Oracle (ORCL.US) slips ahead of Q4 earnings, but Bank of America sees 20% upside potential. After closing 3% lower yesterday, the stock is now trading roughly 40% below its all-time high reached in the autumn of 2025. The key question for investors: will Oracle help reignite the Nasdaq rally, or could it mark a short-term peak in AI-driven market sentiment?

Key Takeaways

Despite the recent pullback, BofA Securities raised its price target on Oracle from $200 to $240 per share while maintaining a Buy rating. The new target implies approximately 20% upside from current levels.

According to BofA, investor sentiment has improved after Oracle addressed funding concerns by raising a combined $50 billion through debt and equity financing.

The primary growth driver remains demand for cloud and AI solutions, particularly through Oracle Cloud Infrastructure (OCI).

Wall Street expects Oracle to report Q4 revenue of $19.19 billion, representing approximately 20% year-over-year growth.

Adjusted EPS is expected to come in at $1.96, up roughly 15% from a year earlier.

Key topics during the earnings call will likely include the pace of data-center expansion, the timing of revenue recognition from AI-related contracts, and the capital requirements needed to finance further growth.

Morningstar believes OCI is now at the center of the AI boom thanks to partnerships with companies such as OpenAI, Meta, and xAI.

The research firm expects Oracle's revenue to grow at an average annual rate of 30% over the next five years, while OCI revenue is projected to expand even faster, at roughly 78% annually.

Key risks include Oracle's ability to secure sufficient GPU capacity and bring new data-center infrastructure online quickly enough to meet demand.

Another important factor to monitor is Oracle's increasing reliance on major AI customers, particularly OpenAI.

The Key Risk: Debt

As a result, today's earnings release may be less about quarterly performance and more about whether Oracle can effectively monetize the massive demand for AI infrastructure. Given the recent deterioration in momentum across U.S. equities, investors may react nervously if the company misses expectations or disappoints on even one of the market's key metrics.

Oracle currently holds $553 billion in Remaining Performance Obligations (RPO), representing contracted future revenue commitments. RPO grew 325% year-over-year, highlighting exceptionally strong demand for AI infrastructure services.

The key question is how quickly Oracle can convert this enormous backlog into recognized revenue.

Analysts expect Oracle's cloud infrastructure business to continue growing at nearly 50% annually.

However, the balance sheet remains a major concern. Oracle's long-term debt exceeds $124 billion, while interest expenses have increased by approximately 32% year-over-year.

Free cash flow over the past twelve months is negative, at nearly -$25 billion, and the company may require up to $50 billion in additional financing initiatives.

Oracle also carries approximately $261 billion in additional data-center lease commitments.

At the same time, Oracle is increasingly competing with AWS, Microsoft, and Google in the AI infrastructure race. Over the long term, management aims to capture higher-margin AI workloads rather than compete solely as a traditional infrastructure provider.

The biggest risk remains execution: the company's massive investments must translate into revenue growth, margin expansion, and stronger cash flows quickly enough to justify the scale of capital being deployed.

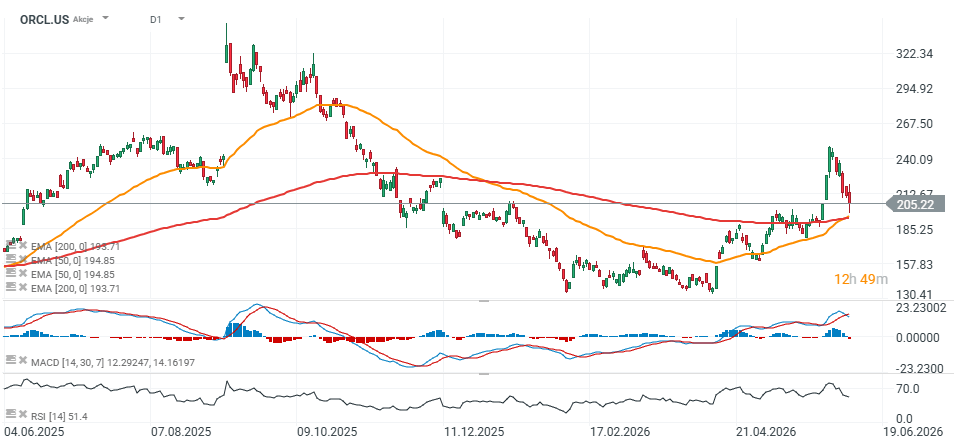

ORCL.US (D1)

Oracle shares are currently trading "dangerously" close to the 200-day exponential moving average (EMA200), marked by the red line on the chart. The $200 level appears to be a critical support zone for maintaining the longer-term bullish trend. A sustained break below this level could be interpreted by the market as a signal of growing concerns regarding the AI infrastructure investment cycle and Oracle's ability to generate attractive returns on its aggressive expansion strategy.

Source: xStation5

Intel Raises the Stakes: $20 Billion for a Major Comeback

Market Wrap: Energy Leads Gains in Europe, ASML Rebounds 🔼 Alcon Rises 4% After Earnings

Will the Wall Street Rally Gain Momentum? 🗽 A Recap of the US Earnings Season

Berkshire earnings: What do the reports say about the market’s direction?

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.