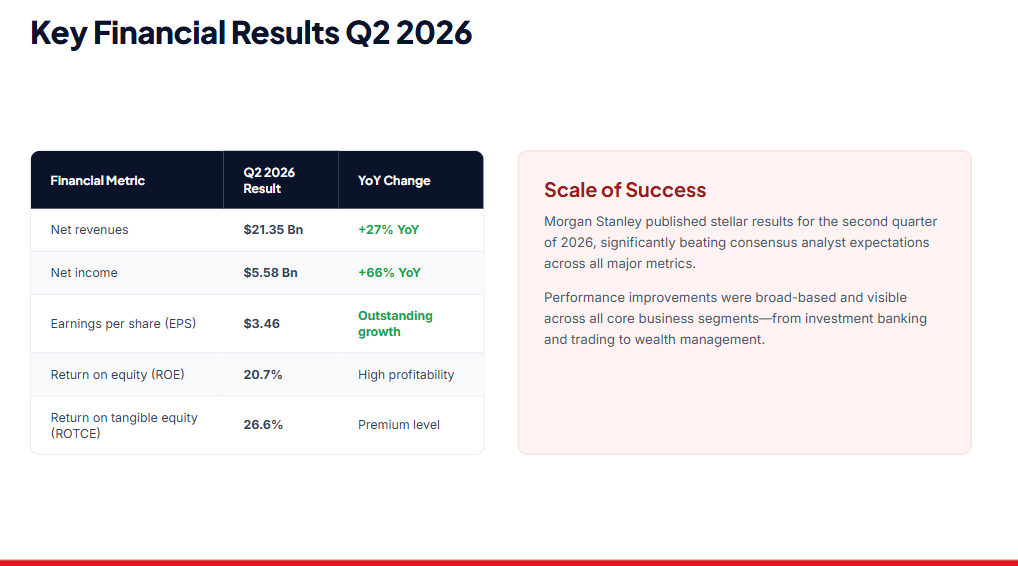

Morgan Stanley delivered outstanding results for the second quarter of 2026, significantly exceeding analysts’ expectations in both revenue and net income. The bank reported record revenues of $21.35 billion, while net income climbed to $5.58 billion, marking one of the strongest performances in recent years. The improvement was visible across virtually all key business segments, including investment banking, trading, wealth management, and asset management.

However, the numbers themselves are not the only impressive aspect of the report. Morgan Stanley once again demonstrated that it has one of the most diversified business models among the world’s largest investment banks. In addition to its highly successful capital markets operations, the bank benefits from a massive wealth management division, which provides stable, recurring fee-based revenue streams. As a result, Morgan Stanley’s earnings are less dependent on short-term market conditions than many of its competitors.

Market reaction was clearly positive. Following the earnings release, Morgan Stanley shares gained more than 2% in pre-market trading. Investors appreciated not only the scale of the earnings beat but, more importantly, the quality of the results and the fact that improvement was visible across nearly all major areas of the business.

Key financial highlights

-

Net revenues: $21.35 billion (+27% YoY)

-

Net income: $5.58 billion (+66% YoY)

