Markets remain highly reactive to earnings surprises, sector rotation, and shifting macroeconomic trends, creating fresh opportunities for investors this month. From Porsche’s turnaround efforts and Nvidia’s highly anticipated earnings report to SoFi’s meme-stock momentum, Nike’s World Cup-driven catalyst, and BP’s strength amid elevated energy prices, these five stocks stand out for their potential to shape market sentiment in May. Here’s what investors should be watching and the key factors that could drive performance in the weeks ahead.

Markets remain highly reactive to earnings surprises, sector rotation, and shifting macroeconomic trends, creating fresh opportunities for investors this month. From Porsche’s turnaround efforts and Nvidia’s highly anticipated earnings report to SoFi’s meme-stock momentum, Nike’s World Cup-driven catalyst, and BP’s strength amid elevated energy prices, these five stocks stand out for their potential to shape market sentiment in May. Here’s what investors should be watching and the key factors that could drive performance in the weeks ahead.

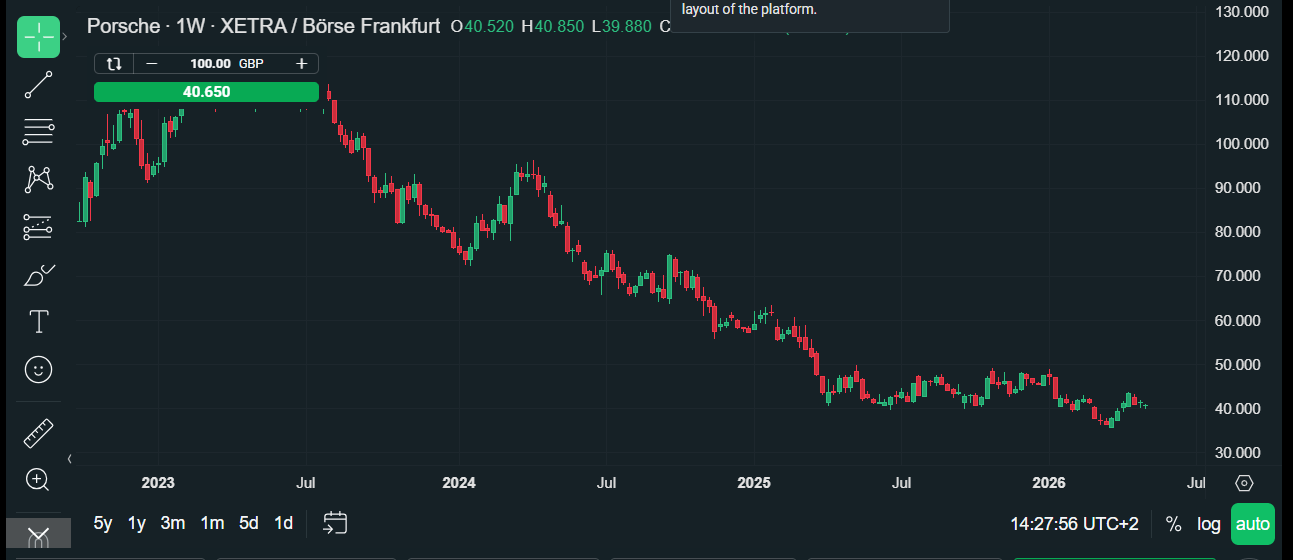

1. Porsche

Things have picked up for Porsche’s share price in the past month, after a rough start to the year for the European auto sector. Porsche has been in focus due to a series of missteps, including falling sales and a delayed switch to EV models. The company reported Q1 profits that were weaker than a year ago at EUR 399mn, vs. EUR 517mn, operating profit slipped and sales revenue fell to EUR 8.4BN from EUR 8.58bn a year before. Deliveries fell by 14% and the company’s share of EV sales was also weaker.

The one bright spot in the earnings report was the forward guidance, which remained stable. The company continues to deliver on its strategy shift under its new CEO and plans to make the company as lean as possible, while delivering new and innovative sports cars. The latest Porsche Cayenne Electric Turbo has received glowing early reviews, and there is hope that sales could receive a boost, even if the macroeconomic backdrop is challenging, due to the rising price of energy and the ongoing war in the Middle East, which is disrupting sales in the lucrative Middle East market.

