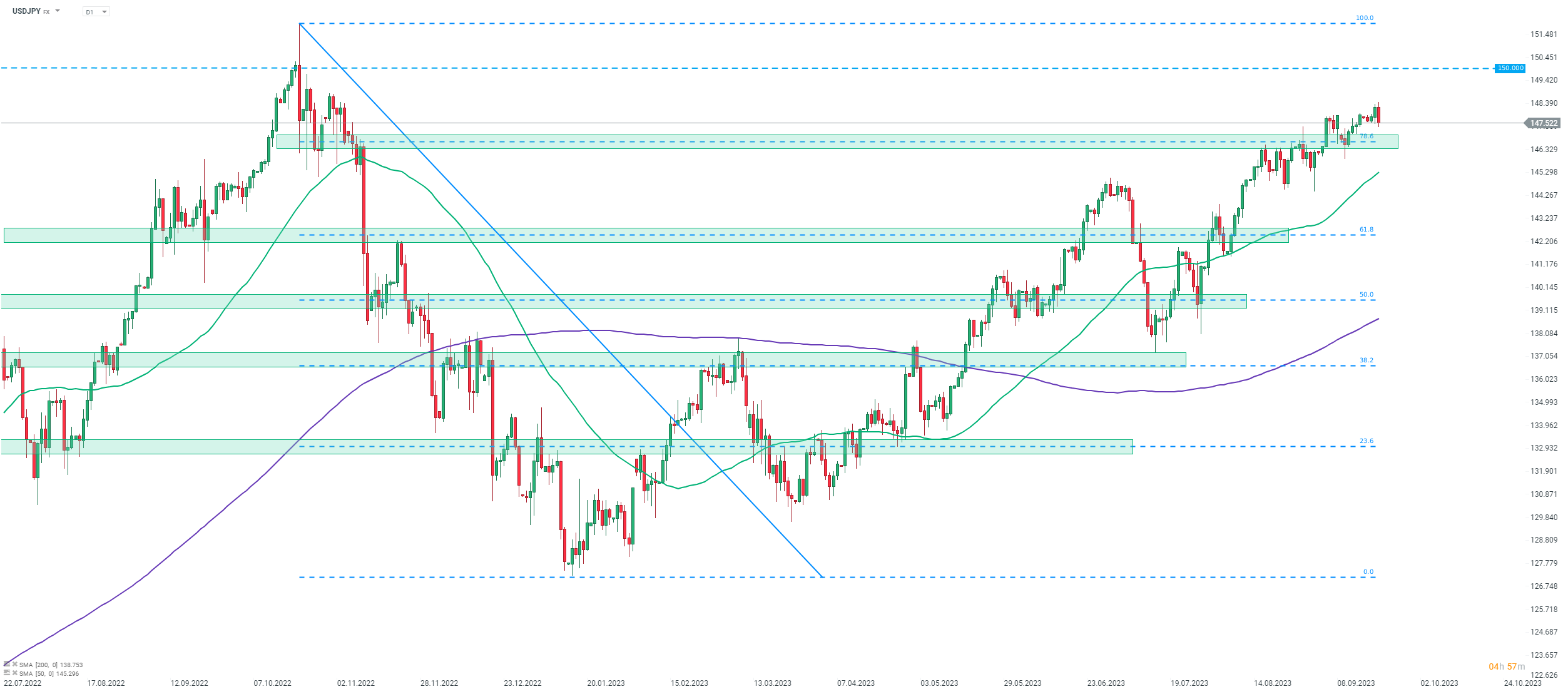

Taking a look at USDJPY chart at D1 interval, we can see that the pair has recovered more than 80% of the downward move launched in October 2022. It should be noted that back then a reversal on USDJPY market was triggered by Japanese intervention and given that the pair is once again approaching 150.00 area, a direct action rather than just verbal intervention becomes more and more likely. JPY weakness is a headache for BoJ and Japanese authorities therefore it cannot be ruled out that Ueda will strike a hawkish note tomorrow to provide some support for JPY.

Source: xStation5

Source: xStation5

Daily Summary - Oil gains due to uncertainty, market awaits inflation data

Chart of the Day: USDJPY Rises Again. Intervention Is Not Enough — Markets Await BoJ Action

Economic Calendar: RBA Holds Rates, Markets Await US Housing Data

Daily Summary: Failure of negotiations in the gulf, oil and gas prices soar

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.