Netflix shares plunged more than 9% after the market close, despite the company reporting solid results for the first quarter of 2026. The negative market reaction was mainly driven by more cautious forward guidance, which came in below expectations in several key areas. The most important Q1 figures were earnings per share and revenue - both beat market expectations, but this was not what investors focused on, as future outlook proved more critical. The streaming pioneer also announced that chairman and co-founder, Reed Hastings is stepping down from the board after 29 years.

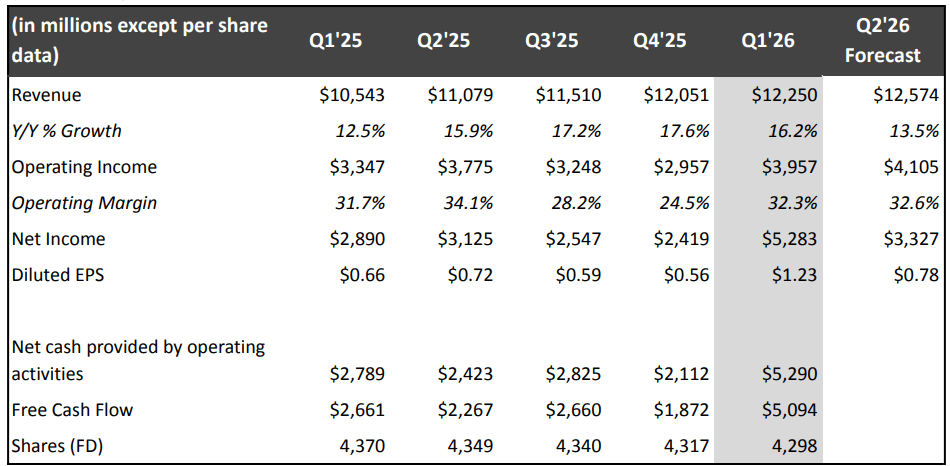

- EPS: $1.23 vs. $0.66 y/y

- Revenue: $12.25B vs. $12.17B expected

Other elements of the report present a more nuanced picture. Free cash flow reached $5.09B compared to expectations of $2.67B, representing a clear positive surprise. At the same time, guidance for the second quarter came in below consensus: the company expects EPS of $0.78 (vs. $0.84), revenue of $12.57B (vs. $12.64B), and operating income of $4.11B (vs. $4.34B). Operating margin is projected at 32.6%, compared to expectations of 34.4%.

For the full year, Netflix still anticipates relatively stable growth, although some metrics differ from market expectations. The company sees free cash flow at around $12.5B (previously about $11B; vs. $12.05B expected). Annual revenue is projected in the range of $50.7B to $51.7B (vs. $51.37B), implying growth of 12% to 14%. Full-year operating margin is expected at 31.5% (vs. 32%), while 2026 advertising revenue remains on track to reach around $3B. The market may have quietly hoped for an upward revision of this figure.

Record engagement with content?

Importantly, Netflix reached a record level of user engagement in Q1, which is one of the company’s key internal metrics for platform quality. The company is expanding into new content formats, including video podcasts and live events (such as the World Baseball Classic, which set viewership records in Japan). This indicates a shift beyond the traditional streaming model.

Netflix is also pushing further into gaming, launching a standalone app for children—signaling product diversification. At the same time, AI is becoming a core element of its technology strategy, highlighted by the acquisition of InterPositive (a GenAI tool for creators) and the use of AI to enhance user experience. This points to continued investment in production efficiency and personalization.

A redesign of the mobile app is also planned, including the introduction of vertical video formats, which may be a response to competition from platforms like TikTok. Recent price increases have been well received by the market, suggesting relatively low price sensitivity among users (pricing power). Netflix also emphasizes strong confidence in its long-term growth, referring to a “long runway of growth”—indicating further expansion potential. While acknowledging the highly competitive nature of the industry, the company highlights that its strategy is based on continuous product improvement and faster execution than its competitors.

Netflix key financial figures

Source: Netflix

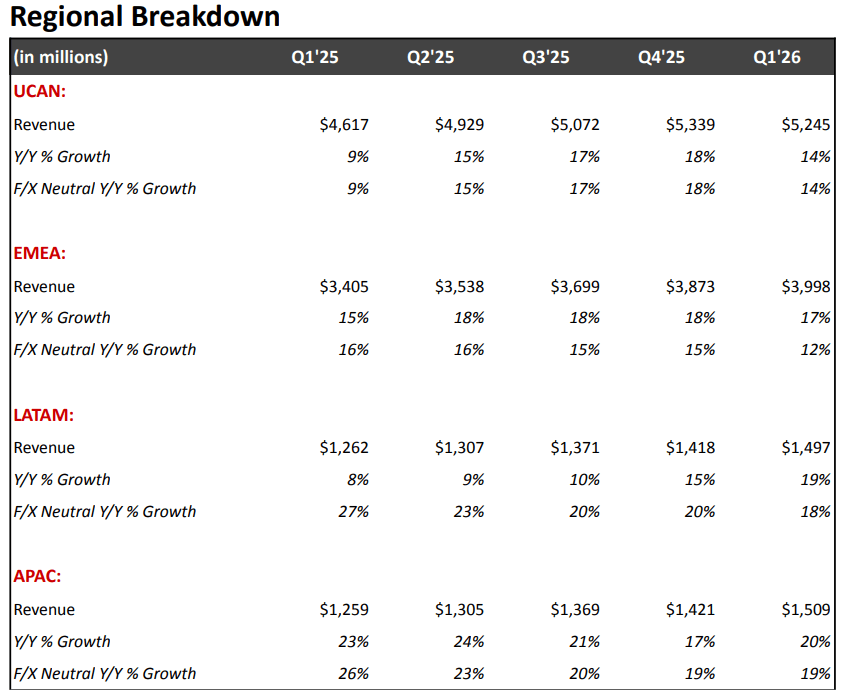

Netflix revenue breakdown by region

Source: Netflix

Key insights from the results

Revenue growth was driven by a combination of subscriber growth, price increases, and rising advertising revenue. This indicates that Netflix’s business model is becoming increasingly diversified.

