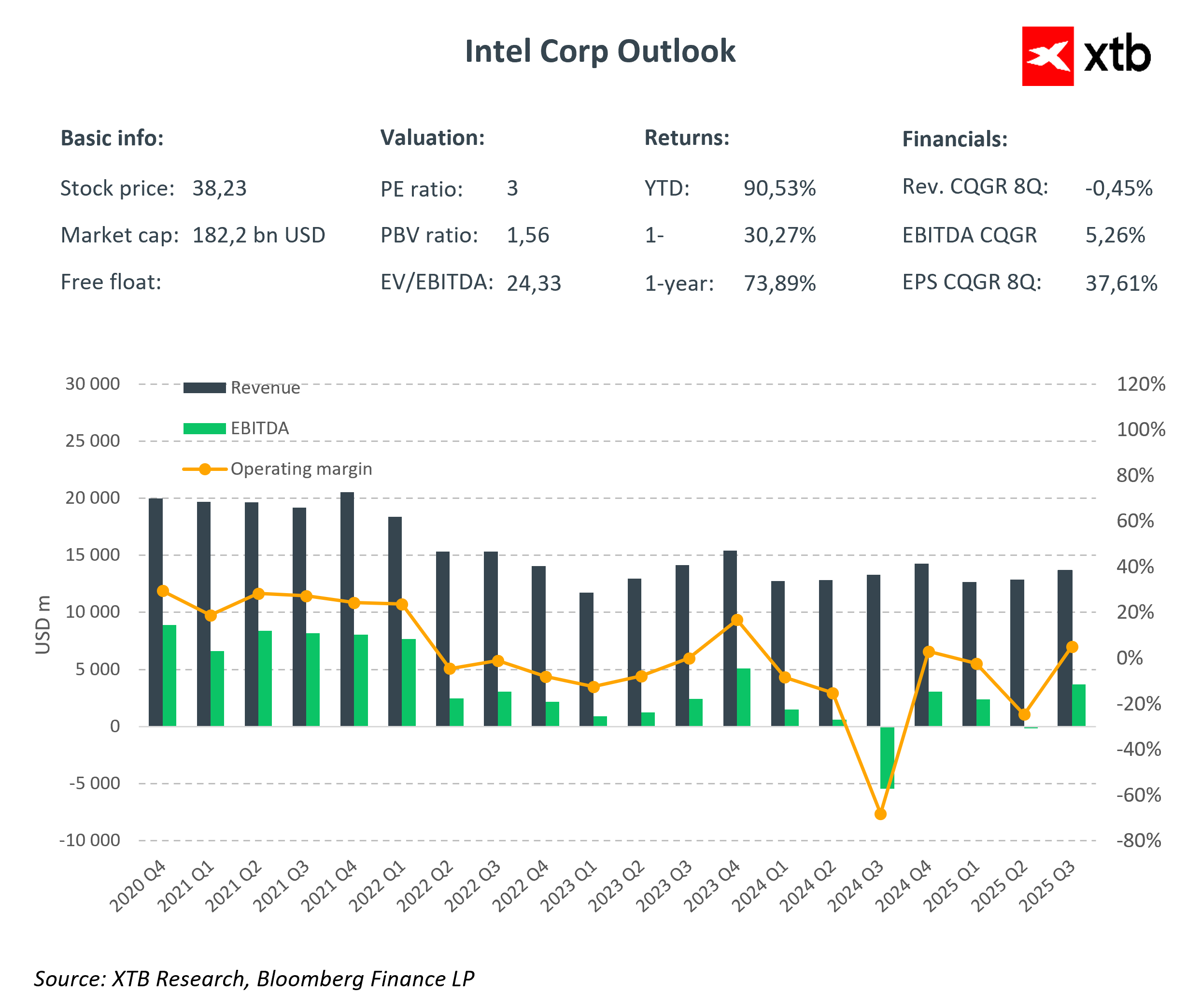

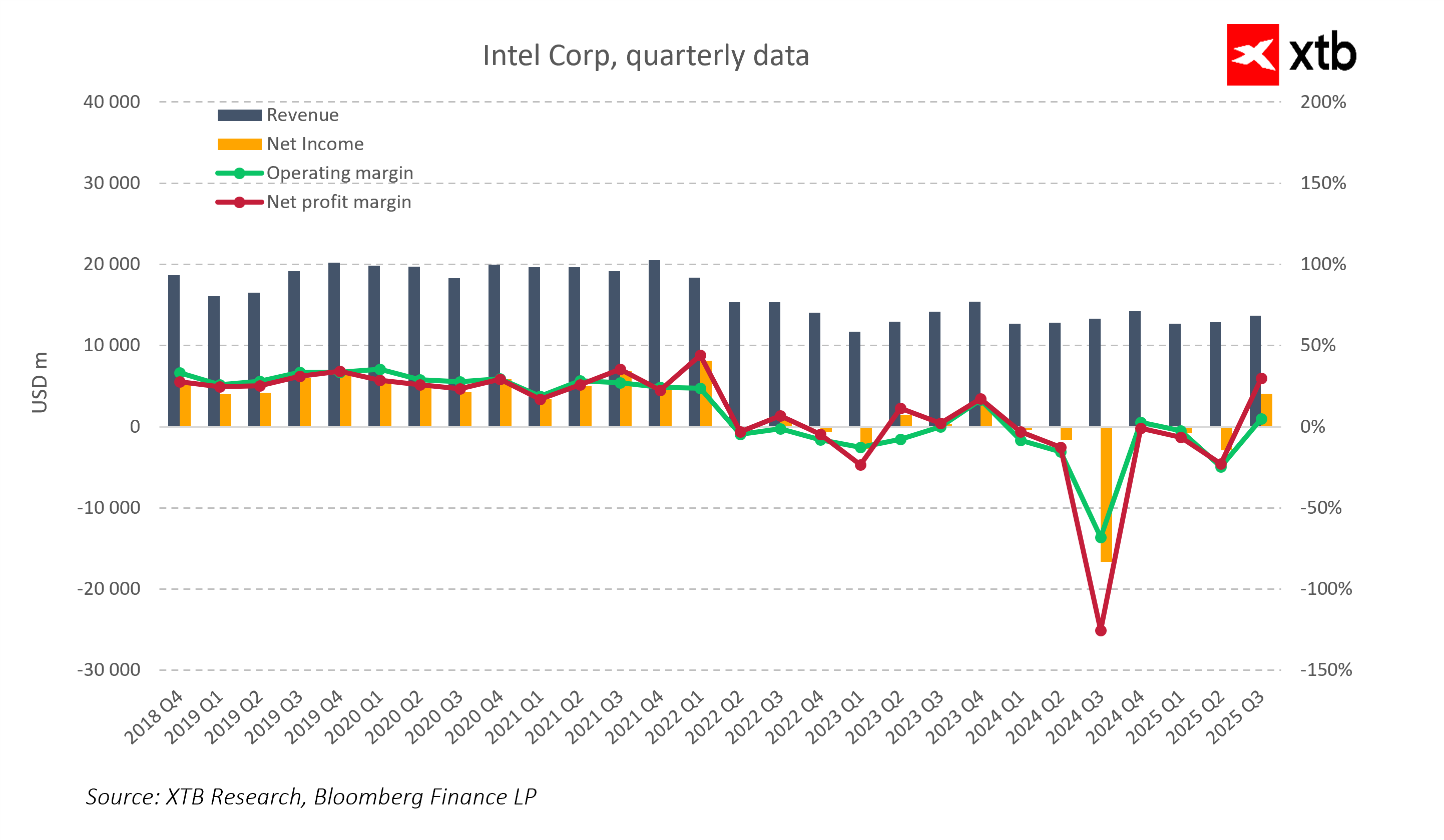

- Intel returns to profitability, achieving Q3 2025 revenue of $13.7B and net income of $4.1B (EPS $0.90), confirming the effectiveness of restructuring.

- The company invests in AI, foundry services, and advanced production processes, supported financially by the U.S. government, Nvidia, and SoftBank, strengthening high-margin segments.

