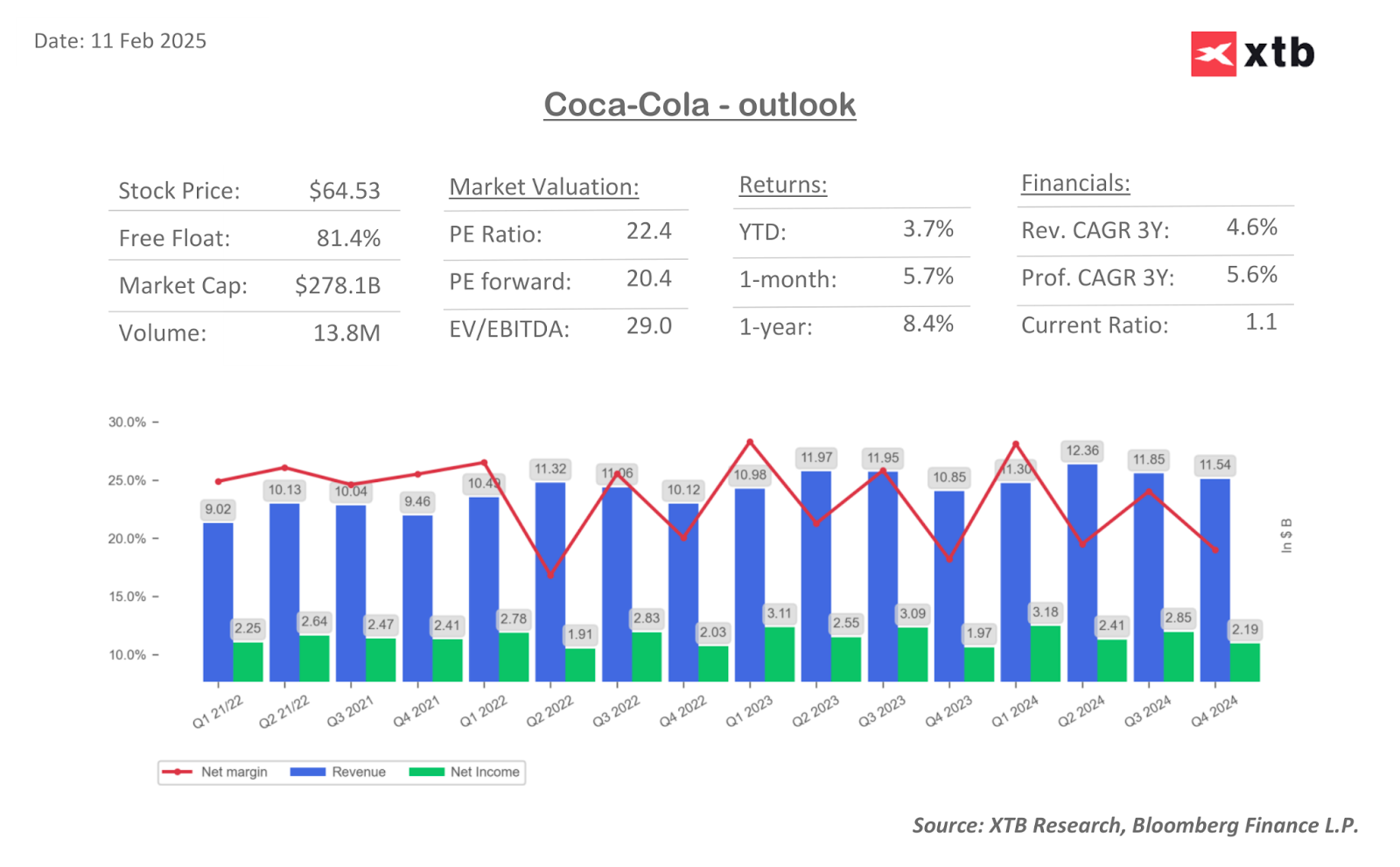

Coca-Cola (KO.US) reported its 4Q24 results today. One of the largest producers of soft drinks broke its negative streak from the previous quarter by reporting a rebound in sales volumes. Additionally, the results stand in contrast to PepsiCo’s report from last week, which was received more cautiously by investors.

