-

-

Geopolitics – Iran/Israel escalation: On Sunday, Iran fired rockets toward Israel for the first time since the ceasefire began in April, citing U.S. violations of the naval blockade and activities in Lebanon. Israel responded with strikes on approximately 10 military targets in western and central Iran, ignoring Trump’s calls for restraint; rumors also reached the public regarding attacks launched from Yemen toward Israel and unconfirmed shelling of the Prince Sultan base in Saudi Arabia.

-

Geopolitics, continued – diplomatic deadlock: Trump publicly stated that Netanyahu “will have no choice” and must accept the deal – but an Iranian diplomat explicitly stated that a deal with Trump “is no longer possible at this stage.” The lack of a clear path to de-escalation is sustaining the risk premium in the markets.

-

Oil – a historic supply disruption: WTI is up by approx. +4.7% to ~$94.4, Brent by a similar margin to around $97; prices are simultaneously pricing in the Iran-Israel exchange of fire and the fact that the closure of the Strait of Hormuz has reduced actual OPEC+ production from 42.77 million b/d (February) to 33.19 million b/d (April)—the largest supply crisis in the organization’s history. OPEC+ is raising production limits by 188,000 b/d for the fourth consecutive time starting in July, but this is largely a “paper” decision—most members are unable to even reach their previous quotas.

-

Fed – shift from a pivot to rate hikes: May payrolls (+172,000, the third strong month in a row), combined with the energy shock from Iran, pushed the probability of a Fed rate hike before year-end to over 70–75% (vs. 45% a week earlier according to CME FedWatch). Goldman Sachs has pushed back the first rate cuts to 2027; Capital Economics explicitly forecasts two 25-bp hikes this year; Hammack of the Fed signals that with persistently high inflation, a hike may be necessary “soon.”

-

Wall Street on Friday – red dominates, but rotation is evident: The heatmap for Friday’s session shows a massive sell-off in tech: MU -13.25%, INTC -11.28%, AMD -10.86%, AVGO -7.92%, AMAT -9.71%, META -5.51%, MSFT -2.66%, NVDA -6.2%. A defensive rotation is clearly emerging—Healthcare remained in the green (JNJ +2.02%, WMT +4.09%, KO +3.46%, PG +4.09%), some Industrials (UNP +13.19%, ETN), and Transportation; this is a classic picture of a market shifting from “growth/momentum” to “value/defensive.”

-

Asia – Tech sell-off, KOSPI on the brink: The KOSPI fell by 8–8.4% at its peak (triggering a circuit breaker) and ended the session down about 5%—13% below last week’s record highs; foreign investors sold a net total of approximately $801 million in shares by noon local time alone. Nikkei -3.7%, Nikkei Tokyo Electron -6.7%, SoftBank -7.5%, TSMC -2.1%, TAIEX -3.9%; Nomura analysts point out that this is mainly “forced selling” following excessive positioning, not a shift in the long-term thesis on AI.

-

European futures ahead of the open: DAX/DE40 futures are down about 0.5% ahead of the open; EU50 similarly; European futures fell by ~1% in response to the Asian sell-off. The heavy exposure of European indices to the semiconductor (ASML, Infineon) and energy sectors suggests that the opening will be mixed: energy may gain, while tech/growth will remain under pressure.

-

Currencies – Dollar at two-month highs, yen under pressure: The DXY index at 100, EUR/USD slipped to around 1.1507 (two-month low), GBP/USD around 1.3316 (three-month low), AUD/USD at a two-month low of 0.7016. USD/JPY remains above 160 – the yen has erased the entire effect of the BoJ’s May intervention (11.7 trillion JPY); the market has largely priced in a single BoJ rate hike in June, so without signals of faster tightening, the yen will struggle to regain ground.

-

Gold – Yields Take Precedence Over Safe-Haven Status: Spot gold is down about 0.2% to $4,311–4,319/oz after Friday’s 3% drop (the lowest since March 24). Silver is stable at around $67.7, platinum is down 0.5%, and palladium is unchanged; the entire metals complex is losing the battle against rising real interest rates.

-

Cryptocurrencies and IPOs of the week: Bitcoin is rebounding after dipping below $60,000 on Friday (its sharpest weekly decline since the FTX collapse, -16%) – now trading around $62,600–$63,000 (+1.55%); Ethereum is up 3% to around $1,679.

