- Micron previously stated that its entire HBM memory production for calendar year 2026 has already been sold out.

- Wall Street consensus estimates call for approximately 280% year-over-year revenue growth and nearly 967% year-over-year EPS growth.

- During its previous earnings call, management indicated that the shortage of advanced AI memory products could persist beyond 2026.

- Implied volatility on Micron options is currently at its highest level in roughly two years, signaling extremely elevated expectations for a significant post-earnings stock move.

- Micron previously stated that its entire HBM memory production for calendar year 2026 has already been sold out.

- Wall Street consensus estimates call for approximately 280% year-over-year revenue growth and nearly 967% year-over-year EPS growth.

- During its previous earnings call, management indicated that the shortage of advanced AI memory products could persist beyond 2026.

- Implied volatility on Micron options is currently at its highest level in roughly two years, signaling extremely elevated expectations for a significant post-earnings stock move.

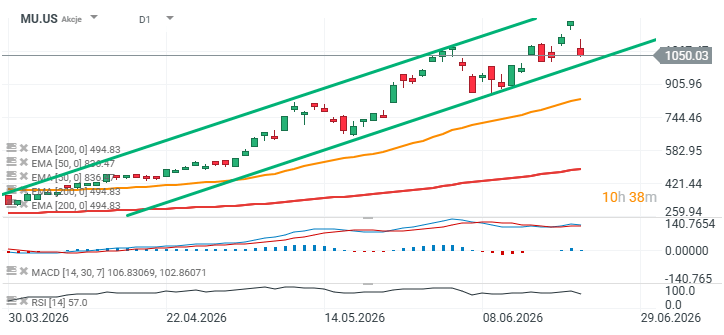

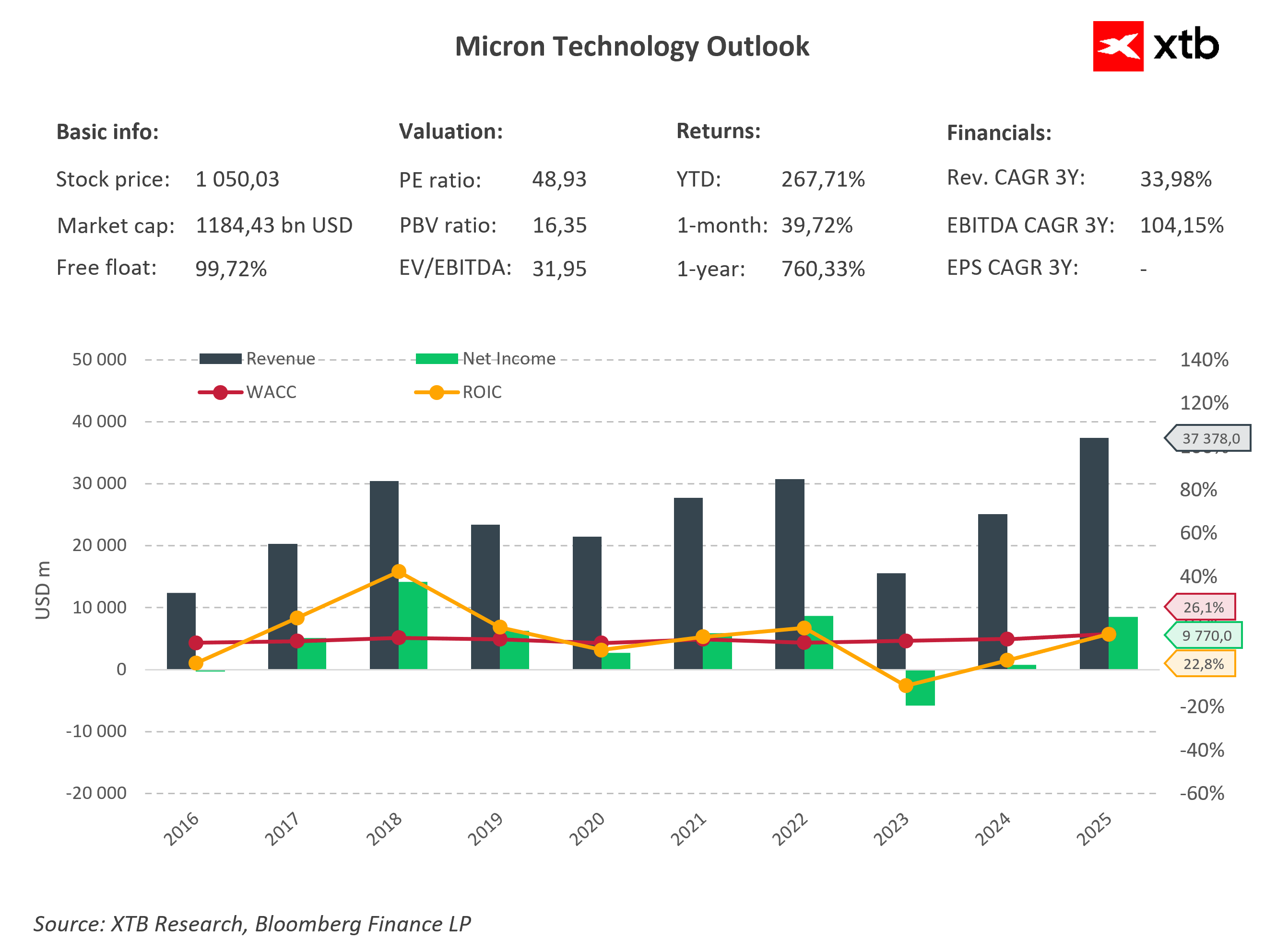

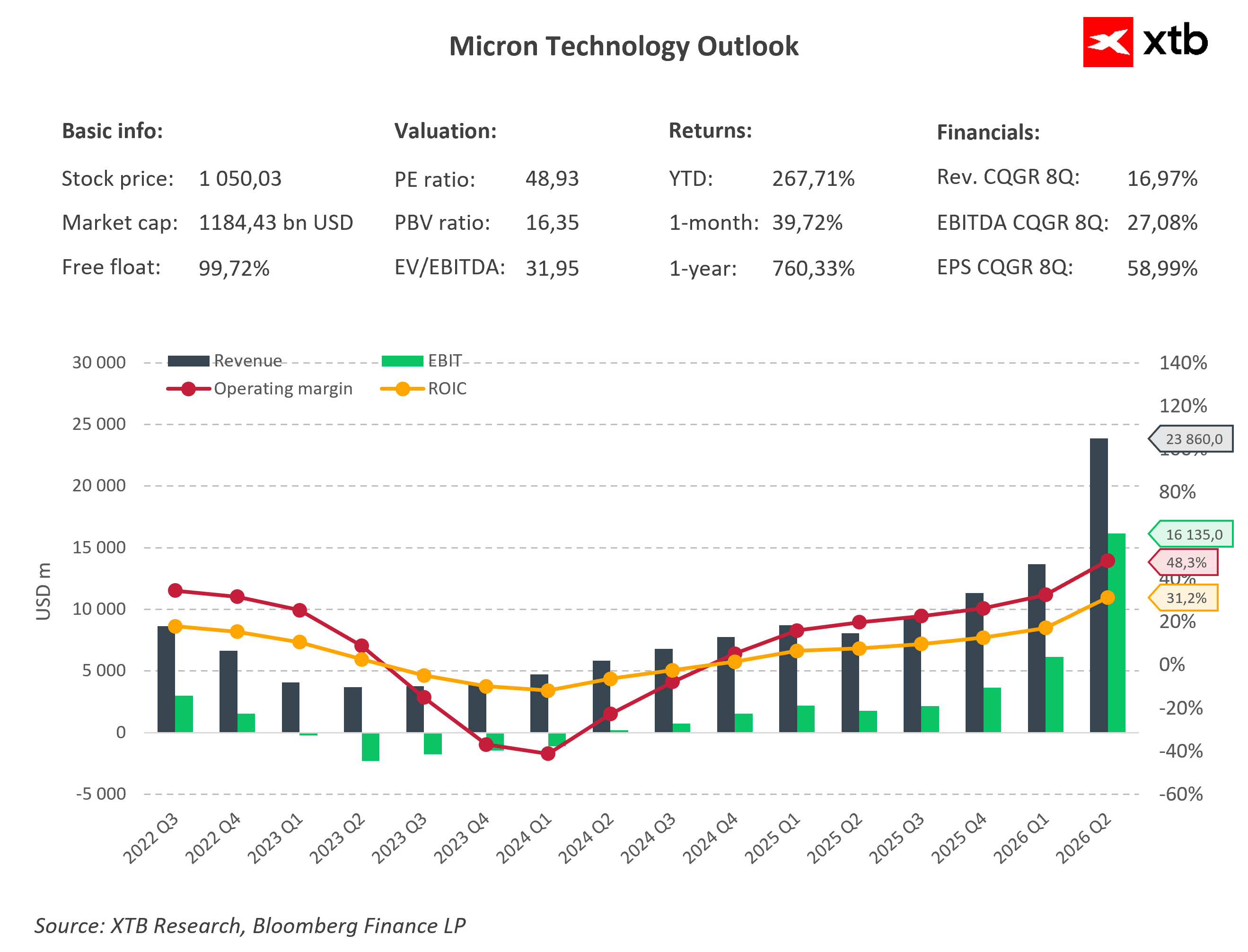

Following a sharp decline of more than 13% in Micron shares and a broad selloff across the semiconductor sector, investors are eagerly awaiting the company's fiscal third-quarter 2026 results, scheduled for release after the market close on June 24. Expectations are exceptionally high, with Wall Street forecasting revenue of approximately $35.3–35.4 billion and earnings per share above $20, marking another quarter of record-breaking growth driven by the artificial intelligence boom. Demand for high-bandwidth memory (HBM) used in AI accelerators remains the key growth driver, while Micron previously stated that its HBM production capacity for 2026 has already been fully allocated. However, investors will focus not only on the headline results but, more importantly, on fourth-quarter guidance and management's commentary regarding supply and demand trends in the DRAM and NAND