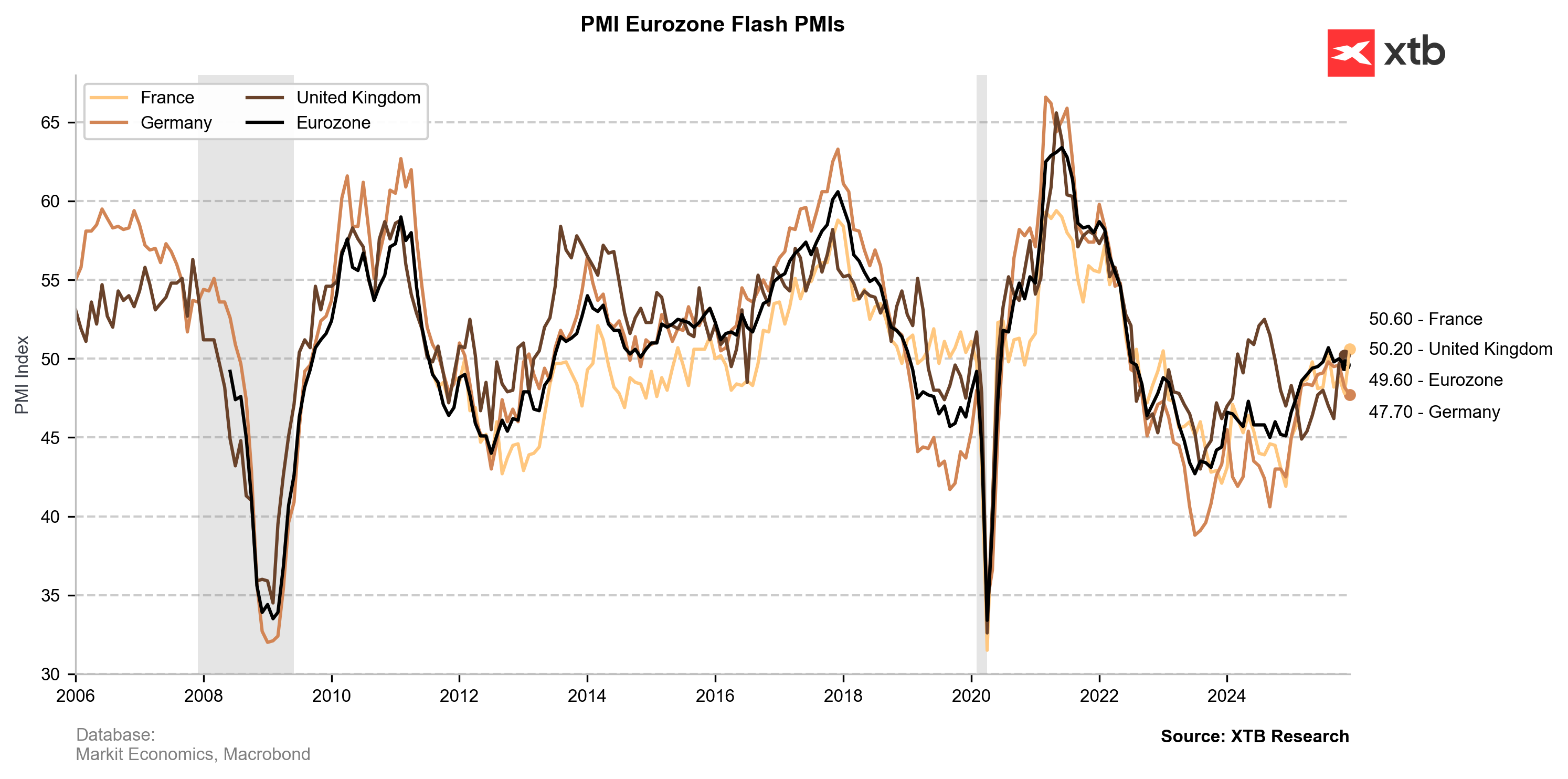

The Euro is trading lower following the release of the final preliminary Purchasing Managers’ Index (PMI) data for December, which highlighted fatal weakness in Germany’s manufacturing sector and a mixed activity profile for France.

Germany: Preliminary December PMI Readings

-

Manufacturing PMI: 47.7 (Expected 48.5; Prior 48.2). Significantly worse than anticipated. Signals further distress for the industrial sector, which has struggled to gain traction throughout the year.

-

Services PMI: 52.6 (Expected 53.0; Prior 53.1). Marginally below expectations. The sector remains in expansion territory but is losing momentum.

-

Composite PMI: 51.5 (Expected 52.4; Prior 52.4). Worse than expected. Indicates a slowdown in the overall rate of economic growth.

France: Preliminary December PMI Readings

-

Manufacturing PMI: 50.6 (Expected 48.1; Prior 47.8). Significantly better than anticipated. A surprise return to the expansion zone (above 50.0).

-

Services PMI: 50.2 (Expected 51.1; Prior 51.4). Worse than expected. A slowdown in the rate of growth, bordering on stagnation.

-

Composite PMI: 50.1 (Expected 50.3; Prior 50.4). Marginally worse than expected. The economy is effectively stagnating at year-end.

Market Reaction and ECB Implications

Despite an initial flicker of optimism sparked by the unexpected improvement in French manufacturing, the overwhelmingly negative tenor of the German data has dominated market sentiment. The Euro is distinctly weaker following the releases, with a similar reaction observed in German bond yields.

The current readings suggest that the European Central Bank (ECB) may lack the mandate to shift its rhetoric to a more aggressively hawkish stance in upcoming meetings.

Key Takeaways

-

German Industry Under Pressure: The primary disappointment lies with the German Manufacturing PMI (47.7). This sharp decline, falling well short of forecasts, signals a deepening contraction in the bloc's key industrial engine. Production is falling for the first time in 10 months, confirming substantial sector weakness. It raises questions over whether the anticipated economic recovery for 2026 will materialize.

-

France’s Faltering Stability: France presents a mixed picture: industrial stabilization is positive, but the services sector is rapidly losing steam. The French Composite activity (50.1) signals a precarious balance between expansion and stagnation. Despite domestic political headwinds, the expansionary nature of the manufacturing print is a welcome development.

-

Wider Eurozone Outlook: The acute weakness in Germany, the Eurozone's largest economy, outweighs the relative strength seen in French manufacturing. The German Composite PMI’s drop to 51.5 (vs 52.4 expected) implies a further deceleration in the region’s growth momentum.

-

ECB Policy Stance: The ECB is expected to maintain a neutral position in its forward guidance. The data is broadly consistent with the trend observed throughout 2025. Crucially, there appears to be little prospect for introducing a more hawkish tone for 2026. This dynamic may serve to neutralize any residual positive impact on the euro stemming from recent hawkish comments by policymakers like Isabel Schnabel.

Three Markets to Watch Next Week (July 31, 2026)

What July can tell us about where stocks go next

Market Wrap: European equities at 3-week highs! Apple dips in US premarket!

Euro Area core inflation above estiamtes! EURUSD under key resistance!

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.