NVIDIA reported results for the first quarter of fiscal year 2027 that once again came in ahead of market expectations on both the revenue and earnings levels. At the same time, the market reaction remains relatively muted, which suggests that investors are increasingly less focused on a simple “beat and raise” dynamic and are instead paying closer attention to the quality of growth, its diversification, and its durability within the context of the global artificial intelligence investment cycle.

Results vs expectations. Another strong beat in a high-expectation environment

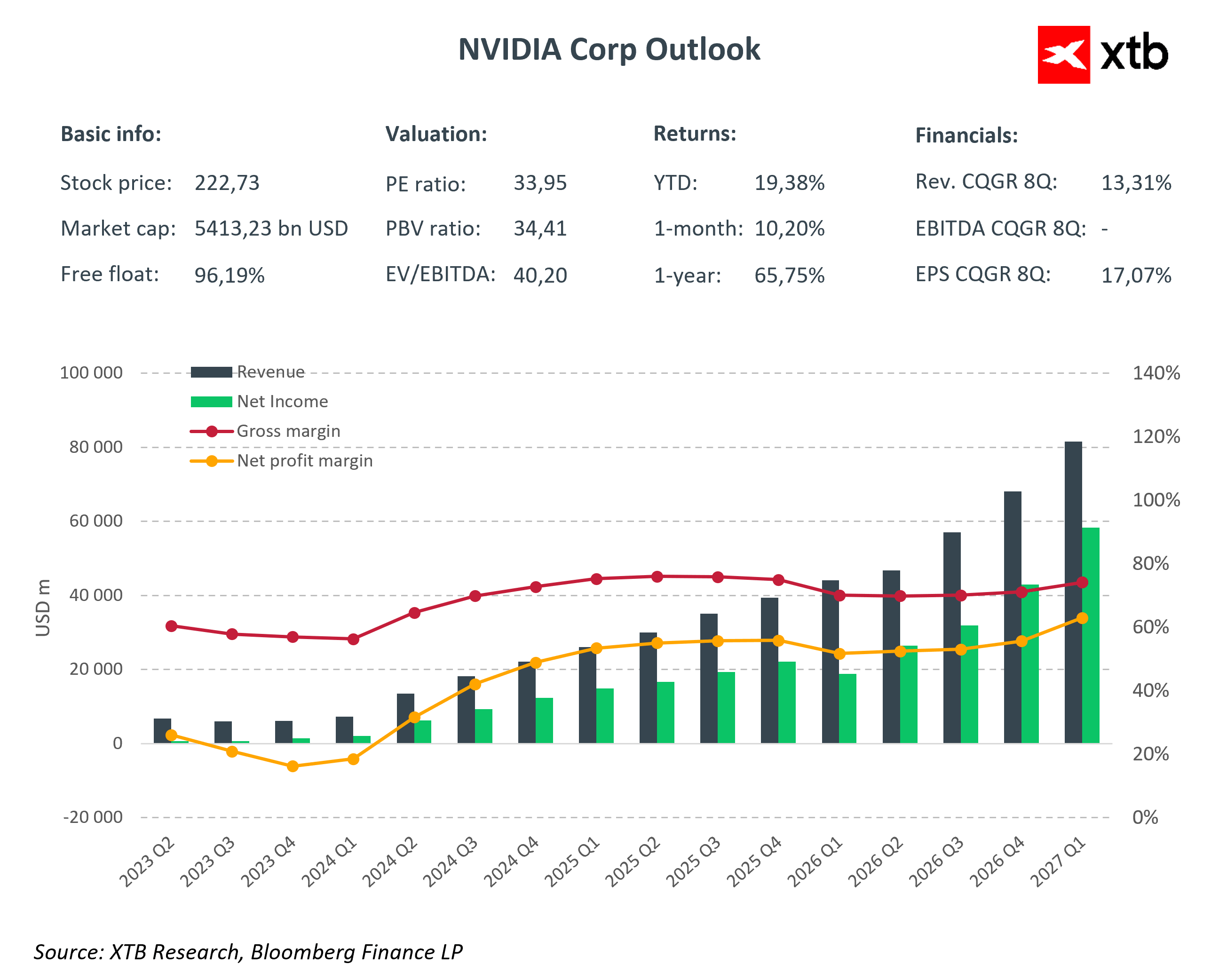

Revenue came in at $81.615 billion versus Bloomberg consensus of $79.15 billion, representing a clear upside surprise as well as 85 percent year-over-year growth and 20 percent quarter-over-quarter growth. The scale of the beat confirms that demand for AI infrastructure remains stronger than expected, despite a very elevated base and increasingly demanding market expectations.