Even so, the share price has outperformed its rivals so far this year, including BMW and Mercedes Benz. Although Porsche’s share price is down by 12% year to date, this compares to a 19% drop for Mercedes Benz, and a 17% decline in BMW’s share price in the same period. Analysts are neutral on the stock, and this has not shifted even though Donald Trump has slapped another 25% tariff levy on EU auto exports. The President has a history of changing his mind regarding tariff rates, hence this latest threat to the EU car industry may be disregarded by investors at this stage.

As you can see, the share price is hovering near its lowest ever level. If the turnaround plan can take hold, then Porsche could be a bargain.

Chart 1: Porsche, 5-year chart

Source: XTB. Past performance is not a reliable indicator of future results.

2. Nvidia

The chip giant is in focus this month, as we wait for its first quarter earnings report scheduled for release on May 20th. Analysts expect another monster report, and estimated revenues are more than $78bn! The chip and graphics processing sector has been in high demand so far this year, although Nvidia’s share price has been a laggard. It has risen by 4.55% so far this year, this compares to a 56% gain for AMD and a 150% gain for Intel.

Nvidia has a habit of beating earnings expectations and forward guidance. After a strong reporting season for the hyperscalers, who boosted their AI capex spending, expectations are that some of this cash will flow back to Nvidia. The problem for Nvidia’s share price is twofold. Firstly, there is growing competition. For example, Google and Amazon are producing their own chips, while China’s demand for Nvidia’s AI accelerator chips has fallen from a 95% market share in 2022 to 55% today. Exports to China have been hit by trade restrictions and domestic rivals that are taking Nvidia’s market share. The second issue, which is limiting Nvidia’s share price, is its sheer size. It remains the world’s biggest company and has a market cap of $4.8 trillion. Nvidia is essentially a victim of its own success, with investors looking to diversify AI exposure away from just the chip giant.

We doubt that these concerns will impact the numbers that Nvidia reports on 20th May. Although there have been limited gains for the share price this year, the stock still made a record high last month. The question now is, can a bumper earnings season boost the share price back above $200?

Chart 2: Nvidia

Source: XTB.Past performance is not a reliable indicator of future results.

3. SoFi

SoFi’s share price has had a rough start to the year, and is down nearly 40%, however, it has gained traction in the past month and has also generated a lot of attention on social media. After the stock crashed earlier this year, it generated meme-like activity, after a strong Q1 earnings report. The company reported a 43% increase in revenues, and a record increase in customers. The company beat earnings estimates by $50mn, so why did its share price sell off? This was down to forward guidance, which was left unchanged: the company expects revenues of $7.89bn by 2028.

The company is growing fast, and it remains profitable. It also has a small fanbase that is trying to counter the arguments against holding the stock. While there was weakness in loan platform fees in Q1, which fell compared to a year earlier, the company remains over-capitalized and well positioned to fund more loans on its balance sheet throughout this year.

Keyboard warriors are calling out the short squeeze of SoFi’s shares and they see it as unjustified and unfair. This has boosted the share price by 7% in the past month, although it remains deep in the red YTD. For some, this is the opportunity of 2026, especially since the share price is trading at 7 times 2028 EBITDA forecasts.

Chart 3: SoFi 5-year share price

Source: XTB. Past performance is not a reliable indicator of future results.

4. Nike

This is another unloved US stock, which is lower by 30% YTD, however, it is a big year for Nike. It may not be the main sponsor of the Fifa World Cup, that accolade goes to Adidas, however, Nike is the kit supplier for 12 national teams including Brazil, France, England, and the USA. This will give Nike plenty of brand visibility on the pitch. Nike will be a major presence throughout the World Cup, and is spending big on advertising, especially since the tournament is on home soil.

Although Nike’s share price has slumped so far in 2026, going back to 1990, Nike’s share price typically peaks in the weeks leading up to the World Cup, before falling during the event itself. After the World Cup, Nike’s share price trends to rebound strongly, on average 37% from the low through to year end. It also has a history of outperforming the S&P 500 on World Cup years.

Nike’s share price during World Cup years is a ‘buy the rumour, sell the fact’ dynamic. From a company fundamentals perspective, there is a clear link between Nike’s revenue growth and the World Cup. Its revenue growth during World Cup quarters tends to outpace other quarters for the sports brand, averaging 13% revenue growth, vs. 9% growth in non-World Cup quarters.

