We’re just moments away from the release of the May CPI report — the most important macroeconomic publication of the week. The release is especially crucial given the current economic backdrop, including the ongoing trade war. This month’s data could reveal the first signs of the tariffs announced by Donald Trump at the beginning of April.

14:30 (U.S. time) – May CPI data:

- CPI (MoM): forecast 0.2%; previous 0.2%

- CPI (YoY): forecast 2.5%; previous 2.3%

- Core CPI (MoM): forecast 0.3%; previous 0.2%

- Core CPI (YoY): forecast 2.9%; previous 2.8%

The consensus expects a 0.2% monthly rise in the headline CPI and a 0.3% monthly increase in core inflation (excluding food and energy).

Tariff Impact

May marked the first full month of the trade war’s intensified phase, making this a key report for assessing how trade restrictions are influencing U.S. prices. It’s expected to show the first core inflation uptick of the year, highlighting the real inflationary impact of tariffs. For example, audio equipment prices have started rising at a record pace over the past two months. Increases are also spreading to furniture, clothing, electronics, and automobiles — all heavily import-dependent categories.

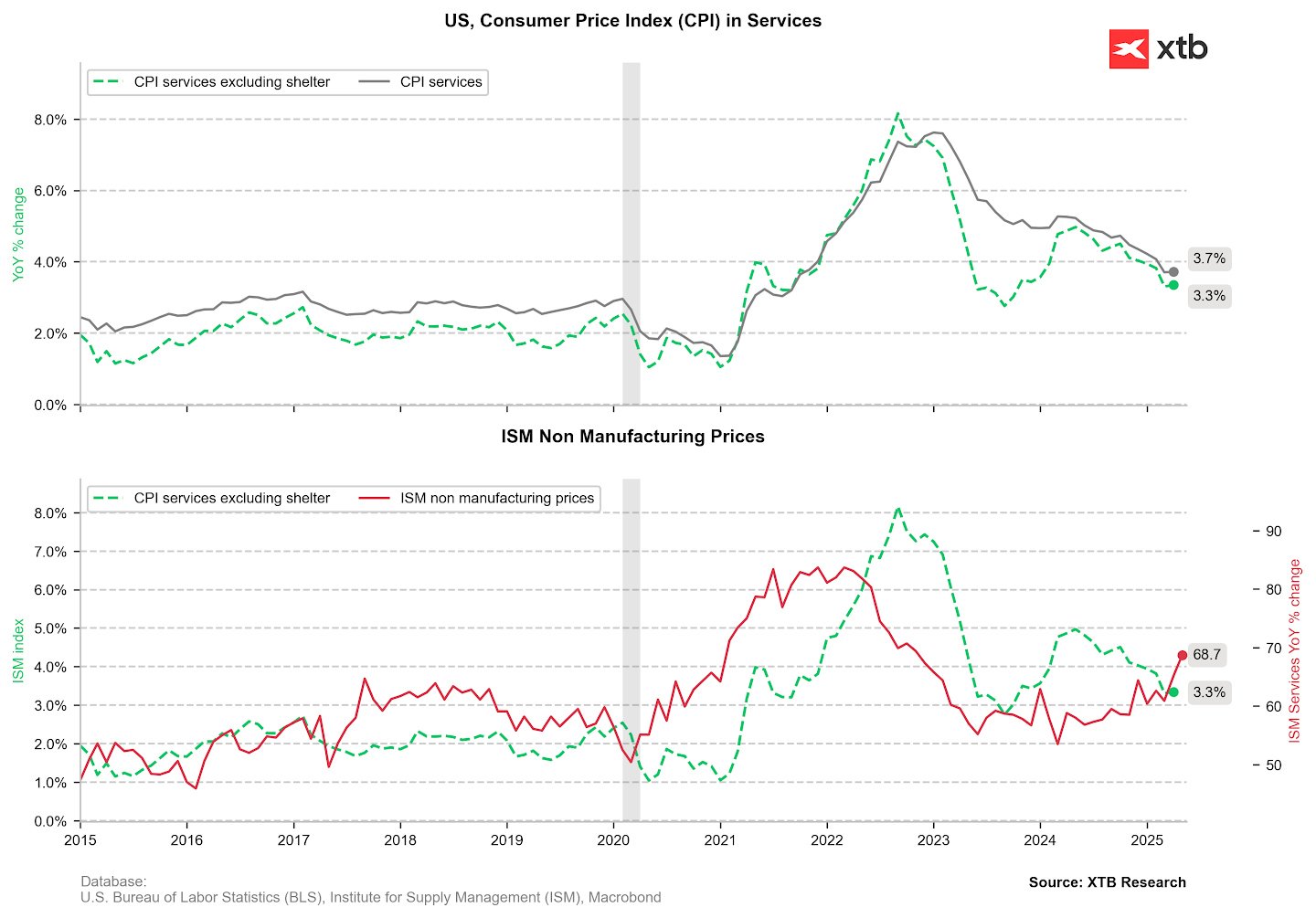

On the other hand, service inflation has continued to decline in recent months, particularly due to lower transportation inflation, driven by falling fuel prices. Meanwhile, food inflation has picked up again.

Although tariffs on many key products fell in May, this hasn’t yet translated into lower consumer prices. Price increases are still expected in major consumer categories.

Inflation Outlook (Charts & Data)

Service inflation has declined quite noticeably in recent months (excluding rent costs). On the other hand, businesses are signaling that inflationary pressure is rising, as reflected in regional indices and ISM indices. Source: Macrobond, XTB

The price subindex from the ISM services report points to clearly rising inflationary pressure, which may lead to a halt in the further decline of service inflation. Source: Macrobond, XTB

Although on a yearly basis fuel prices are the main factor behind limited inflation, fuel prices have remained stable in recent months. The indicated price subindex from the ISM services report suggests in advance that inflation may rebound in the near term. Source: Macrobond, XTB

Inflation will likely rebound anyway due to base effects (unless we see a clear month-over-month drop). However, if international trade factors have a greater impact on inflation in the coming months, inflation could rebound more strongly than the path assumed by the average monthly inflation rate of 0.1–0.2%. Source: Macrobond, XTB

EURUSD

Market reaction ahead of the report is mixed. The U.S. dollar is slightly weaker against the euro, and a similar pattern can be seen in equity futures, which are marginally down after yesterday’s gains. Alongside CPI, investors are also awaiting any updates from the two-day trade talks between China and the U.S. At the time of publication, EUR/USD is up 0.08% to 1.14336.

Oil rises over 3% 🛢️

Economic Calendar: Big Tech, Tensions Over Iran, and the ECB’s Decision ⏰

Morning Wrap: A New Threat of Conflict in the Middle East 🚨 (23.07.2026)

Tesla and Alphabet results round up

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.