CoreWeave is one of the leaders of the relatively new “neo-cloud” sector, companies providing cloud services with a tight focus on AI solutions.

A key question is how appropriate the word “leader” really is here, because despite impressive revenue growth and valuations, the growth strategy of most companies in this sector raises serious doubts about its sustainability. These doubts were reflected in the company’s latest earnings call, after which the stock fell by more than 6% in pre-market trading.

Financial metrics

- Revenue posted a phenomenal 112% year-over-year increase, rising to USD 2.08 billion.

- The bottom line looks worse: EPS (loss) came in at -USD 1.4 versus market expectations of around -USD 0.9.

- Backlog surged by as much as 284%, reaching USD 99.4 billion.

However, the deeper we dive into the company’s financial statements, the more questions arise.

- Adjusted net profit fell to USD 21 million, implying a margin of around 1%.

- That is a quarter-over-quarter decline of more than 76% and a year-over-year decline of more than 87%.

- Net loss is growing much faster than revenue and backlog, reaching USD 589 million in Q1.

- This represents a year-over-year increase of 392%.

- Depreciation and amortization expenses are also rising rapidly, reaching USD 1.14 billion (more than half of revenue).

- That is an increase of more than 250% year over year.

Guidance

- The outlook for the second quarter is also below consensus. Management guided revenue to USD 2.45–2.6 billion, versus market expectations closer to USD 2.7 billion.

Against the backdrop of poor financial figures, the company highlights its successes, such as collaborations with Anthropic, Meta, Jane Street, and Mistral. A partial attempt to address the profitability issue and the company’s enormous CAPEX (over USD 6 billion) is to secure financing of USD 8.5 billion and sell a stake worth USD 2 billion to Nvidia. However, concerns about monetization not only remain, the problem is becoming increasingly pressing.

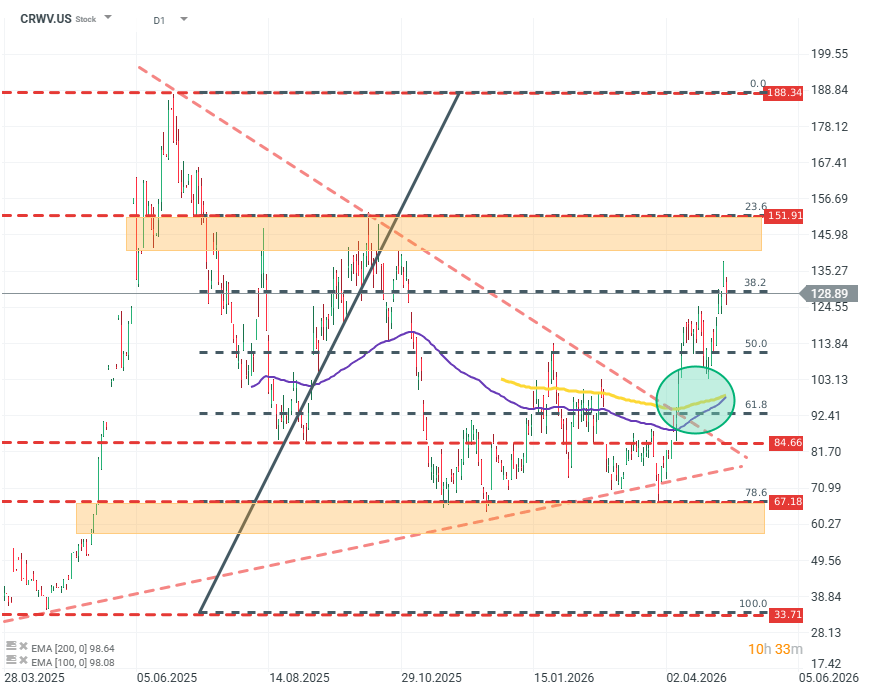

CRWV.US (D1)

The company’s technical picture looks much better than its fundamentals. The share price clearly broke out of a narrowing falling wedge consolidation, stopping at the 38.2% Fibonacci level. If the EMA100 crosses above the EMA200, it would be a strong bullish technical signal. Source: xStation5.

Daily Summary - The market starts to doubt rate hikes after Warsh, but Trump destroys the rebound

US OPEN: Wall Street Holds Its Breath Ahead of Fed Decision and Tech Giant Earnings

SK Hynix earnings: Did market over-sold?

France Challenges Palantir, Market Reacts.

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.