Howmet Aerospace (HWM.US) is at the heart of one of the strongest aerospace & defense upcycles in recent years. The company has delivered a total return of more than 80% year-over-year, and its latest quarterly results have only reinforced the momentum. Fundamentals remain solid: cash flows are rising, the balance sheet is disciplined, and the market is now pricing in an almost flawless execution of the growth strategy.

In Q4, Howmet reported:

-

Non-GAAP EPS: $1.05 (vs. $0.97 consensus)

-

Revenue: $2.2bn (+16% y/y)

-

Commercial Aerospace sales: +13% y/y

The market reaction was clearly positive, with the stock up nearly 10% following the release. The company also issued constructive guidance for 2026, calling for:

-

Revenue: approx. $9.1bn

-

Adjusted EPS: approx. $4.45

-

Free cash flow: approx. $1.6bn

On a full-year basis:

-

Revenue: +11% y/y to $8.25bn

-

Adjusted EBITDA: +26% y/y to $2.4bn

-

Adjusted EPS: +40% y/y to $3.77

-

Free cash flow: $1.43bn

At the same time, Howmet reduced its net debt-to-EBITDA ratio to 1.0x, paid down part of its debt, executed share buybacks, and raised its dividend significantly—underscoring the quality and resilience of its cash generation.

Fundamentals: strong demand in a cyclical environment

Howmet’s growth is supported by:

-

Sustained demand in commercial aviation and high product quality

-

A dynamic defense segment (Defense Aerospace +21% y/y in 2025)

-

Rising defense budgets in the US and Europe

-

Operating leverage alongside double-digit revenue growth

At the same time, the company is maintaining elevated capital expenditure, which may limit near-term FCF growth but strengthens its competitive position over the longer term. With 2026 EPS expected around $4.45–$4.50, the market values Howmet at over 50x forward 12-month earnings, while the trailing P/E exceeds 60x. These multiples are typical of high-growth technology names rather than a traditional aerospace components manufacturer—even one operating with exceptional efficiency. Assuming long-term EPS growth in the high-teens, current multiples still imply a very optimistic scenario of a continued upcycle with limited disruption.

Key risks to monitor

-

Potential volatility in defense spending

-

Risk of slower deliveries in key programs (e.g., the F-35)

-

Competitive pressure in aerospace components

-

Elevated capex if the cycle weakens

-

Escalation of trade tensions and the impact of tariffs

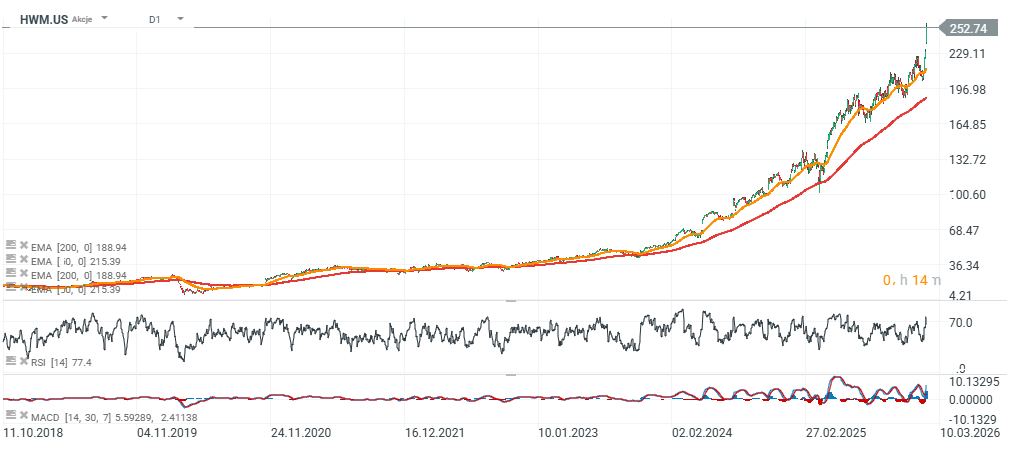

Technical picture and sentiment

Momentum remains exceptionally strong, with the stock at all-time highs and clearly above long-term moving averages. Such a setup often attracts momentum capital and can sustain the trend even at premium valuations. On the other hand, a significant distance from the 200-day moving average increases vulnerability to a correction if sentiment turns.

Howmet Aerospace remains one of the leaders of the current aerospace & defense cycle. Fundamentals are strong, the balance sheet is healthy, and earnings growth is robust. However, the valuation requires continued near-perfect execution and a supportive macro and defense-budget backdrop. From an analytical perspective, this is a high-quality operator—but at current multiples, the market has already priced in much of the upside scenario. The next leg for the stock will likely depend on the durability of the commercial and defense aviation cycle and Howmet’s ability to sustain its current pace of earnings growth.

Source: xStation5

Oil prices jump as markets wait for key earnings releases

Chart of the Day: AI supports gains – can Tesla and Google sustain them? (22.07.2026)

Economic Calendar: Time for Tesla and Google Earnings (22.07.2026)

Morning Wrap: AI companies and gold back in favour? (22.07.2026)

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.