-

This week’s focus will be on SpaceX’s Nasdaq debut on Friday (expected to be the largest IPO in history), CPI data (Wednesday), and PPI data (Thursday)—these three catalysts will set the tone for the coming weeks.

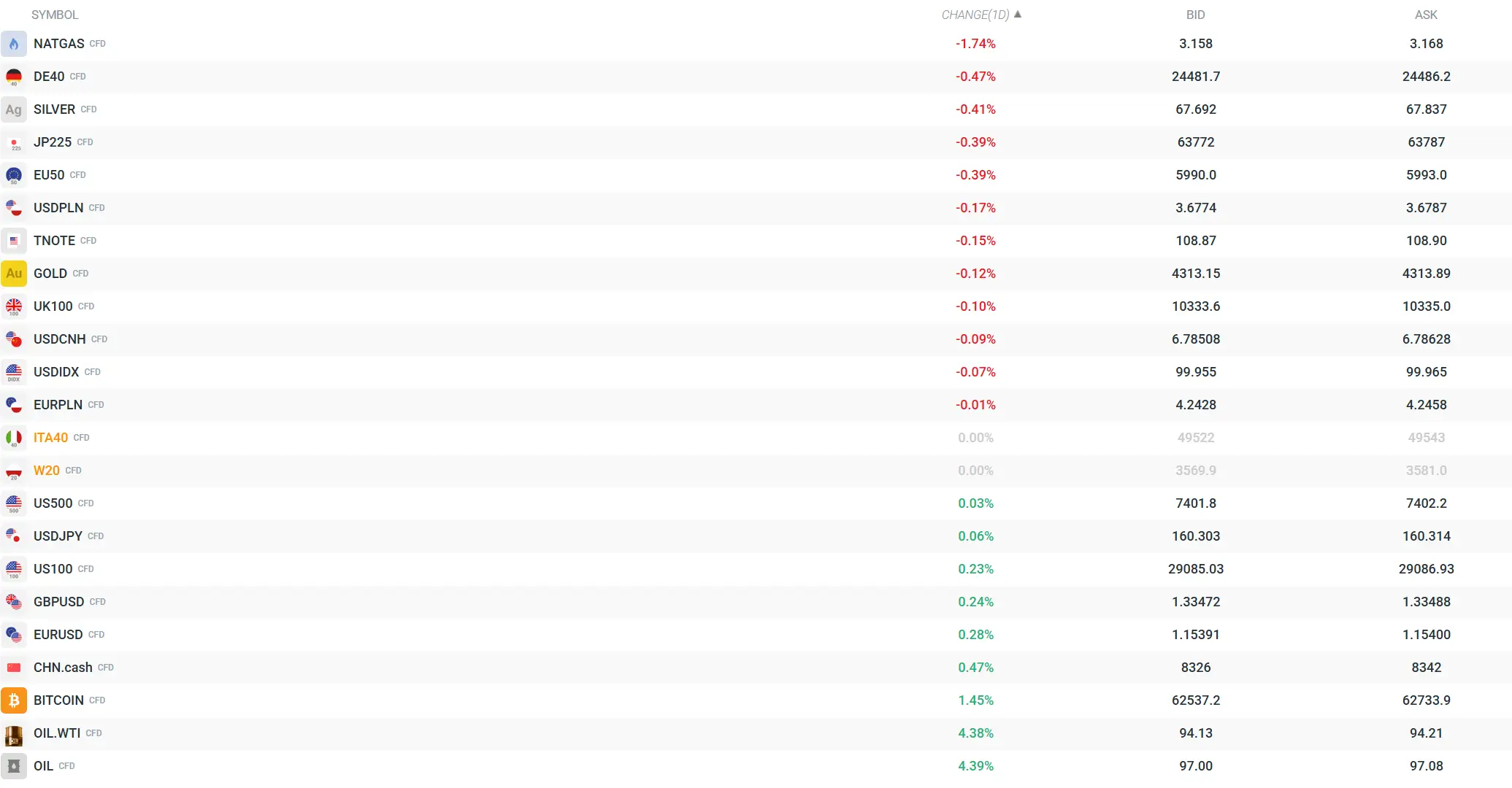

An overview of the prices of key financial instruments. Metals and stock markets under pressure. Oil prices surge on geopolitical developments. Source: xStation

-

Daily summary: Dollar rout after NFP, Gold back on the rise

Three markets to watch next week (07.08.2026)

The dollar sinks after labor market data💲📉

US OPEN: Shallow rebound in the shadow of a weak labor market

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.