Markets are starting the new week under dual pressure: the escalation of the Iran-Israel conflict and the Fed’s shift in narrative from a pivot to potential rate hikes. This combination has pushed oil prices higher and sent tech stocks sharply lower.

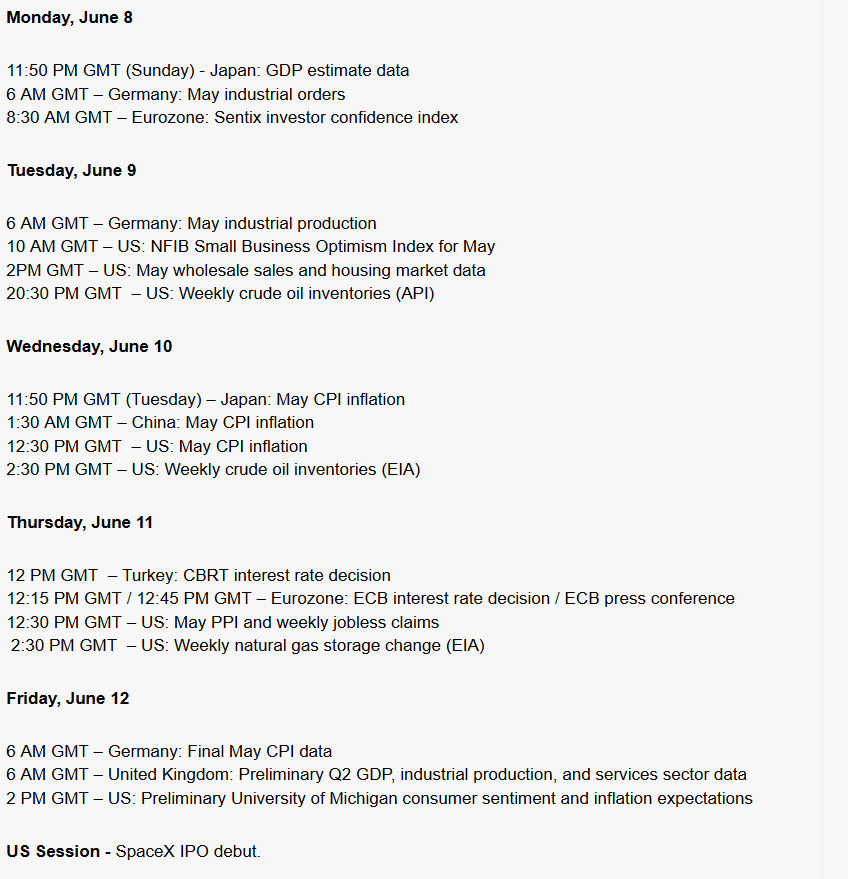

Schedule for today and the rest of the week

Wednesday’s CPI release and Thursday’s ECB decision are the key events of the week—together with any potential geopolitical escalation, they will set the tone for the coming weeks. It’s shaping up to be a busy week, especially for the tech sector.

What drives the markets in the morning?

Escalation in the Middle East

Iran fired rockets toward Israel for the first time in four weeks; Israel responded with strikes on approximately 10 military targets, including the Karoon petrochemical complex in Khuzestan. The Strait of Hormuz remains effectively closed – OPEC+ is producing just 33.19 million b/d, compared to 42.77 million b/d in February. Result: WTI +4.93% (~$94.63), Brent +5.04% (~$97.60) – the largest single-day jump in months.

The Fed is back on track with rate hikes

Friday’s NFP report (+172,000, the third strong month in a row), combined with the energy shock, pushed the probability of a Fed rate hike before year-end above 70%. Goldman Sachs has pushed back the first rate cuts to 2027, and the market is fully pricing in a tightening of about 30 basis points. Today after 4:00 p.m., we’ll see the NY Fed’s data on inflation expectations—a rise in the 3- and 5-year horizons could add fuel to the fire.

European market open – DE40 and EU50 in the red

Futures were down about 1% before the market opened; right at the start of the session the DE40 fell -0.75% to 24,411 points, and the EU50 -0.70% to 5,972 points. Additional pressure came from data released today from Germany—industrial orders for April fell -3.8% m/m (forecasts: -2.0%), following a +4.5% jump in March, confirming that the March surge was a one-off effect of pre-emptive ordering ahead of supply chain disruptions.

Companies with the highest volatility

Technology remains at the epicenter of change following Friday's "red map" on Wall Street:

-

Semiconductors: MU -13.25%, INTC -11.28%, AMD -10.86%, AMAT -9.71%, NVDA -6.2%

-

Big Tech: META -5,51%, MSFT -2,66%, AVGO -7,92%

-

Clear defensive rotation: UNP +13.19%, WMT +4.09%, JNJ +2.02%, KO +3.46%

In Asia, the KOSPI triggered a circuit breaker (down 8% at its peak, closing the session down about 5%), the Nikkei fell 3.7%, and TSMC dropped 2.1%.

Currencies and metals

The DXY is hovering around 100 – the dollar is at two-month highs. EUR/USD 1.1516, USD/JPY above 160 – the yen has erased the entire effect of the BoJ’s May intervention. Gold is down -0.51% to $4,296 – rising real interest rates are outweighing its safe-haven appeal; silver is down -1.67%.

Bitcoin is making a comeback

After falling below $60,000 on Friday (its biggest weekly drop since the FTX collapse), Bitcoin has rebounded to around $62,900, up 2.03%.

Daily Summary: Failure of negotiations in the gulf, oil and gas prices soar

FX Weekly: Yen Returns to Losses, Dollar Under Pressure (10.08.2026)

US OPEN: Debt and the Strait of Hormuz fuel growing concerns.

⬆️TTF gas rises over 6% near 58 EUR

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.