- Foreign exchange (FX) had a positive impact on results, meaning that part of the revenue growth was supported not only by operational performance but also by macroeconomic factors.

- A significant portion of the EPS increase was influenced by a one-off $2.8 billion termination fee related to the Warner Bros. transaction, recorded under “interest and other income.” This suggests that part of the profit improvement is not recurring.

Operating margin is expanding year over year, confirming improving operational efficiency rather than just scaling effects. At the same time, Netflix is clearly communicating its financial priorities, pointing to a gradual shift away from a “growth at all costs” approach toward a more balanced model focused on:

→ revenue growth

→ operating margin

→ free cash flow

Advertising is becoming an increasingly important segment, with the company expecting it to nearly double in 2026, making it one of the key growth drivers. Content costs (content amortization) are expected to be front-loaded in the first half of the year, which explains weaker margins in Q2 and highlights cost seasonality. Netflix signals margin improvement in the second half of the year (Q3–Q4), suggesting that current cost pressures are temporary rather than structural. Revenue growth in Q2 is expected to remain solid (~13%), despite weaker profitability guidance, indicating a divergence between revenue dynamics and cost trends.

Key cash flow insights

The cash flow section shows that Netflix entered 2026 with a very strong liquidity position. Operating cash flow increased to $5.3 billion from $2.8 billion a year earlier, while free cash flow rose to $5.1 billion from $2.7 billion in the same period.

- This represents a significant improvement, although it is important to note that a large portion of the increase was driven by the one-off $2.8 billion termination fee related to the Warner Bros. deal. This means that while cash generation appears strong, not all of the improvement is recurring.

- The company also raised its full-year 2026 free cash flow guidance to approximately $12.5 billion from the previous $11 billion estimate, again largely due to this one-off effect. At the same time, Netflix has not changed its capital allocation approach.

- The company continues to prioritize reinvestment in the business—both organically and through selective M&A while maintaining liquidity, and only then returning excess cash to shareholders. This suggests that management remains focused on long-term growth and financial flexibility rather than short-term shareholder returns.

At the end of the quarter, Netflix reported $14.4 billion in gross debt and $12.3 billion in cash and cash equivalents. The elevated cash position reflects the earlier pause in share buybacks during the Warner Bros. transaction, followed by the receipt of the termination fee. After deciding not to increase its offer for Warner Bros., Netflix resumed share repurchases, buying back 13.5 million shares for $1.3 billion during the quarter, with $6.8 billion remaining under the current authorization. This highlights strong capital flexibility while maintaining a disciplined balance sheet approach.

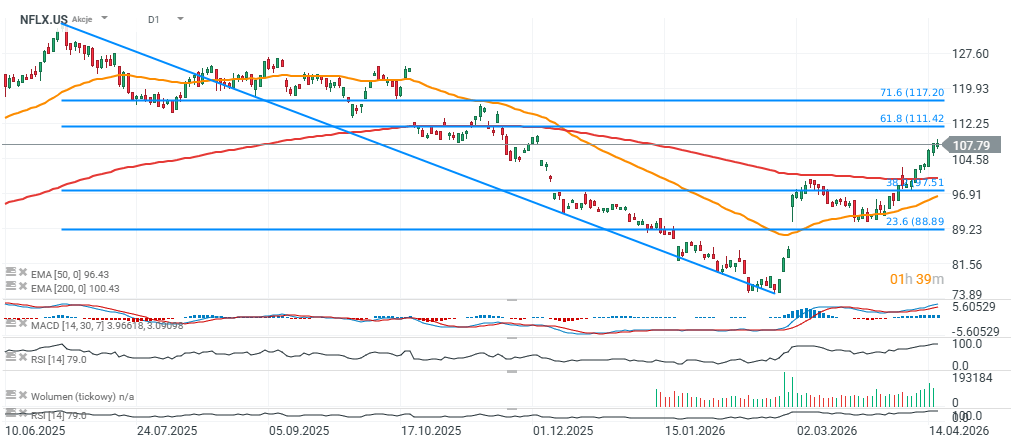

Netflix shares (D1 timeframe)

The after-hours reaction suggests that the price may retest the key support level tomorrow, defined by the 200-day EMA (red line) around $97 per share. Holding this level could indicate a return to upward momentum, while a break below it may be interpreted as confirmation of a prevailing downtrend - following nearly a 40% rebound from the January lows.

Source: xStation5

What July can tell us about where stocks go next

Market Wrap: European equities at 3-week highs! Apple dips in US premarket!

Morning Wrap: AI Fuels the Rebound. Technology Makes a Strong Comeback

Apple is still impressive, but the market is no longer impressed

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.