- Dell shares are down more than 10% despite the absence of any direct negative company-specific news.

- The company is widely regarded as one of the biggest beneficiaries of the AI infrastructure investment cycle.

- Global PC shipments declined by nearly 5% year over year in the second quarter

- Dell shares are down more than 10% despite the absence of any direct negative company-specific news.

- The company is widely regarded as one of the biggest beneficiaries of the AI infrastructure investment cycle.

- Global PC shipments declined by nearly 5% year over year in the second quarter

Dell Technologies shares are down more than 11% today, while other AI infrastructure names such as Micron and Sandisk are also trading lower despite the broader US market remaining slightly positive. The scale of the decline suggests investors are reacting less to overall market sentiment and more to growing concerns about the quality and long-term sustainability of the AI infrastructure boom. As one of the largest builders of Nvidia-powered AI servers, Dell sits directly in the AI supply chain, making its valuation highly sensitive to any changes in expectations for hyperscaler data center spending. Dell shares are trading near $400, marking one of the stock's sharpest single-session declines in recent quarters.

-

The main source of pressure stems from concerns that hyperscalers may have overbuilt AI infrastructure. Reports that Meta is considering leasing excess AI training and inference capacity to enterprise customers have raised fears that future AI server demand could slow.

- Dell is particularly exposed to this scenario because it manufactures Nvidia-based AI servers. Any slowdown in AI infrastructure spending would affect not only chipmakers but also system integrators such as Dell.

- Rising memory prices represent another headwind. AI-optimized servers already carry lower gross margins than Dell's traditional hardware business, meaning higher component costs could further compress profitability.

- Insider activity has also weighed on sentiment. Company insiders sold approximately $1.56 billion worth of shares over the past three months without meaningful insider buying, while two additional Form 4 filings were disclosed on July 14.

- Dell's selloff appears to be driven primarily by company- and sector-specific factors. Investors are increasingly questioning whether exceptionally high expectations for AI infrastructure remain justified after a period of explosive order growth and expanding backlogs.

- A short-term risk has also emerged from recent Windows 11 updates. Microsoft temporarily halted the rollout of update KB5101650 to certain Dell devices after reports of unexpected shutdowns, lower performance, overheating, and excessive battery drain.

- The issue has been traced to a compatibility conflict between Microsoft's new USB-C Connection Manager interface and Intel's Innovation Platform Framework driver, which manages processor power and thermal performance.

- Microsoft and Dell are currently working on a fix expected within the coming days. While the financial impact is likely to be limited, the incident could temporarily affect Dell's product quality perception and increase customer support activity.

- Investors are beginning to distinguish between revenue growth and profitability growth. In Dell's case, the key risk is that the AI server boom could ultimately prove less profitable and less durable than previously anticipated.

A Weaker PC Market Does Not Change Dell's Long-Term AI Story

Dell's second major business segment, personal computers, is facing pressure from rising memory and storage costs. Global PC shipments declined by nearly 5% year over year during the second quarter, as higher component prices forced manufacturers to increase selling prices and encouraged customers to postpone purchases. Even so, Dell continued to outperform the broader market, while AI servers remain the company's primary growth engine.

- Worldwide PC shipments declined 4.9% year over year during the second quarter of 2026, according to IDC, as memory and storage prices increased by 20% to 40%.

- Higher component costs translated into more expensive PCs, weakening demand and leading many customers to delay purchases.

- Dell shipped approximately 9.3 million PCs during the quarter and maintained a 14% share of the global market, demonstrating stronger relative performance than many competitors despite weaker industry conditions.

- Dell continues to benefit from its strong enterprise customer relationships and commercial business, allowing the company to gain market share even as consumer PC demand remains subdued.

- AI infrastructure remains Dell's largest growth driver. During fiscal first-quarter 2027, revenue increased 88% year over year to $43.8 billion, comfortably exceeding Wall Street expectations.