This is a significant difference, which may give Nike’s share price a meaningful catalyst later this year.

Chart 4: Nike, 5-year chart

Source: XTB. Past performance is not a reliable indicator of future results.

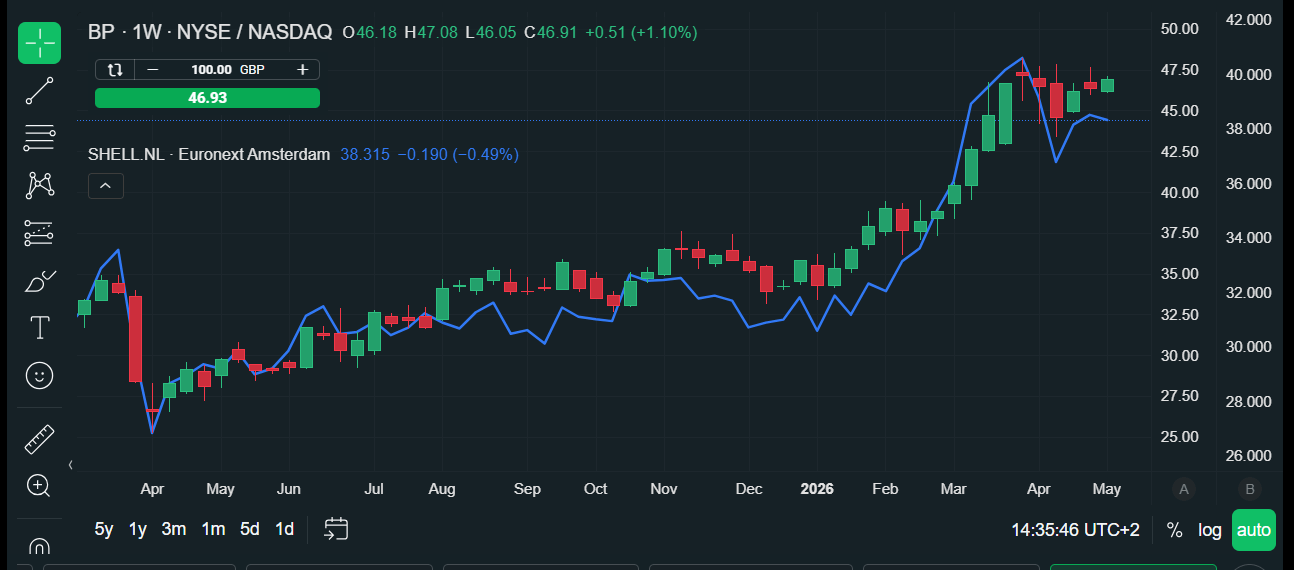

5. BP

The UK energy major has seen its share price rise more than 30% so far this year, as it outperforms some of its biggest rivals. BP had an exceptional Q1 performance, and profits came in at $3.2bn, more than double the year before. The company beat analyst expectations and cited exceptional oil trading revenue as a key driver of the results. The sharp rise in the oil and gas price also boosted the earnings report, as BP traders took advantage of historic volatility in energy prices.

Interestingly, production was also strong, and refining availability was above the 96% target, at 1.5 million barrels per day. This compares to some of its US rivals like Exxon Mobil and Chevron, which saw production disruption last quarter due to the suspension of activities across the Middle East.

The company increased debt last quarter, and net debt rose to $25.3bn. It will need to watch debt creep if it wants to reach its goal to have a net debt position of $14bn - $18bn by 2027. Otherwise, this was an extraordinarily strong report. The company does not expect production to be as high in Q2, as it also struggles with disruption caused by the conflict in the Middle East.

However, the longer the oil price remains elevated, we may continue to see earnings outperformance. The company said that it was focused on boosting its dividend this year and an increase of 4% is expected. If revenues continue to surprise on the upside, then BP could give away even larger shareholder sweeteners.

Overall, although the share price has fallen 3.5% in the past month, this could be a good entry point, as the energy sector remains a hedge in the current environment.

Chart 5: BP and Shell

Source: XTB. Past performance is not a reliable indicator of future results.

Taiwan Semiconductor Manufacturing Company (TSMC): A Global Semiconductor Powerhouse

5 Top Stocks to Watch out for Right Now

5 Top Dividend Stocks for 2025 - Strong Picks Amid Market Volatility

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.