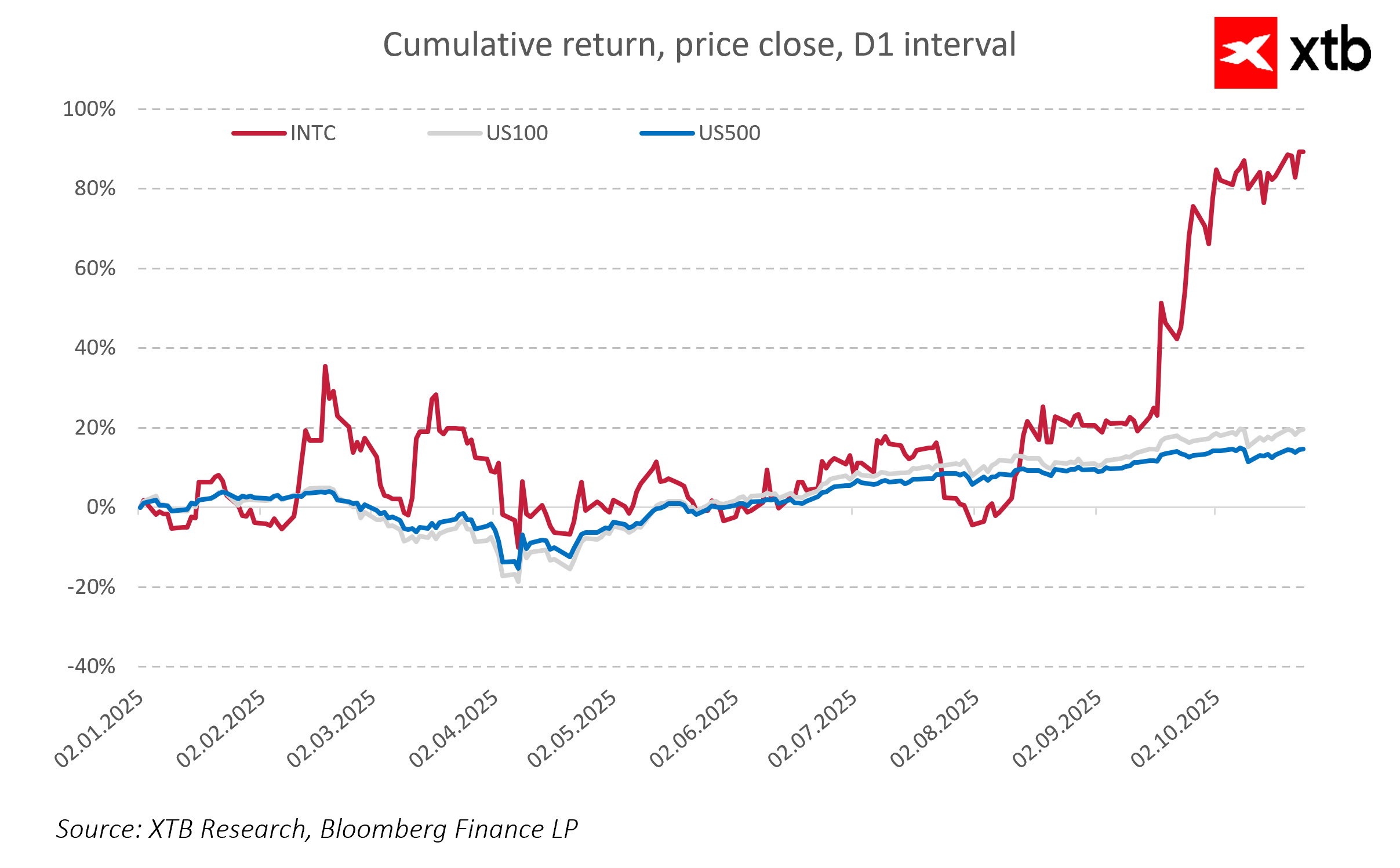

- Q4 2025 guidance: revenue of $12.8–13.8B and non-GAAP EPS of $0.08; investors are confident in the recovery’s success, reflected in stock performance exceeding benchmarks.