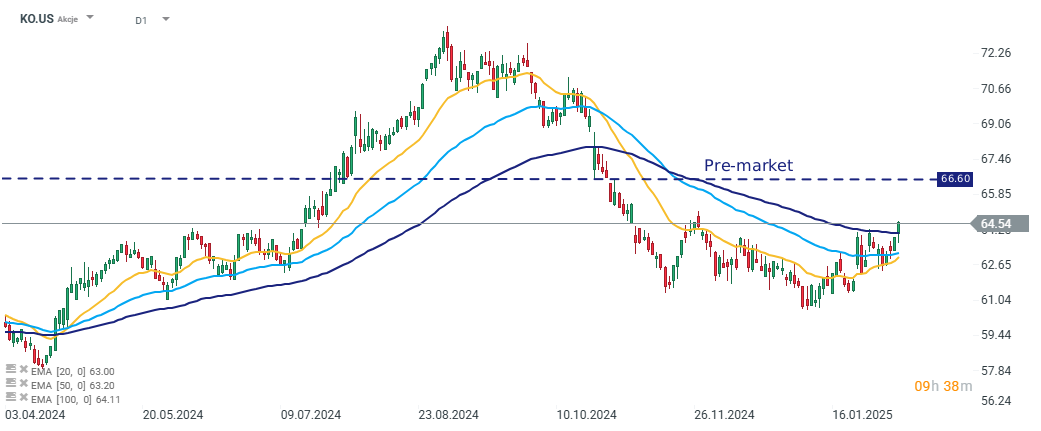

Coca-Cola’s stock is up over 3% in pre-market trading. Source: xStation

At the revenue level, despite a continued q/q downward trend, the company reported better results than last year, overcoming the struggles of the previous quarter. Furthermore, in 4Q24, sales volume increased by 2% y/y.

This is particularly significant for investors given the declines in volume in the previous quarter. Restoring market strength—especially among U.S. consumers—will be key to maintaining the company’s growth momentum in the coming quarters.

The company also improved its profitability, with an operating margin of 24% (compared to 23.1% a year earlier). Although external factors, such as currency fluctuations, impacted the operating margin in the fourth quarter, strong organic sales growth of 14% (compared to the forecasted 7.2%) played a major role in supporting profitability.

This time, the price/mix effect—representing the impact of product mix and price changes on revenue—was even more pronounced. It stood at 9% in 4Q, compared to the forecasted 6.7%.

For 2025, the company expects adjusted EPS growth of 2-3% and organic revenue growth of 5-6%, slightly below the 7% consensus estimate. Despite this minor downside, Coca-Cola delivered strong financial results and alleviated some concerns about market conditions that had built up among investors following the previous earnings report.

4Q24 RESULTS:

- Adjusted EPS: $0.55 (forecast: $0.52)

- Adjusted operating revenue: $11.5 billion (forecast: $10.67 billion)

- Adjusted organic revenue growth: +14% (forecast: +7.24%)

- Price/mix: +9% (forecast: +6.71%)

- Change in concentrate sales: +5% (forecast: +0.56%)

- Unit case volume: +2% (forecast: -0.21%)

- Unit case volume for nutrition, juice, dairy, and plant-based beverages: -1%

- Unit case volume for sparkling soft drinks: +2%

- Unit case volume for water, sports drinks, coffee, and tea: +2%

- Operating margin: 24% (vs. 23.1% a year earlier); forecast: 22%

FULL-YEAR OUTLOOK:

- Expected adjusted EPS growth: +2% to +3%

- Expected adjusted organic revenue growth: +5% to +6% (forecast: +7.09%)

Daily Summary: Chip War Weighs on Wall Street as Oil Plunges After US–Iran Ceasefire ⭐

Nasdaq-100 under pressure after chip sell-off

China Is Building Its Own Chip-Making Machines. ASML Under Pressure as the Technology War Enters a New Phase

US Open: Wall Street Rebounds After US Iran Ceasefire

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.