- Net income surged 256% to $3.44 billion, GAAP diluted EPS reached $5.24, adjusted EPS came in at $4.86, and free cash flow totaled approximately $3.2 billion.

- Revenue from the Infrastructure Solutions Group climbed 181% to $29 billion, driven by record demand for AI servers and enterprise storage systems used in AI data centers.

- The Client Solutions Group, which includes Dell's PC business, generated $14.6 billion in revenue, representing 17% year-over-year growth despite the weaker global PC market.

In practice, Dell is currently being pulled in two different directions. Its traditional PC business is facing pressure from weaker industry demand and rising component costs, while AI infrastructure continues to expand at a pace that is fundamentally reshaping the company's financial profile. The key question for investors is no longer whether Dell is benefiting from AI, but whether the current growth in AI servers and earnings will prove durable enough to justify today's premium valuation.

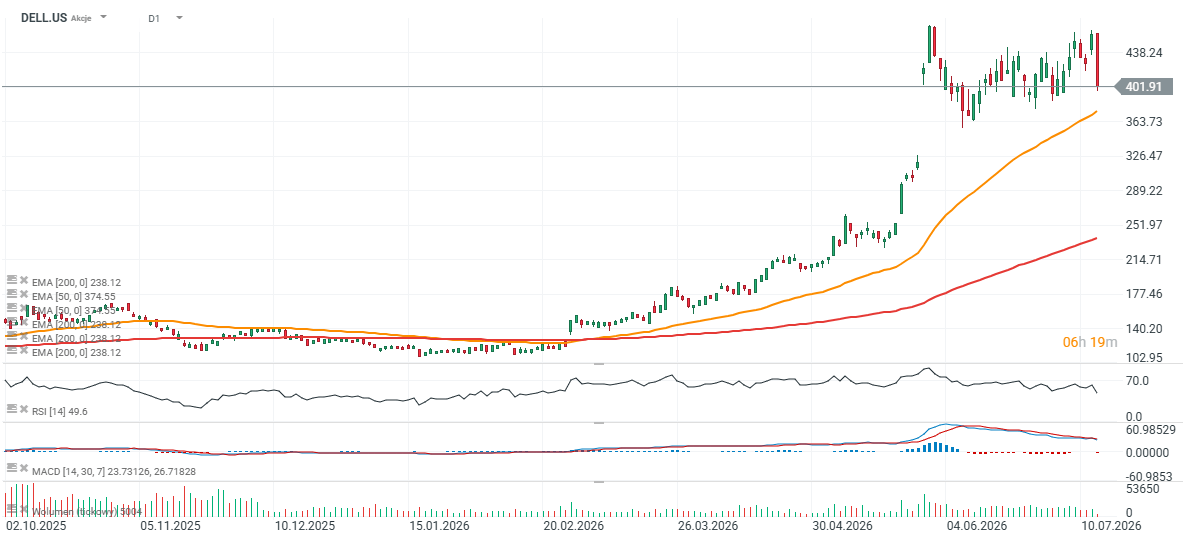

Dell Shares (D1 Interval)

Dell shares are testing the lower boundary of their broader uptrend today, pulling back toward the opening level of the May 29 bullish gap. Valuation remains one of the stock's biggest challenges. Dell currently trades at roughly 30-35 times forward earnings, well above traditional PC manufacturers such as HP. That premium assumes the AI server investment cycle will continue for many years. Any slowdown in enterprise AI spending, delays in infrastructure upgrades, or further increases in memory costs could quickly pressure margins and reduce investors' willingness to pay such elevated valuation multiples.

Source: xStation5

Stock of the Week: Arista Networks—A Second-Tier Technology with Top-Tier Results

US Open: S&P 500 shows strength as semiconductor lags 🚩 Western Digital down 12%

SoftBank earnings: Intel and AI are not enough?

Nasdaq 100 Slides Again 🚩 SanDisk Falls 10% After Earnings, Semiconductors Under Pressure

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.