Apple Inc. is entering its Q2 2026 earnings at a point where the market no longer values the company purely as a stable hardware-and-services business, but increasingly views it as a lagging participant in the global artificial intelligence cycle. This fundamentally changes how results are interpreted, as the focus shifts from the question of “is Apple delivering” to whether “Apple is returning to a phase of innovation-driven growth.”

At the same time, this quarter is also transitional from a product and strategic cycle perspective. Apple is operating between its traditional model built around the iPhone and services, and a new growth architecture that is gradually being built around AI, refreshed hardware, and potential new device categories.

Key market expectations for Q2 2026

-

Revenue around 109.7 billion USD

-

EPS around 1.96 USD

-

iPhone around 57 billion USD

-

Mac around 8.1 billion USD, supported by a new product cycle

-

Services around 30.4 billion USD, a stable high-margin segment

-

China around 18.9 billion USD, a key demand-sensitive region

-

Margins supported by product mix, but under pressure from memory costs

-

CapEx moderate, but gradually increasing due to AI and hardware investment

Market expectations and positioning

The market is pricing in another solid quarter of growth driven by a new product cycle, where the key contributors are the iPhone 17e, refreshed Mac lineup, and new iPads. The MacBook Neo is particularly important as it pushes Apple further into a more mass-market price segment and may expand volumes beyond the traditional premium core.

At the same time, investors assume the company remains partially exposed to memory cost pressures, which could limit margin expansion despite a favorable product mix.

Against this backdrop, the market is no longer evaluating Apple purely on a beat-or-miss basis, but increasingly on the quality and durability of its product cycle.

AI as the missing element of the growth narrative

Artificial intelligence remains a central but still incomplete part of Apple’s story. The company is gradually introducing AI features into iOS and its broader ecosystem, but the market still views these developments as incremental improvements rather than a fundamental shift in how the company operates.

In practice, AI is currently seen as a potential driver of higher device upgrades, a factor that strengthens ecosystem stickiness, and a foundation for future product categories such as wearables, smart home devices, and fully AI-driven hardware. However, there is still no clear evidence that AI is directly generating a new layer of revenue monetization.

Memory costs and margin pressure

A key short-term factor remains pressure in the supply chain, particularly in memory components. Unlike in previous cycles, this is no longer a secondary issue, as it is beginning to affect both product pricing and production capacity.

This means that even with stable demand, Apple may face limitations in further expanding gross margins, which increases the importance of product mix and the Services segment as a stabilizing profit buffer.

Services as a stabilizer, not the main re-rating driver

The Services segment remains one of the most important components of Apple’s business model, generating high-margin and recurring cash flows. However, its role in the current cycle is more stabilizing than growth-driving.

Unlike in previous years, Services is no longer the primary driver of valuation re-rating. Instead, the key factors now are the hardware cycle, artificial intelligence, and potential entry into new product categories.

Management transformation and strategic regime shift

An additional key element is the change in leadership structure, with John Ternus taking over as CEO while Tim Cook transitions to the role of chairman.

John Ternus is viewed as a more product- and engineering-focused leader, which the market interprets as a potential shift toward faster product decisions and a higher willingness to take technological risks. Tim Cook, meanwhile, remains a stabilizing force in operational and geopolitical areas, reducing the risk of abrupt strategic shifts.

High expectations and limited room for error

Apple is currently one of the most fully priced companies among large-cap technology stocks, meaning the market is no longer pricing in stability alone, but rather a renewed acceleration in growth.

As a result, even solid earnings may fail to generate a lasting positive reaction unless they are supported by a clear shift in the forward-looking narrative. The key areas of market sensitivity include the durability of the iPhone and Mac cycle, the impact of memory costs on margins, and the pace of AI integration and monetization.