- Intel returns to profitability, achieving Q3 2025 revenue of $13.7B and net income of $4.1B (EPS $0.90), confirming the effectiveness of restructuring.

- The company invests in AI, foundry services, and advanced production processes, supported financially by the U.S. government, Nvidia, and SoftBank, strengthening high-margin segments.

- Q4 2025 guidance: revenue of $12.8–13.8B and non-GAAP EPS of $0.08; investors are confident in the recovery’s success, reflected in stock performance exceeding benchmarks.

Intel is rebounding after a period of challenges and transformation, rebuilding its market position and investor confidence. The results for the third quarter of 2025, published on October 23, show a clear sign of stabilization, as the company reported growth in both revenue and net income, confirming the effectiveness of its restructuring efforts.

Intel is focusing on strategic areas for future growth, such as artificial intelligence, foundry services, and operational cost optimization. A key element of this strategy has also been significant capital investments, including $8.9 billion from the U.S. government, $5 billion from Nvidia, and $2 billion from SoftBank, which strengthened the company’s liquidity and support the development of key technology projects.

This commentary takes a closer look at Intel’s Q3 2025 financial results, examines the factors influencing the current figures, and reviews initiatives aimed at maintaining a positive trend in the coming months.

Financial Results

-

Revenue: $13.7 billion, up 3% year-over-year. Revenue growth was driven primarily by rising demand for data center chips and a gradual recovery in the PC segment, which is slowly stabilizing after a period of slowdown.

-

Net Income: $4.1 billion ($0.90 per share), returning to profitability after last year’s loss of $16.6 billion. The result exceeded analyst expectations, confirming the effectiveness of cost-cutting measures and margin improvements.

-

Gross Margin: 38.2% (non-GAAP 40%), a significant increase compared to last year’s 15%. Margin growth was driven by both production cost reductions and a higher revenue share from high-margin segments, including data centers and AI-supporting chips.

Key Factors Driving Results

-

Operational Cost Reduction: Lowering operating expenses by approximately 20% to $4.4 billion improves efficiency and allows savings to be redirected to the development of new technologies, including the 18A production process and AI solutions.

-

Strategic Support: Intel secured $8.9 billion from the U.S. government, $5 billion from Nvidia, and $2 billion from SoftBank, accelerating investments in fabs, innovative technology development, and strengthening its position in the foundry services segment.

-

High-Margin Segment Growth: Strong demand for data center and AI chips boosts Intel’s margins, enabling the company to compete in key technology areas and support long-term revenue growth.

-

PC Market Stabilization: Higher revenue in the Client Computing Group indicates a gradual recovery of the PC market and Intel’s return to laptop and desktop market share, strengthening the company’s revenue base.

Outlook for Q4 2025

Intel expects revenue between $12.8 and $13.8 billion and non-GAAP EPS of around $0.08. For the full year, the company plans to invest approximately $27 billion in capital expenditures. In Q3 2025, GAAP EPS was $0.90, confirming a return to profitability after a period of losses.

The Q3 2025 results confirm the effectiveness of Intel’s restructuring and the rebuilding of investor confidence. Improving profitability, better cost control, and stabilization in key business segments indicate the company is entering a phase of sustainable improvement. Rising sales in AI and data center areas show that Intel is successfully adapting to the latest technology trends and turning them into a real competitive advantage.

Despite challenges in implementing new production processes and strong competition in the semiconductor market, the company shows clear signs of stabilization and determination to continue growing. Intel is increasingly seen as an example of a company that, through consistent restructuring, strategic partner support, and focus on innovative, high-margin business segments, can rebuild its industry position. Importantly, investors appear confident that Intel’s recovery will succeed. Since the beginning of 2025, the company’s shares have significantly outperformed major market benchmarks, reflecting growing market conviction that the strategy is delivering expected results.

Daily Summary: Wall Street Regains Ground; Another Intervention in the Yen Market❓

Three Markets to Watch Next Week (July 31, 2026)

What July can tell us about where stocks go next

Market Wrap: European equities at 3-week highs! Apple dips in US premarket!

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.