markets. After the stock has surged more than 1,000% since April 2025, investors are looking for confirmation that the AI investment cycle continues to accelerate rather than approaching a saturation point. As a result, Micron's earnings report could either serve as a catalyst for a renewed rally across the AI sector or trigger another wave of profit-taking.

What Will the Market Focus on Most?

-

Revenue and earnings guidance for the fourth quarter, as well as outlook commentary for fiscal 2027.

-

Growth trends in HBM shipments and demand from AI infrastructure and data center customers.

-

Whether Micron can maintain its record-high gross margin, previously guided at around 81%.

Micron Earnings as a Test of the AI Bull Market

Micron is set to report fiscal third-quarter results at a time when the semiconductor sector is facing mounting pressure following a sharp selloff in AI-related stocks. As a result, the report will not be judged solely on revenue and earnings figures but also on whether demand for AI infrastructure remains strong enough to justify the sector's elevated valuations.

The Market Is Looking for More Than Just Record Results

Consensus estimates call for revenue of approximately $35.3–35.4 billion and earnings per share above $20, representing extraordinary year-over-year growth. However, expectations have risen so dramatically that simply beating forecasts may no longer be enough. Investors will be looking for evidence that growth can remain strong in the coming quarters.

HBM Remains the Core of the Micron Growth Story

The most important part of the report will be the company's HBM business, which supplies advanced memory solutions used in AI accelerators. Micron has previously indicated that its HBM capacity for 2026 is already fully booked, making any updates on customer demand, shipments, pricing, and future capacity expansion particularly important.

Margins Will Reveal the Industry's Pricing Power

Micron previously guided for a gross margin of around 81%, which would represent one of the highest profitability levels in the company's history. Maintaining or further expanding margins would reinforce the view that tight supply conditions across DRAM, NAND, and HBM markets continue to strengthen Micron's pricing power.

