-

Wall Street indices traded lower today with small-cap Russell 2000 dropping over 1%, Dow JOnes trading 0.7% down and S&P/ASX 200 declining 0.3%. Nasdaq is an exception and manages to post a 0.1% gain

-

European stock markets traded lower today but the scale of declines was rather small. German DAX dropped 0.12%, French CAC40 trades 0.16% lower while UK FTSE 100 was 0.34% down

-

No breakthrough was made on the US debt ceiling and media reports hint that negotiations may drag

-

US President Biden wants to reach an agreement ahead of G7 meeting later this week but Democrats and Republicans are said to still be far apart on key issues

-

Fed Mester said that Fed remains committed to bringing inflation back to 2% and she does not think that central bank reached a spot to hold rates yet

-

Fed Barkin said that he likes optionality signaled by latest FOMC statement and that a lot may change in the outlook ahead of June meeting as a lot of key data will be released before it

-

Fed Williams said that inflation is gradually moving in the right direction and that economy is beginning to return to more normal patterns

-

ECB Holzmann said he would have preferred a 50 basis point rate hike at May meeting and said that rates need to go beyond 4% to combat inflation

-

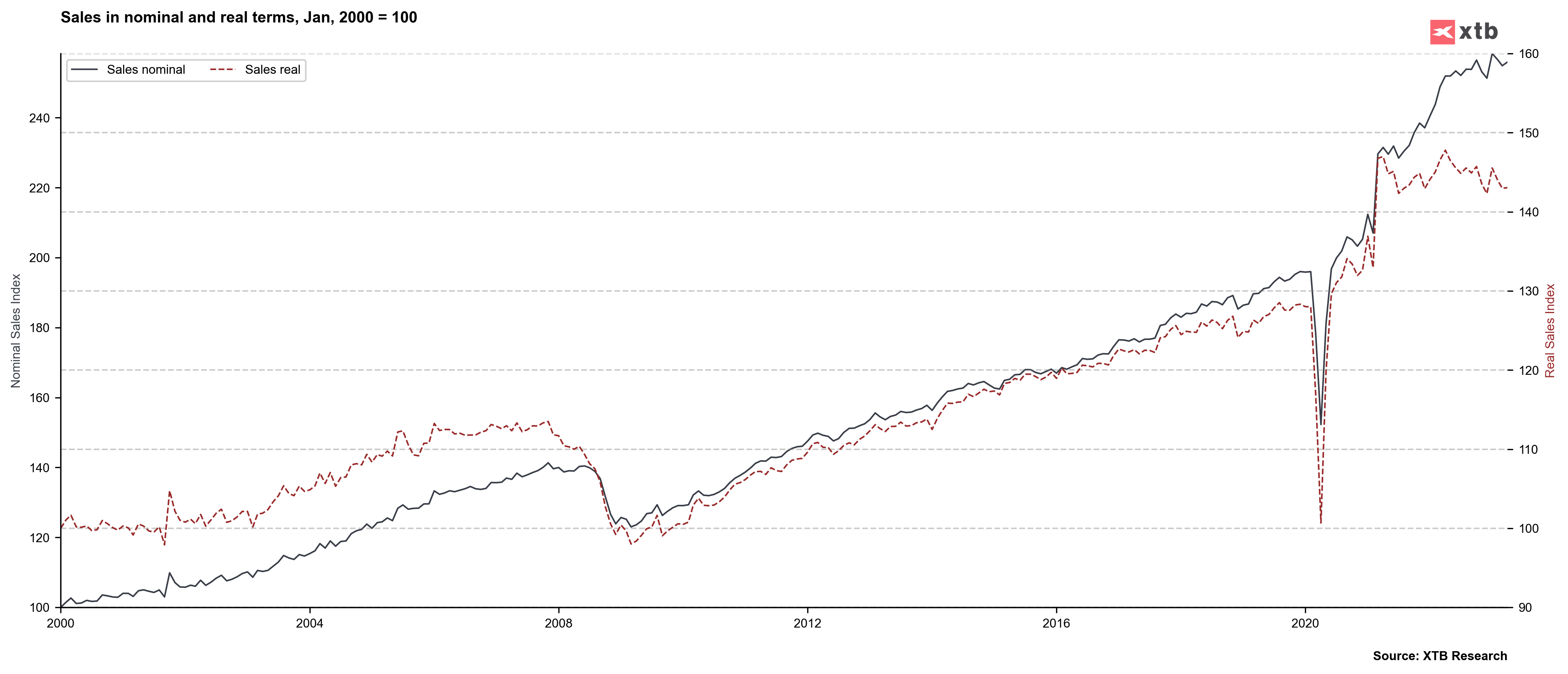

US retail sales data for April came in mixed - headline retail sales missed expectations (0.4% MoM vs 0.8% MoM expected) while retail sales ex-autos matched analysts' expectations of 0.4% MoM

-

US industrial production increased 0.5% MoM in April (exp. 0.0% MoM)

-

Canadian CPI inflation accelerated from 4.3 to 4.4% YoY in April (exp. 4.1% YoY)

-

Chinese activity data for April turned out to be a disappointment. Retail sales were 18.4% YoY higher (exp. 21.0% YoY), industrial production increased 5.6% YoY (exp. 10.9% YoY) while urban investments rose 4.7% YoY (exp. 5.5% YoY)

-

UK jobs report for March showed 5.8% YoY increase in wages (exp. 5.8% YoY) as well as the unemployment rate ticking higher from 3.8 to 3.9% (exp. 3.8%)

-

Euro area GDP report for Q1 2023 showed a 0.1% QoQ expansion - in-line with preliminary release

-

German ZEW index dropped from 4.1 to -10.7 in May (exp. -5.3)

-

Polish Q1 GDP report showed a 0.2% YoY contraction (exp. -0.8% YoY). On a quarterly basis growth reached 3.9% QoQ (exp. 0.7% QoQ)

-

IEA boosted global oil demand growth forecast for 2023 to 2.2 million barrels per day, up from 2.0 mbpd previously

-

Atlanta Fed GDPNow model points to a 2.6% growth in Q2 2023, down from 2.7% in previous release

-

USD and CAD are the best performing major currencies while NZD and AUD lag the most

-

USD strengthening pressures precious metals with gold trading over 1% lower and dropping below psychological $2,000 mark

-

Energy commodities traded mixed today - oil dropped 0.7% while US natural gas prices climbed 0.8%

-

Cryptocurrencies traded lower today - Bitcoin dropped 1.1%, Dogecoin traded 0.4% down while Ethereum declined 0.1%

US retail sales climbed in April, following a drop in March. However, the situation looked less upbeat in case of real retail sales as gap between the two continues to grow. Source: Macrobond, XTB

US retail sales climbed in April, following a drop in March. However, the situation looked less upbeat in case of real retail sales as gap between the two continues to grow. Source: Macrobond, XTB

FX Weekly: Yen Returns to Losses, Dollar Under Pressure (10.08.2026)

The Week Ahead: 3 Events to Watch

Economic Calendar: Markets Awaken After a Weekend of Geopolitical Deadlock🚢

Morning Wrap: No Breakthrough in the Strait of Hormuz; Investors React to Berkshire Hathaway's Earnings

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.