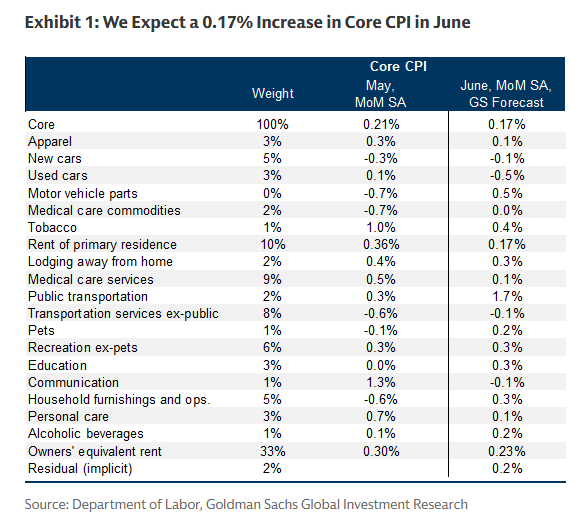

Investor attention today is focused on the June U.S. CPI report, due at 1:30 PM GMT. Goldman Sachs forecasts suggest that the report may be interpreted as moderately dovish. The most important inflation component, housing costs, continues to slow, while the automotive sector has exerted mild disinflationary pressure. Oil prices have also fallen sharply from their recent peaks.

- Only selected services, such as airfares and hotels, continue to show notable price pressure, but not enough to change the broader picture. Goldman Sachs believes that some of the recent favorable inflation data may have reflected seasonal effects, meaning that a single report would not yet confirm a lasting return of inflation to the Fed’s target.

- GS expects headline CPI to rise by 3.8% year-over-year and core CPI by 2.8%. On the other hand, oil prices have rebounded by more than 20% from their recent low, which could lead investors to view even a favorable CPI report as partly outdated.

Macroeconomic data

- 11:00 AM GMT – United States: NFIB Small Business Optimism Index, forecast: 95.7, previous: 95.3.

- 1:15 PM GMT – United States: ADP weekly employment change, forecast: none, previous: 21,000.

- 1:30 PM GMT – United States: CPI inflation year-over-year, forecast: 3.8%, previous: 4.2%.

- 1:30 PM GMT – United States: CPI inflation month-over-month, forecast: -0.1%, previous: 0.5%.

- 1:30 PM GMT – United States: core CPI inflation year-over-year, forecast: 2.8%, previous: 2.9%.

- 1:30 PM GMT – United States: core CPI inflation month-over-month, forecast: 0.2%, previous: 0.2%.

- 1:55 PM GMT – United States: Redbook Index year-over-year, forecast: none, previous: 11.5%.

