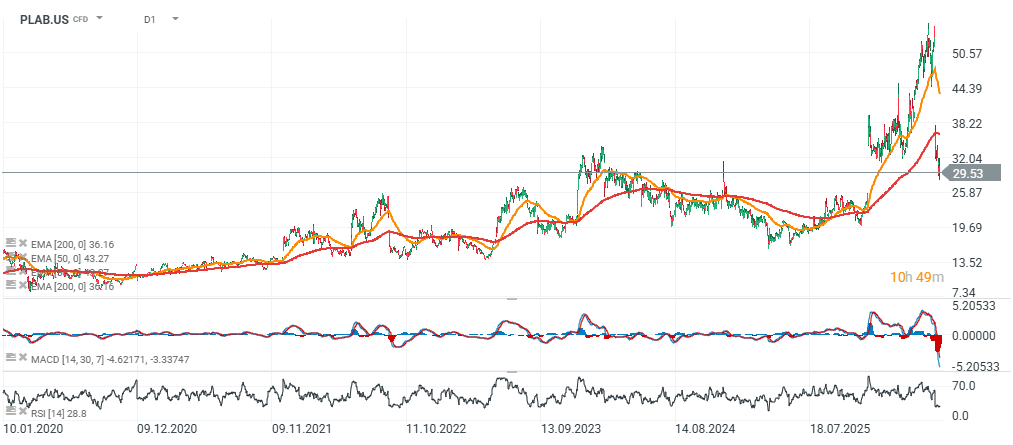

Photronics (PLAB.US) has come under significant pressure following its fiscal Q2 earnings release, leaving the company with a market capitalization of approximately $1.8 billion despite holding nearly $650 million in cash. The stock has fallen almost 50% from its all-time high near $56 per share, as investors reacted negatively to weaker-than-expected results and cautious Q3 guidance.

Many market participants have effectively viewed Photronics as a laggard within the semiconductor sector, shifting capital toward faster-growing AI and chip-related names. The company attributed the weakness primarily to a slowdown in semiconductor tape-outs, the stage at which new chip designs move toward commercial production.

Photronics generates much of its revenue when new semiconductor designs enter production, creating demand for photomasks used in the manufacturing process. Management linked the recent slowdown to geopolitical tensions in the Middle East, which weighed on customer activity and reduced demand for photomasks.

At the same time, management noted that conditions began improving as early as May. The number of new chip projects has started to recover, suggesting that the current weakness could prove temporary rather than structural. The company also emphasized that it expects to benefit from long-term AI-related semiconductor demand.

What Could Support Future Growth?

One potential growth driver is the company's advanced display mask business. Samsung Display is beginning mass production of next-generation G8.6 AMOLED panels, which are expected to be used in future Apple MacBook Pro models. Higher production volumes of advanced displays should translate into increased demand for high-quality photomasks, a core Photronics product.

Another opportunity comes from the growing outsourcing trend among major memory manufacturers such as Samsung and SK hynix. Outsourcing now extends to increasingly advanced semiconductor nodes, including processes as small as 7 nanometers. This trend could significantly expand Photronics' long-term addressable market.

The company is also investing heavily in new production capacity in both South Korea and the United States. These expansion projects are expected to be completed by fiscal 2027, with benefits likely beginning to appear in financial results as early as next year.

Valuation and Investment Thesis

Following the sell-off, Photronics is trading close to book value and at a price-to-earnings ratio of around 10, which is unusually low for a semiconductor-related company. While short-term volatility remains possible, the company continues to generate profits, maintains healthy double-digit net margins, and carries no meaningful debt burden. Its balance sheet remains one of the strongest among small- and mid-cap semiconductor suppliers.

The core investment thesis is that the current slowdown is cyclical rather than permanent. A recovery in semiconductor design activity, continued growth in AI and memory markets, and rising photomask outsourcing could support revenue and earnings growth over the coming years. The key risks remain the pace of demand recovery, the company's ability to utilize its expanding manufacturing capacity efficiently, and maintaining margins in a more competitive environment.

Historically, Photronics shares have been highly volatile. The stock is currently trading roughly 30% below its 200-day exponential moving average (EMA200), underscoring both the severity of the recent sell-off and the challenge of re-establishing a sustainable long-term uptrend. The biggest risk facing the company is a broader economic slowdown or recession that could further delay semiconductor tape-outs and new chip design activity. Such a scenario would likely weigh on demand for photomasks and could signal that the company's current earnings power may not be sustainable in the coming years.

Source: xStation5

Intel Raises the Stakes: $20 Billion for a Major Comeback

Market Wrap: Energy Leads Gains in Europe, ASML Rebounds 🔼 Alcon Rises 4% After Earnings

Will the Wall Street Rally Gain Momentum? 🗽 A Recap of the US Earnings Season

Berkshire earnings: What do the reports say about the market’s direction?

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.