-

Earnings per share (EPS): $3.46

-

Return on equity (ROE): 20.7%

-

Return on tangible common equity (ROTCE): 26.6%

-

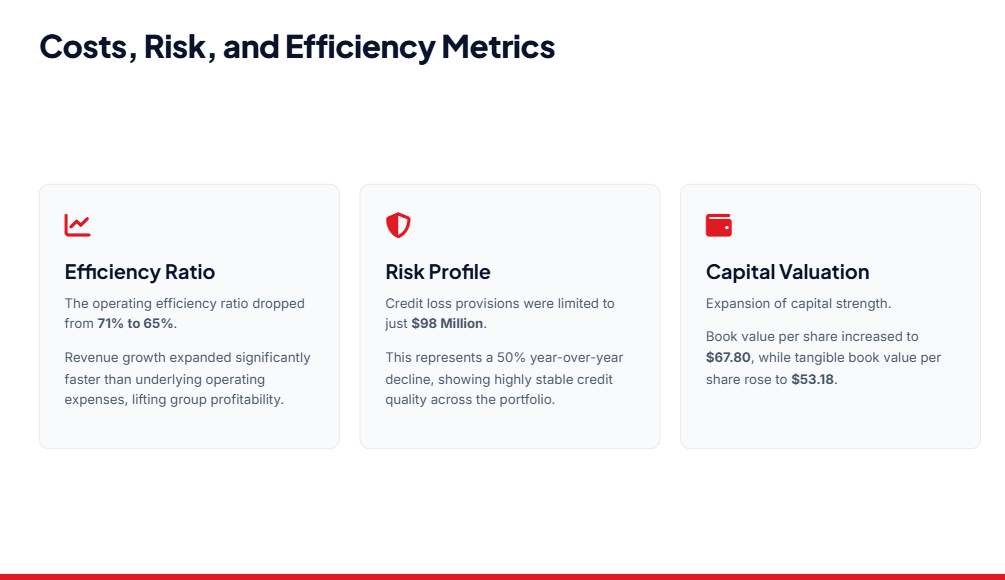

Efficiency ratio: 65% (compared with 71% a year earlier)

-

Provision for credit losses: $98 million

-

Book value per share: $67.80

Financial performance and profitability

The most impressive aspect of Morgan Stanley’s results is the pace of profitability improvement. Revenues increased by 27% year over year, while net income surged by 66%, showing that the bank was able to effectively capitalize on the favorable market environment. Revenue growth translated into an even faster increase in earnings, highlighting both strong operational efficiency and disciplined cost management.

The bank’s strong financial position is further confirmed by a 20.7% return on equity. These are levels achieved by the most profitable financial institutions globally and demonstrate that Morgan Stanley is using shareholder capital extremely efficiently.

Another important factor was the improvement in the efficiency ratio, which declined from 71% to 65%. This means revenues grew significantly faster than operating expenses, resulting in a clear improvement in overall profitability across the group.

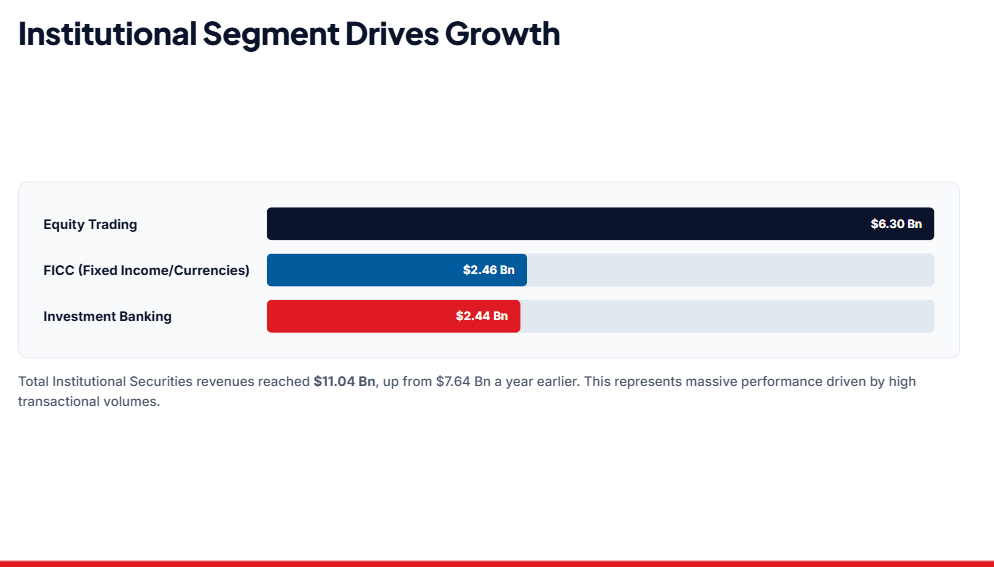

Institutional Securities segment once again drives growth

The largest contribution to Morgan Stanley’s results came from the institutional business, which generated $11.04 billion in revenue, compared with $7.64 billion a year earlier. This segment benefited the most from improving conditions across global capital markets.

