The Swedish audio distribution platform, listed on a U.S. exchange, fell more than 10% after publishing its Q1 2026 results. Despite the extreme market reaction, the figures do not seem to justify it - at least not at first glance.

- Earnings per share (EPS) came in clearly above expectations, reaching as much as €3.45 versus market expectations of around €2.95.

- Revenue was merely solid, almost exactly in line with the consensus, totaling €4.53 billion.

Additional positives for the company include:

- Premium subscribers increased by 9% year over year to 293 million—close to market expectations.

- Revenue from premium users rose by 10% year over year to €4.15 billion.

- Monthly active users increased to 761 million—also above expectations.

- Gross margin rose to a record 33%, beating the company’s own guidance.

- Operating profit was also record-high, rising to €715 million with a 15.8% margin.

- Free cash flow (FCF) was record-high as well, at €824 million.

Could anything spoil such strong results? The market seems to be focusing almost exclusively on guidance.

The company announced that Q2 operating profit is expected to reach €630 million. That is a decline versus Q1 and materially below market expectations of about €674 million. Revenue is expected to increase to €4.8 billion, with monthly active users rising to 778 million.

This suggests the company is not expecting a structural deterioration in business conditions, but rather signaling a temporary dip in profitability - albeit from a very high base.

At the same time, the company is showing it can steadily grow revenue, and the user metrics are also providing reasons for optimism.

While a significant quarter-on-quarter drop in profitability is a notable short-term issue, the magnitude of the sell-off appears, in the context of this release, overdone.

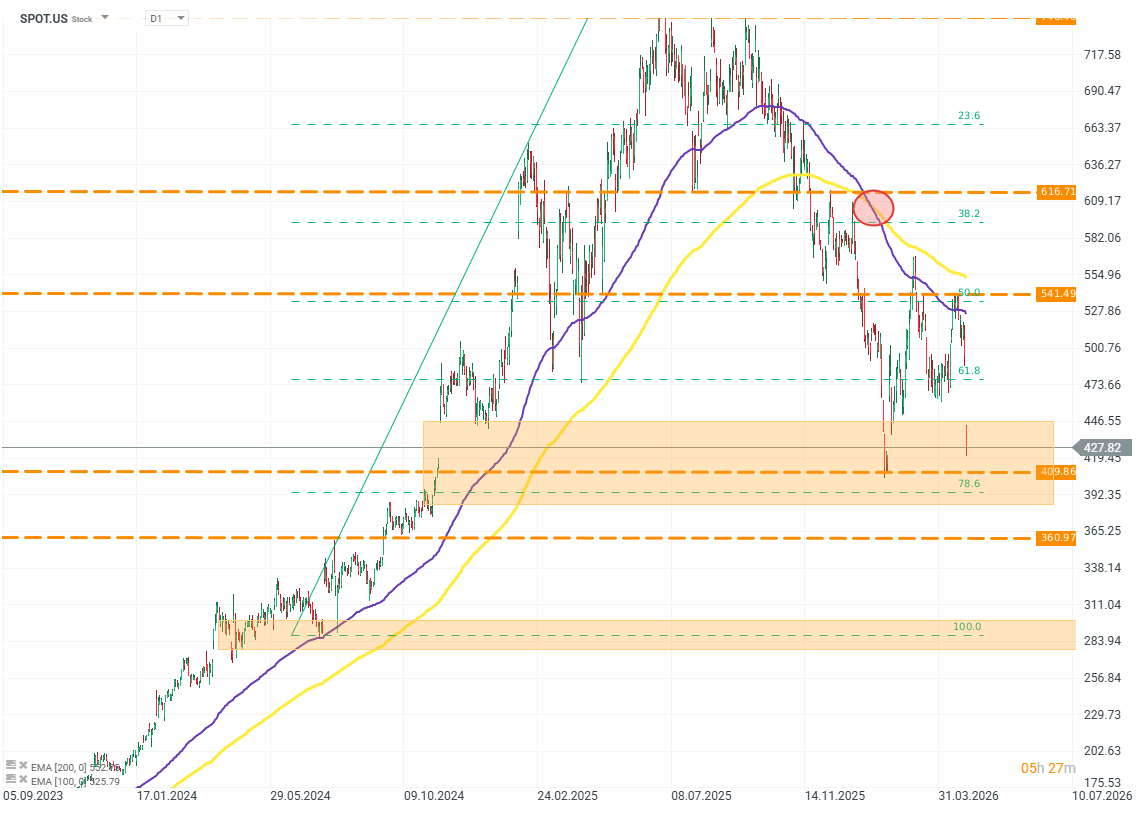

SPOT.US (D1)

The second half of 2025 proved very difficult for Spotify. The company’s valuation fell by as much as 45%, wiping out the entire gain from early 2025. The depth of this decline may raise questions—questions shared by analysts at investment firms. Given the time frame, the drop in the company’s valuation may have been driven mainly by capital rotating into AI-focused companies. Source: xStation5

Daily Summary: Nasdaq 100 Up 3.2% – Is the Bull Market Back? (04.08.2026)

Palantir Earnings: High Expectations and Even Bigger Gains

Daily Summary - The market starts to doubt rate hikes after Warsh, but Trump destroys the rebound

US OPEN: Wall Street Holds Its Breath Ahead of Fed Decision and Tech Giant Earnings

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.