Arm Holdings’ results show the company is currently at a very interesting stage of development. ARM is still not benefiting from the artificial intelligence boom to the same extent as Nvidia or AMD, but it is increasingly building a position for the next phase of AI infrastructure growth. However, the market is pricing in this potential well in advance, which naturally raises expectations for every earnings release.

The report itself was solid. The company slightly beat analyst expectations on both revenue and earnings, while maintaining very high profitability. Despite this, investor reaction was relatively muted. After an initial move higher, the stock quickly gave back most of its gains, suggesting that the market was looking for a stronger signal of acceleration in the AI-related business.

Key quarterly figures:

-

Revenue: $1.49 billion (+20% year over year)

-

Adjusted EPS: $0.60 vs. $0.58 expected

-

Licensing revenue: $819 million (+29% year over year)

-

Royalty revenue: $671 million (+11% year over year)

-

Adjusted gross margin: 98.3%

-

Adjusted operating margin: 49%

For years, ARM’s key advantage has been its business model based on processor architecture and technology licensing to the world’s largest technology companies. The company did not need to invest billions of dollars in manufacturing facilities or production capacity, allowing it to maintain exceptionally high margins and a highly scalable business model.

Today, however, ARM is gradually evolving this model. The company is developing its own processors for AI infrastructure and data centers, moving further up the value chain. This represents a significant strategic shift, as ARM aims to participate not only in architecture and licensing revenue, but also in the market for complete computing solutions for modern data infrastructure.

At the same time, ARM still does not intend to operate like a traditional semiconductor manufacturer such as Intel. Its model remains closer to Nvidia: ARM designs chips, while production is outsourced to external partners such as TSMC. Nevertheless, moving into in-house processor development introduces greater operational complexity, higher costs, and the need to build a more extensive supply chain.

This was one of the most interesting elements of the report. ARM stated that demand for its new AI solutions increased from $1 billion to $2 billion, but the company maintained its previous $1 billion revenue target due to supply constraints.

This highlights a key dynamic in today’s AI market. The bottleneck is increasingly not demand, but the ability to scale supply quickly and secure sufficient wafers, memory, packaging, and testing infrastructure. Management noted that the company is actively working to expand its production capabilities in order to meet growing customer demand.

At the same time, ARM is strengthening its presence in data centers. The company’s architecture is no longer associated solely with smartphones and low-power mobile devices. ARM-based processors are already being developed by Amazon, Microsoft, and Google, while its architecture is also present in AI servers built by Nvidia.

This could become one of the most important long-term trends for the company. As AI models scale, energy efficiency and cost optimization in data centers are becoming increasingly critical. ARM’s architecture naturally aligns with these requirements, which could steadily increase its share in modern computing infrastructure.

However, the market remains highly demanding. ARM’s current valuation already reflects a very ambitious growth scenario, meaning that even solid results may not be enough to sustain investor enthusiasm. Today, the market is pricing not the current scale of the business, but ARM’s potential position in the global AI ecosystem several years ahead.

In the long term, the story still looks very compelling. ARM has one of the strongest technology ecosystems in the semiconductor industry, exceptionally high margins, and an architecture that is increasingly aligned with the needs of modern data centers. While it is not yet monetizing AI at the level of Nvidia or AMD, the direction of change is becoming increasingly clear.

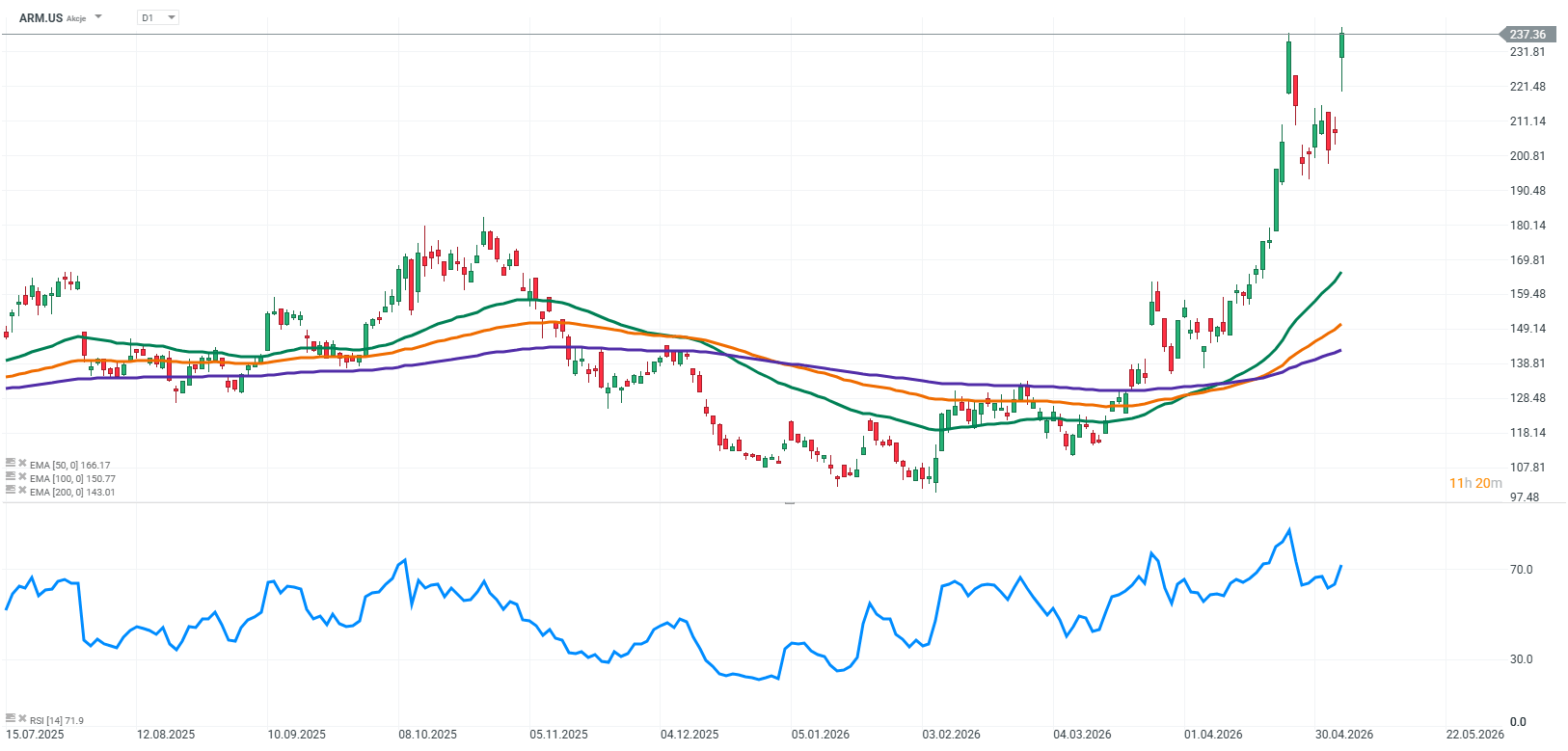

Source: xStation5

AI trade loses momentum, as LVMH fails to impress

Economic Calendar: PayPal, Visa and Coca-Cola to overshadow macro data (28.07.2026)

Morning Wrap: US halt to attacks balanced by semiconductor sector declines (28.07.2026)

Daily Summary: Chip War Weighs on Wall Street as Oil Plunges After US–Iran Ceasefire ⭐

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.