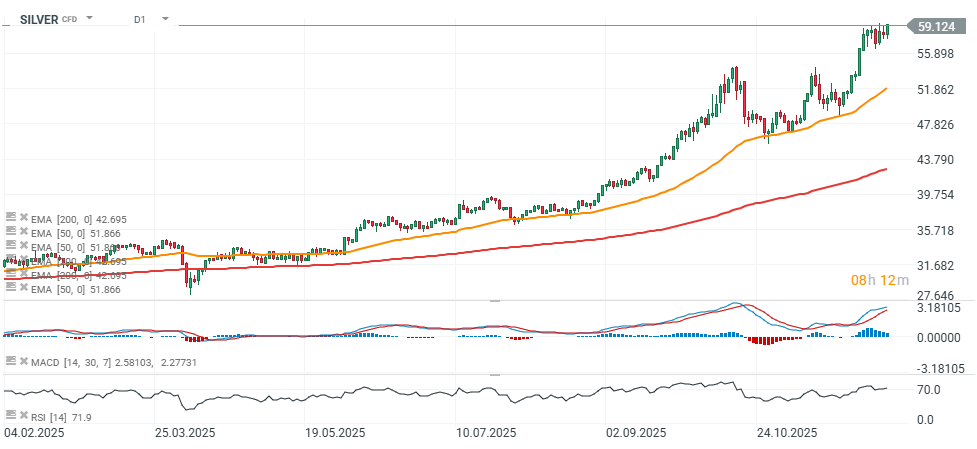

Silver (SILVER) is trading nearly 2% higher today ahead of tomorrow’s Federal Reserve decision. The market expects a 25 bp rate cut and is increasingly positioning for a more aggressive policy shift in 2026, when Kevin Hassett is expected to become the new Fed Chair — likely implementing a monetary policy framework aligned with the views of Donald Trump and close members of his administration, including Scott Bessent.

Although USD index futures (USDIDX) have been edging higher over the past few sessions, silver continues to see strong upward pressure. After each of the last two corrections, demand returned rapidly — first after the drop to $45/oz, and then after the pullback to $48/oz. The market is now moving toward the psychologically important $60/oz zone, even though ETFs cut 4.76 million troy ounces of silver from their holdings in the last session, reducing this year’s net purchases to 127.6 million ounces — the largest one-day decrease since October 24. Positive forecasts from industry giant Heraeus are also supporting sentiment.

Key Takeaways from Heraeus’ 2026 Outlook

-

Heraeus expects gold to reach $5,000/oz in 2026, with the rally resuming after a consolidation phase driven by central bank buying, falling real interest rates, and concerns over U.S. fiscal dominance.

-

Silver is expected to trade in the $43–62/oz range, though weakening demand in PV, jewelry, and silverware markets means the metal will depend heavily on investment inflows.

-

Central bank purchases remain a critical pillar of support for gold, and the dedollarization trend continues. Many central banks plan to increase their gold reserves while reducing U.S. dollar exposure.

-

Investment demand remains strong: sales of bars and coins continue to rise, and ETF holdings increased 18% in 2025, though still below the 2020 peak — leaving room for additional buying.

-

Heraeus warns that U.S. fiscal dominance — higher government spending and political pressure to keep rates low — may keep real interest rates negative, which historically supports gold prices.

-

A potential U.S. recession in 2026 remains a downside risk, especially for PGMs, as labor-market indicators weaken and the yield curve’s uninversion signals a deteriorating economic outlook.

-

Demand for platinum, palladium, and rhodium may decline further as combustion-engine vehicle sales shrink, while ruthenium remains supported by HDD demand linked to data-center expansion.

-

The sharp silver rally in 2025 was driven by tight liquidity and strong ETF/retail buying, rather than industrial demand, suggesting the market may need time to stabilize.

-

Photovoltaic sector demand for silver is expected to decline in 2026 for the first time in years, as thrifting accelerates and installation growth in China slows sharply.

-

High prices continue to suppress global demand for silver jewelry and silverware, especially in India, which accounts for the majority of demand in these categories.

-

Silver recycling is likely to increase in 2026 as higher prices incentivize recovery, while mine supply should rise modestly alongside increased production of gold, copper, and zinc.

-

For silver, investment flows remain the primary directional driver — inflows can boost prices, but they have been volatile, and high coin premiums may limit retail activity.

-

Heraeus emphasizes that silver remains a higher-beta version of gold — meaning that if the gold rally returns, silver is likely to follow with significantly higher volatility.

SILVER (D1 interval)

Source: xStation5

🛢️Brent Crude Oil Tests $95 per Barrel

Oil prices jump as markets wait for key earnings releases

Morning Wrap: AI companies and gold back in favour? (22.07.2026)

Daily Summary: Semiconductors Rise in the Shadow of Geopolitical Turmoil

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.