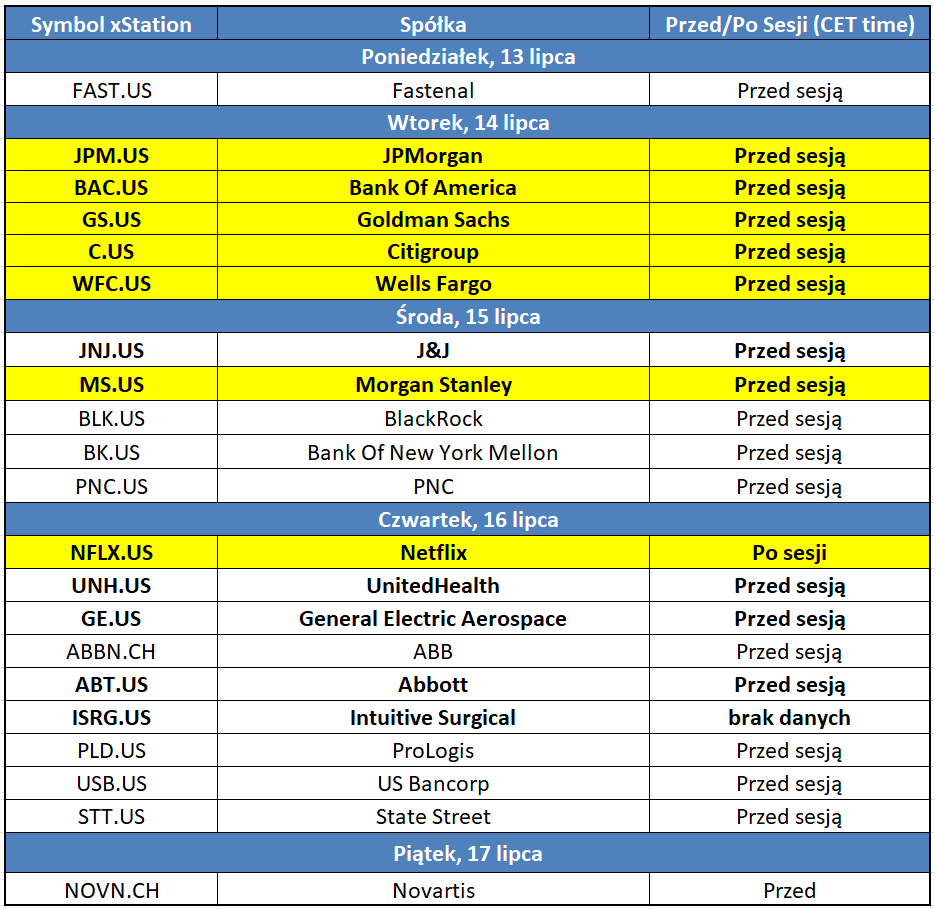

Corporate earnings

- 11:35 AM GMT – JPMorgan Chase: Q2 2026 earnings.

- 11:40 AM GMT – Wells Fargo: Q2 2026 earnings.

- 11:45 AM GMT – Bank of America: Q2 2026 earnings.

- 12:25 PM GMT – Goldman Sachs: Q2 2026 earnings.

- 1:00 PM GMT – Citigroup: Q2 2026 earnings.

Central bank speakers

- 3 PM GMT – Kevin Warsh, Federal Reserve Chair

- 3:30 PM GMT – Christopher Waller, Federal Reserve.

- 5:40 PM GMT – Austan Goolsbee, Federal Reserve.

- 6:30 PM GMT – Susan Collins, Federal Reserve.

- 7:55 PM GMT – Michelle Bowman, Federal Reserve.

- 9:00 PM GMT – Andrew Bailey, Bank of England.

Other events

- 9:00 PM GMT – Planned start of the U.S. naval blockade of Iran.

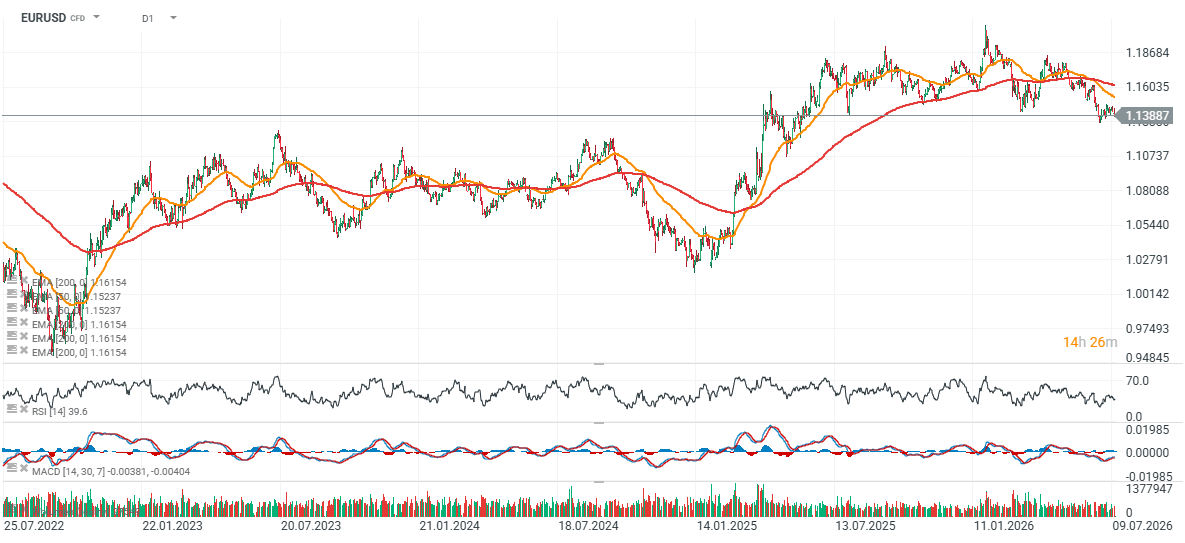

EUR/USD chart (D1 interval)

Oil prices have rebounded by more than 20% from their recent low near $70, supporting further declines in EUR/USD and strengthening the U.S. dollar. EUR/USD is trading below two key moving averages: the EMA200, shown by the red line, and the EMA50, shown by the orange line, signalling a medium-trend downtrend.

Source: xStation5

Corporate earnings calendar for the full week, July 13-17, 2026

Source: XTB Research

Source: Goldman Sachs

Chart of the Day: Yen Falls From 40-Year Highs – What’s Next? (03.08.2026)

Wall Street rebounds as Q2 earnings season significantly exceeds investors expectations

Economic Calendar: What Could Move the Market This Week? (03.08.2026)

The Week Ahead

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.