Key segment results:

-

Investment banking: $2.44 billion

-

Equity trading: $6.30 billion

-

Fixed Income, Currencies and Commodities (FICC): $2.46 billion

The very strong investment banking performance points to continued recovery in mergers and acquisitions activity as well as securities issuance. At the same time, sustained high institutional client activity supported trading revenues, particularly in equities.

The combination of rising transaction volumes and favorable financial market conditions allowed Morgan Stanley to achieve one of the strongest performances in this segment in many quarters.

Wealth Management remains Morgan Stanley’s key competitive advantage

While the Institutional Securities segment is responsible for driving earnings growth, the Wealth Management division is the foundation of Morgan Stanley’s stability. In the second quarter, the segment generated $8.86 billion in revenue, confirming its position as one of the bank’s most important business pillars.

Key figures:

-

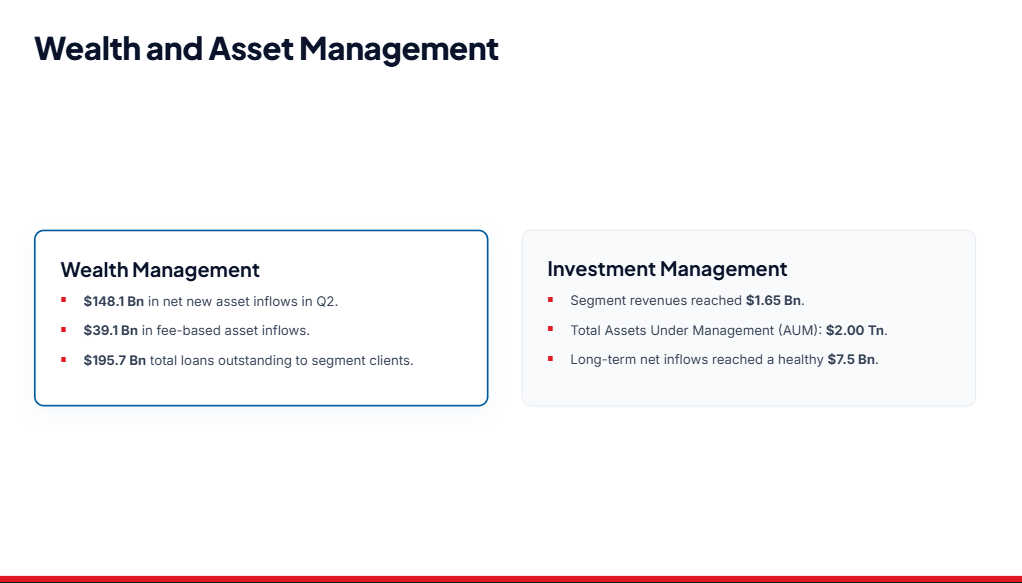

Client assets under fee-based management: $3.02 trillion

-

Net inflows into fee-based assets: $39.1 billion

-

Net new assets: $148.1 billion

-

Client loans: $195.7 billion

This segment is what sets Morgan Stanley apart from many of its competitors. Its enormous client asset base generates stable fee-based revenues that are significantly less sensitive to short-term market fluctuations than trading or investment banking activities.

The very strong inflows of new assets also show that the bank continues to successfully attract new clients and increase the value of assets entrusted to its management. This is a positive signal for investors, as it creates potential for further revenue growth in future quarters.