GAAP earnings per share came in at $2.39, while non-GAAP EPS reached $1.87, both exceeding consensus estimates and confirming the continued strength of the company’s operating leverage and its ability to convert revenue growth into earnings.

On the profitability side, gross margin remained very strong at 74.9 percent, highlighting stable pricing power despite continued expansion in scale and growing operational complexity.

Key financial highlights Q1 FY2027

-

Revenue: $81.615 billion versus $79.15 billion expected, up 85 percent year over year and 20 percent quarter over quarter

-

EPS: $2.39 versus consensus range of $1.77–$1.80

-

Gross margin: 74.9 percent versus approximately 75 percent expected

-

Operating income: $53.536 billion, up 147 percent year over year

-

Net income: $58.321 billion, up 211 percent year over year

-

Data Center segment revenue: $75.2 billion versus roughly $73.5 billion expected, up 73 percent year over year

-

Operating expenses: $7.621 billion, broadly in line with expectations and reflecting continued efficiency at scale

Data Center as the foundation of the AI cycle

The Data Center segment remains the most important component of the report, generating $75.2 billion in revenue. It effectively defines the current growth cycle and continues to serve as the primary monetization channel of the global artificial intelligence boom.

The results confirm that demand from hyperscalers, AI cloud providers, and enterprise customers remains very strong, while the structure of growth is increasingly driven not only by GPUs but also by a broader AI computing and networking ecosystem.

Scale and efficiency

At the operating level, NVIDIA once again demonstrated exceptional scalability. Operating income of more than $53 billion, combined with relatively stable operating expenses of $7.6 billion, highlights a very strong operating leverage profile.