Key takeaways

-

Apple is in a phase where maintaining growth is no longer sufficient, and a re-acceleration is required

-

The product cycle, including iPhone 17e and MacBook Neo, supports results but does not yet reshape the long-term growth structure

-

Artificial intelligence remains the most important missing element of the investment narrative

-

Memory cost pressure limits further margin expansion

-

The market expects Apple not only to remain stable, but to re-establish its ability to deliver high-quality growth rather than just steady performance

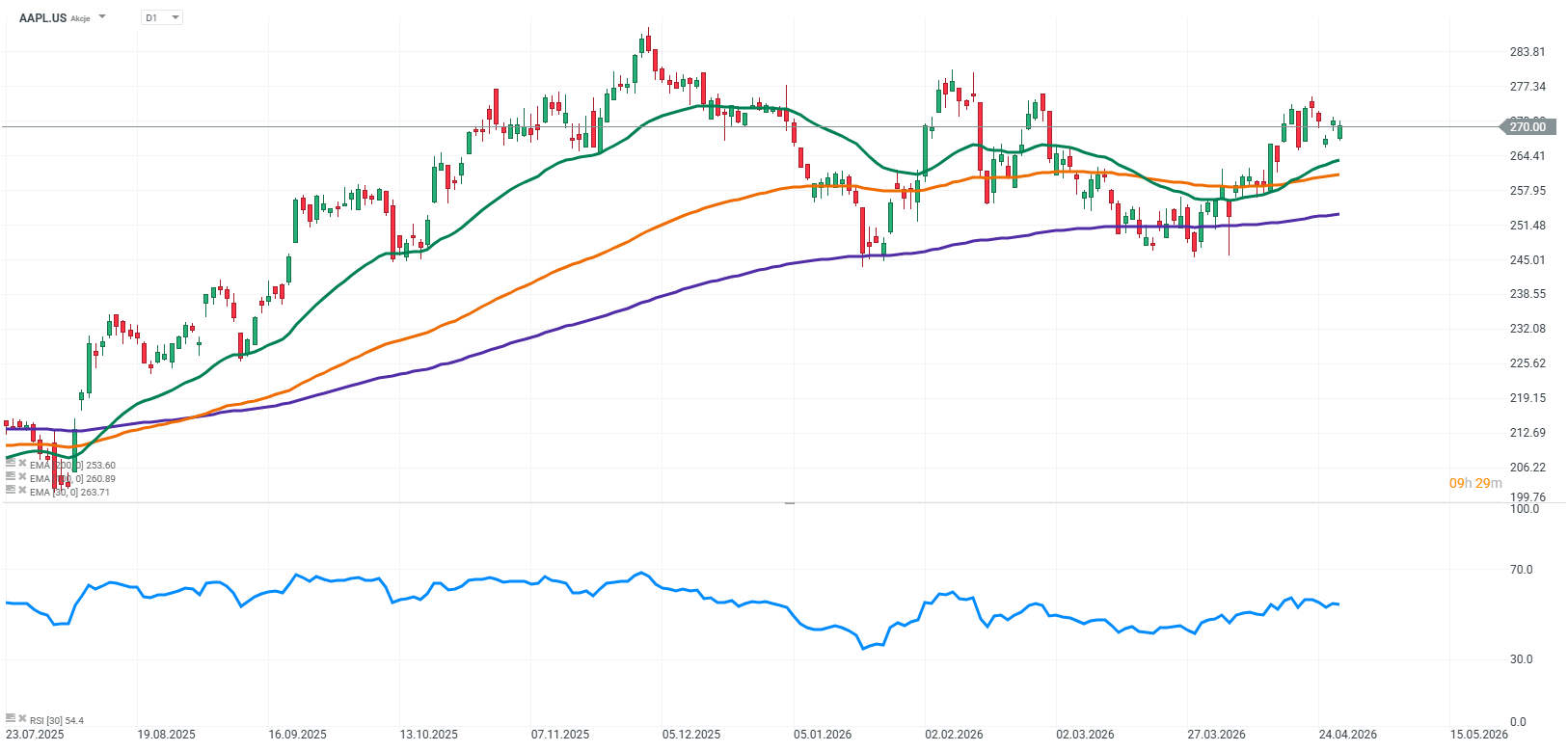

Source: xStation5

US Open: S&P 500 Tries to Halt the Decline 🗽 GE Vernova Falls 5%

Wall Street Fears the Peak of the AI Bull Market. Have Semiconductors Already Seen Their Best Days?

Alphabet and Tesla Ahead of Earnings: Will the Tech Giants Shake Wall Street?

Defense sector ahead of earnings: Summary

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.