Asset Management maintains steady growth

The third major pillar of Morgan Stanley’s business remains its Asset Management division, which generated $1.65 billion in revenue. Assets under management increased to $2.00 trillion, while long-term net inflows reached $7.5 billion.

Although this segment represents the smallest share of group revenues, its importance continues to grow. Expanding assets under management increase the contribution of stable fee-based revenues and further improve the overall quality of Morgan Stanley’s business model.

Costs, risk and capital position

Operating expenses increased alongside the growth of the business, but the pace of cost growth remained significantly below revenue growth. As a result, Morgan Stanley improved operational efficiency and increased profitability.

The quality of the loan portfolio also remains strong. Provisions for credit losses totaled only $98 million, half the level recorded a year earlier. Such a low level of provisions suggests that borrowers remain in a stable financial position and that the bank is not experiencing any meaningful deterioration in asset quality.

Why did the market react so positively?

Following the earnings release, Morgan Stanley shares moved higher in pre-market trading. Investors responded positively not only to the scale of the earnings beat but, above all, to the underlying quality and structure of the results.

The bank delivered strong growth in investment banking, record equity trading results, continued expansion of wealth management, high returns on capital, and improved cost efficiency. Equally important, very low credit provisions confirmed the strength of the loan portfolio and the absence of significant signs of stress among clients.

Compared with other major Wall Street banks, Morgan Stanley stands out because its earnings growth does not rely on a single source of revenue. Strong capital markets activity supports trading and investment banking, while the massive wealth management business provides stable and recurring income streams.

This diversification is exactly why investors increasingly view Morgan Stanley as one of the banks best positioned to benefit from the current recovery in financial markets.

Outlook

Morgan Stanley enters the second half of 2026 from a position of significant strength. If merger and acquisition activity remains elevated and investors continue to actively participate in capital markets, the bank has the potential to maintain strong performance in the coming quarters.

At the same time, the scale of the Wealth Management business reduces dependence on the economic cycle and enhances revenue stability. This makes Morgan Stanley one of the most diversified investment banks globally, allowing it to benefit both from improving Wall Street conditions and from the long-term growth of client assets.

What will we be watching in the next quarter?

Investors will focus on several key factors that will determine whether Morgan Stanley can maintain its strong momentum:

-

Whether the recovery in investment banking continues, particularly in mergers and acquisitions and securities issuance activity.

-

Whether the Wealth Management division maintains strong asset inflows and continues to expand fee-based assets.

-

Whether institutional client activity remains elevated and continues to support trading revenues.

-

Whether the bank can maintain high returns on capital while continuing to control operating expenses.

-

How management assesses the outlook for capital markets in the second half of the year and whether it maintains its positive view on the business environment.

Key takeaways

The second quarter of 2026 confirmed that Morgan Stanley is operating in a highly favorable phase of the current market cycle. The bank is benefiting simultaneously from the recovery in investment banking, strong trading activity, and continued expansion of its Wealth Management business, which provides a stable and recurring source of revenue.

Compared with other major financial institutions, Morgan Stanley stands out primarily because of the structure of its business model. Goldman Sachs remains a more direct beneficiary of improving capital markets activity, while Morgan Stanley combines strong exposure to Wall Street with one of the world’s largest wealth management businesses. This allows its results to be not only very strong but also more balanced and less vulnerable to changes in market conditions.

The combination of high profitability, growing client assets, strong cost discipline, and broad revenue diversification makes Morgan Stanley one of the best-positioned banks on Wall Street.

If the current market environment remains supportive throughout the second half of the year, the bank has solid foundations for further earnings improvement and continued high returns.

Source: xStation5

Stock of the Week: Arista Networks—A Second-Tier Technology with Top-Tier Results

US Open: S&P 500 shows strength as semiconductor lags 🚩 Western Digital down 12%

SoftBank earnings: Intel and AI are not enough?

Nasdaq 100 Slides Again 🚩 SanDisk Falls 10% After Earnings, Semiconductors Under Pressure

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.