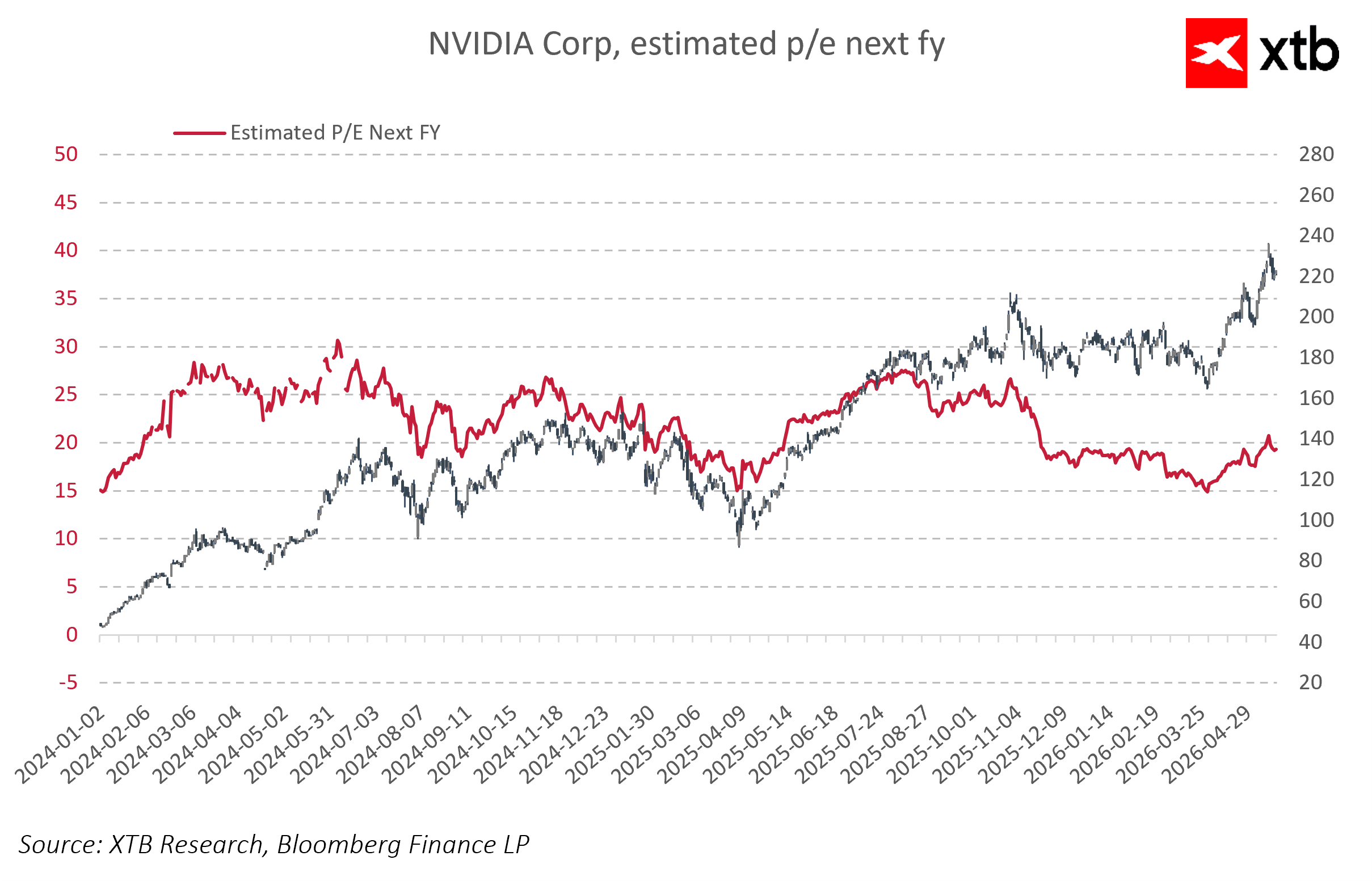

In practice, this means that each incremental dollar of revenue translates into a disproportionately large increase in profits, which remains one of the key pillars supporting the company’s premium valuation.

Capital return as a sign of cycle maturity

Another important element of the report is the announcement of an additional $80 billion share repurchase authorization, alongside an increase in the quarterly dividend from $0.01 per share to $0.25 per share. This signals that the company is entering a phase where, alongside extremely strong growth, capital return and cash distribution to shareholders are becoming increasingly important.

Such a significant expansion of the buyback program, combined with a meaningful dividend increase, suggests that NVIDIA is not only reinvesting heavily into growth but is also increasingly emphasizing shareholder returns, which in a company of this scale further reinforces the quality and stability of its business model.

Guidance: a signal that the AI cycle continues to expand

The most important element for the market remains forward guidance. NVIDIA expects approximately $91 billion in revenue for the next quarter, compared to consensus expectations of $87.2 billion. This represents another clear upside surprise and reinforces the view that demand for AI infrastructure remains in an expansion phase, with no clear signs of meaningful slowdown.

Importantly, the guidance does not include any revenue contribution from China in the Data Center compute segment, leaving additional upside potential in the medium to long term should regulatory conditions change.

Rubin, competition and market structure

Despite very strong results, investors continue to focus on several key risk areas. The first is the transition to next-generation architectures, including the Rubin platform, which is expected to follow Blackwell and further enhance efficiency and scalability in AI infrastructure.

The second is increasing competition from AMD, Broadcom, and Google, all of which are accelerating their efforts in custom silicon and alternative compute architectures in an attempt to capture a larger share of global AI spending.

The third is China, which remains a significant but partially restricted market, maintaining an element of uncertainty while also preserving optional upside in the medium term.