Guidance May Matter More Than the Results Themselves

The market is likely to place greater emphasis on fourth-quarter guidance and management's outlook for fiscal 2027 than on the reported numbers themselves. If guidance points to continued acceleration in AI and data center demand, the report could help restore confidence across the semiconductor sector. Conversely, a more cautious tone could intensify concerns that the AI investment cycle is beginning to cool.

Options Market Positioning Could Limit the Post-Earnings Reaction

Beyond the fundamentals, investors will also be closely watching options market positioning, which appears unusually stretched ahead of the earnings release. Implied volatility for Micron options is currently at its highest level in roughly two years, reflecting elevated expectations for a significant post-earnings move. At the same time, positioning remains heavily skewed toward call options, similar to the setup seen before Micron's March earnings report, when the stock declined despite delivering strong results.

The largest concentration of call options is clustered around the $1,200 level, which could act as a near-term resistance zone. In a bullish scenario, market makers may sell shares as the stock approaches this level, potentially limiting upside momentum. Meanwhile, implied volatility is expected to collapse following the earnings release, which historically has led to rapid option premium decay and increased profit-taking activity. Ultimately, the stock's reaction may depend as much on options market dynamics as on the earnings results themselves.

Source: xStation 5

Source: XTB Research

Source: XTB Research

AMD Did Everything Right… But Only Right

SpaceX Shares Drop 6% After Earnings 🚩 Is Space No Longer Enough for Wall Street?

Daily Summary: Nasdaq 100 Up 3.2% – Is the Bull Market Back? (04.08.2026)

US Open: S&P 500 at ATH, Strait of Hormuz nearing reopening, Palantir up 23%

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.