Less than a month ago, the question of whether gold would reach $2,000 per ounce made definite sense. At the time, gold was testing the $1,800 area and was at its lowest since March of this year. An unexpected geopolitical event in the form of the conflict in the Middle East brought gold back under the close scrutiny of investors, and at one point it approached the indicated round level. In theory, we should be asking ourselves not if, but when gold will reach $2,000 per ounce, although in the near term the answer to this question may be complicated. The right question should be, when the Fed finally lets off the hikes and yields fall, will gold be able to reach new highs, well above $2,100?

Central banks are already reluctant to buy gold

The year 2022 was a record year for gold purchases by central banks. The beginning of this year was solid, but eventually demand from official institutions dropped significantly. On top of all this, we are seeing a further sell-off of gold from the vaults of ETFs, which have accounted for much of the investment demand for the shiny bullion in recent years. An expensive dollar and limited economic growth in Asian countries (mainly China and India) have also made jewelry demand look bad. On the other hand, a pretty high supply in the form of mining and recovery has resulted in an extremely high oversupply in the gold market for several years. So what justified the high gold prices?

Lots of money on the market and high inflation

The Covid pandemic prompted swift and significant action by central banks around the world. Huge "printing" resulted in a very strong rebound in inflation, which was further supported by a strong rebound in energy commodity prices after Russia's invasion of Ukraine. Central banks' balance sheets became so inflated that the market didn't know what to do with so much cash. Hence the very strong gains in the stock market, but also the rise in gold prices and keeping them at very high levels. high levels. It was only the central banks' balance sheet reductions (no debt rollover or even bond sales in the market) that caused gold to start losing noticeably. Add to this the sell-off from ETFs or the low interest of speculators in the futures and options market.

Now that inflation is no longer a problem, and central banks are reducing balance sheets, and interest rates are high, justifying high yields, gold should not be at such high levels. On the other hand, we have experienced such economic and geopolitical uncertainties that gold has returned to its original task of being a vehicle for storing value.

How long is risk able to keep gold prices high?

Looking at a number of different world events over the past nearly 40 years, one can see that elevated volatility in the gold market persists about 20 sessions after a given risk factor occurs. It is now more than 2 weeks since the start of hostilities between Israel and Hamas. Although there has not yet been a ground entry of the Israeli military into the Gaza Strip, the market has already stopped worrying about the conflict. Of course, it is not excluded that an escalation will still occur, but the impact of such events on the gold market is net neutral in the medium to long term. The outlook for the economy, inflation and ultimately interest rates will be needed for further pricing.

Is this the end of rate hikes?

The Fed will make its decision on interest rates on November 1. Rather, interest rates are expected to be kept unchanged and a possible hike in December, although statements from US central bankers do not provide clear answers. The economy appears to be strong, although clearly cooling. Nevertheless, there is a strong possibility that the Fed will eventually see the huge risks that go with excessive increases in yields. These are causing the United States to pay gigantic interest rates on a gigantic debt of more than $33 trillion. The economy needs lower interest rates to avoid drowning, even if the risk of high inflation still remains quite high.

What then awaits us in the gold market?

It seems that gold is currently overbought - high interest rates, further reduction of balance sheets, weak fundamentals in the form of low demand, or even an expensive dollar. All this does not speak for gold. In addition, gold reacted with growth to the recent escalation of the geopolitical conflict in the Middle East. All this speaks in favor of a possible correction.

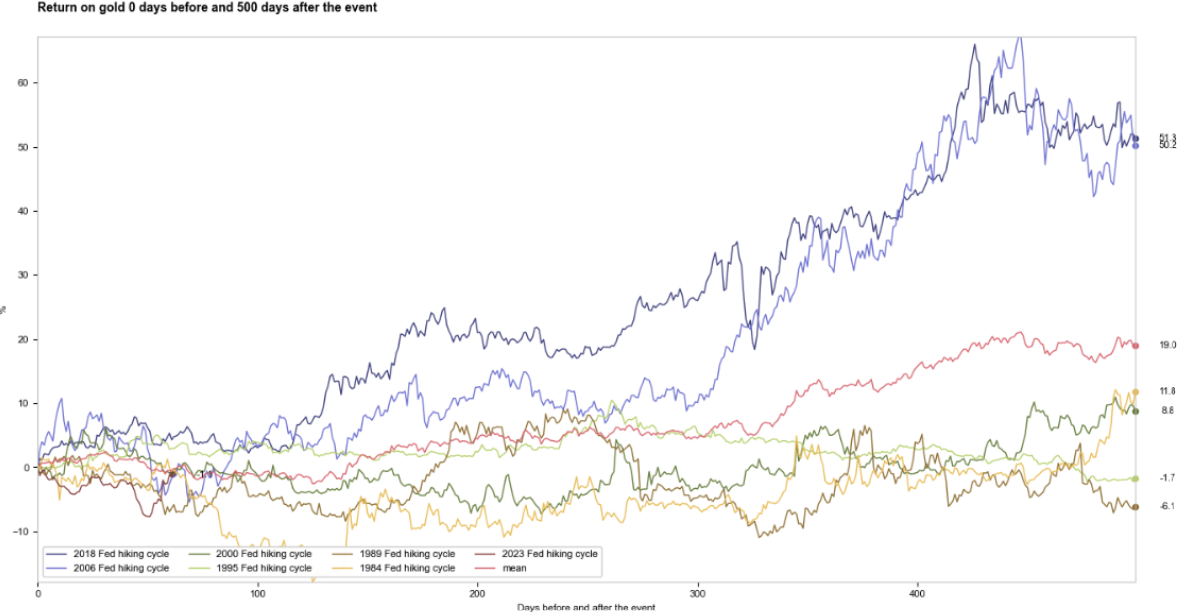

On the other hand, looking at the long term, it seems that investors will once again believe in gold and its properties of protection against inflation or other economic or geopolitical problems. Statistics make it clear that one or two years after the last Fed hike, gold is overwhelmingly gaining. That's why there's a chance that speculators will use the recent overbought condition to bring the gold price lower so that they will have an opportunity to take a larger and longer-term position later, and gold should even go out to new historic highs when the next move from the major central banks is to cut interest rates.

Gold returns for two years after the last hike in the cycle. Source: XTB

XTB Research

When will the rise in oil prices reach us?

Daily Summary: Equities Diverge as Tech Lags, Europe Rallies on Earnings & PMIs (24.07.2026)

Three markets to watch next week (24.07.2026)

Oil Slides Ahead of the Weekend!

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.