Market takeaway

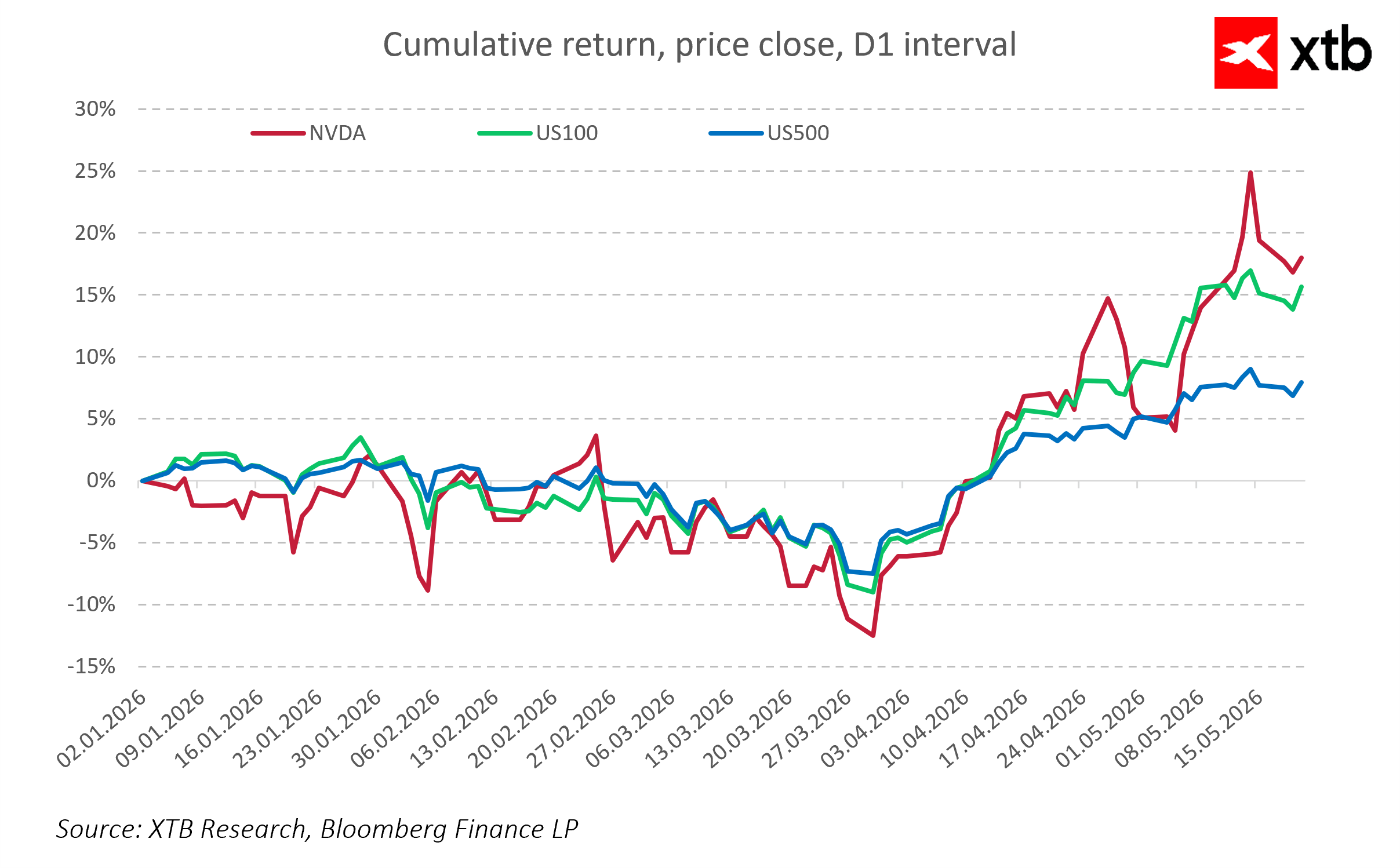

NVIDIA’s latest results once again confirm that the global AI investment cycle remains fully intact, with the company continuing to sit at its core as the leading provider of compute infrastructure.

At the same time, there is a clear shift in how the market interprets results. Investors are no longer reacting solely to earnings beats but are increasingly focused on forward momentum, guidance quality, and the company’s ability to sustain its technological leadership. In this sense, NVIDIA is gradually evolving from a traditional earnings-reporting company into a key indicator of the health of the global artificial intelligence investment cycle.

Did SaaS lost too much? Morgan Stanley says yes.

Tech sector catches its breath 🚀

US OPEN: Semiconductors drive a rebound

Market Wrap: Bulls Return to Europe Thanks to U.S.-Iran Mediation and Data from Germany

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.