🔑 The main factor shaping volatility

The primary driver of today's market movements appears to be falling energy commodity prices. Brent crude oil is currently trading below $105 a barrel, down 6% from its opening price. TTF natural gas saw a similar decline. This limited further gains in bond yields, which had reached their highest levels in the United States since January 2025, when President Trump was inaugurated.

Markets are anticipating NVIDIA's earnings release, scheduled for 10:30 p.m. The semiconductor sector is experiencing strong gains today, partly fuelled by the announcement of strikes by Samsung workers. Solid gains are being recorded by companies including Intel (5.6%) and Micron (3.4%).

🌍 Geopolitics

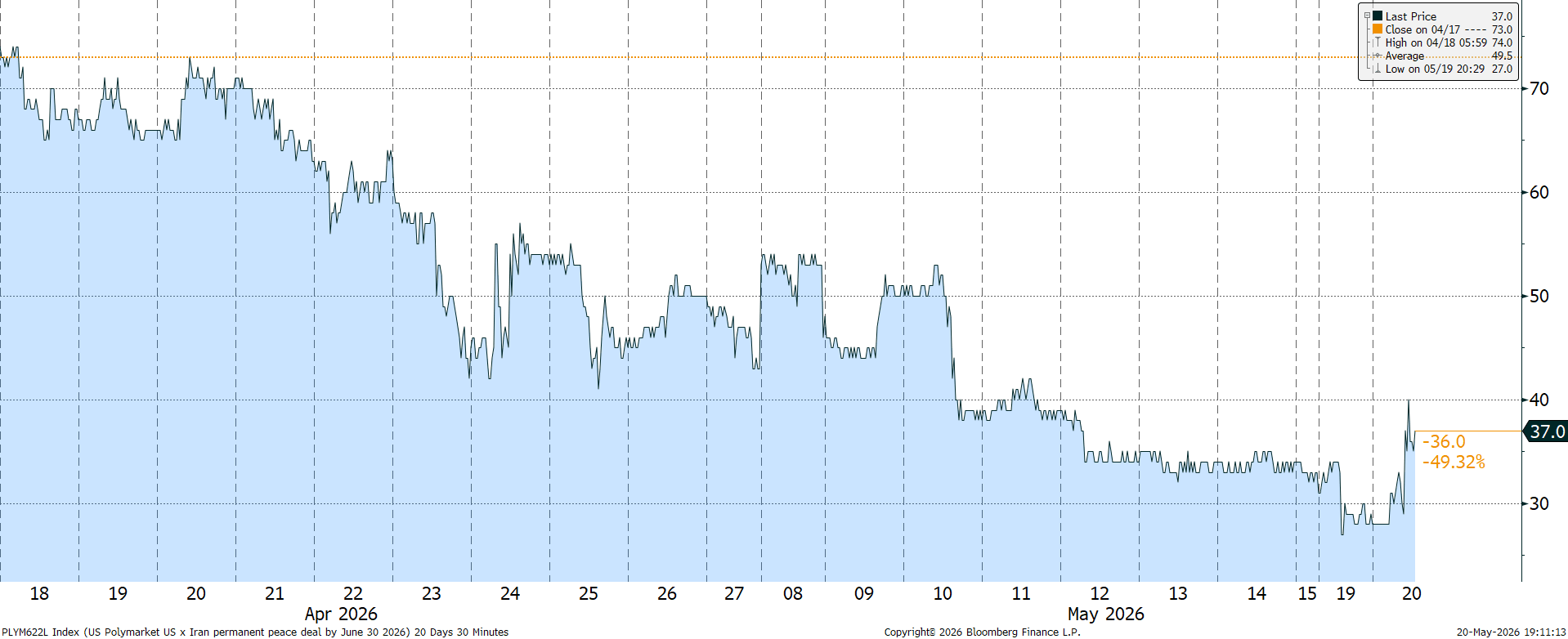

The aforementioned decline in energy commodity prices is partly due to President Trump emphasising today that negotiations with Iran are in their "final stages". He also noted, however, that if Iran fails to comply with US demands, it should expect a resumption of attacks. The Republican's statements are highly erratic and inconsistent, preventing markets from increasing their bets on a swift and meaningful agreement between the parties. The probability of such an event occurring before the end of June, as implied by the Polymarket platform, increased today from 28% to 37%, partly reflecting a shift in market sentiment.

Chart 1: Likelihood of a lasting agreement between the US and Iran by the end of June according to Polymarket (18 April - 20 May)

Source: Polymarket via Bloomberg (20.05.2026)

📊 Macro data

UK CPI inflation data surprised to the downside today. The core measure reached its lowest level since July 2021 (2.5%), pleasantly surprising investors and significantly reducing bets on interest rate hikes from the Bank of England. Two upward moves before the end of the year are no longer fully priced in, and the likelihood of a July hike is now comparable to a coin toss.

Investors are already looking ahead to tomorrow's release of the May PMI figures for major economies. In the meantime, markets are digesting the latest FOMC minutes.

📈 Indices

Ahead of NVIDIA's earnings release, the S&P 500 gained 0.8%, and the NASDAQ Composite rose by 1.2%. European markets closed the day with even stronger gains. The German DAX rose by 1.4%, the French CAC 40 by 1.7%, and the pan-European EuroStoxx 50 by 2.1%.

💼 Shares

Once again, AI ecosystem companies are performing strongly. As mentioned, some are supported by the planned commencement of the Samsung workers' strike on Thursday. However, the market is primarily awaiting NVIDIA's results, which will help dictate the future direction of market sentiment towards the sector.

Among the biggest winners today are:

- AMD (9.8%)

- Intel (5.6%)

- Micron (3.4%)

💱 Currencies

Amid a general improvement in risk sentiment, higher-beta currencies, such as the Swedish krona and Antipodean currencies, are gaining ground. Despite declining expectations for rate hikes, the British pound is also strengthening. The EUR/USD pair remains relatively stable (+0.2%).

- In emerging markets, currencies most exposed to the protracted energy crisis in the Strait of Hormuz (ZAR, KRW, HUF) are appreciating.

🛢️ Commodities

Growing hopes for a resolution to the conflict in the Middle East led to a significant decline in oil and gas prices today (both Brent crude oil and Dutch TTF gas fell by over 6%). The resulting decline in government bond yields, in turn, supported silver (3.0%) and gold (1.0%).

₿ Cryptocurrencies

Market sentiment favours both Bitcoin and Ethereum, with both gaining approximately 1% today.

—

Michał Jóźwiak, Financial Markets Analyst at XTB

Defense sector ahead of earnings: Summary

🛢️Brent Crude Oil Tests $95 per Barrel

Morning Wrap: AI companies and gold back in favour? (22.07.2026)

Red Sea, but not the indices : The effects of the Bab al-Mandab blockade.

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.