The race for artificial intelligence is still most often told through the same names: NVIDIA, Microsoft, or Alphabet. These are the companies building the largest GPU clusters, training frontier models, and setting the pace for the entire market. Within this narrative, AMD for a long time remained in the background as a cheaper alternative or the second choice in the world of processors and accelerators.

However, this picture is increasingly diverging from reality.

AMD is entering a new phase of its history, where it is no longer seen as a subcontractor to broader industry trends, but as one of the key providers of the foundational infrastructure for the entire AI ecosystem. It is increasingly described not just as a chip company, but as a firm that brings together three critical building blocks of the new computing era: EPYC server CPUs, Instinct GPU accelerators, and the growing Ryzen AI platform with NPU units.

This shift did not happen overnight, but recent quarters have clearly accelerated it. Financial results are no longer just strong reports in a cyclical industry, but are starting to resemble a structural growth trend. Data Center has become the largest and fastest growing segment, while AI activity on both the GPU and CPU side has moved from future narrative to a real driver of revenue.

As a result, AMD is increasingly attracting investors looking for exposure not only to AI models themselves, but to the entire infrastructure layer that enables them. The market is gradually recognizing that in the AI era it is no longer only about individual high end GPUs, but about a full computing system in which CPU, GPU, memory, and networking must operate as a single organism.

And this is exactly where AMD appears as one of the few companies trying to deliver that system in a more integrated way.

What is also becoming increasingly clear is a shift in how AI is being perceived. After the phase dominated by GPUs and model training, attention is gradually moving toward inference, AI agents, and more complex workflows that require not only raw compute power, but also intelligent orchestration of the entire system.

In this setup, the CPU is no longer just a supporting component for GPUs. It is regaining its role as one of the core elements of the AI infrastructure.

If this trend continues, AMD, as one of the few major players combining both CPU and GPU capabilities in a single portfolio, could find itself in a uniquely strong position in the next phase of AI market development.

What is AMD

AMD is a global semiconductor company designing integrated circuits for personal computers, servers, and artificial intelligence systems.

Its business is built on three main pillars: Ryzen processors for the PC market, EPYC server chips for data centers, and Instinct accelerators for AI workloads. An increasingly important part of its portfolio is also the Ryzen AI platform with NPU units, which are specialized processing units designed to run artificial intelligence tasks directly on devices. NPUs are optimized for workloads such as image recognition, natural language processing, and local AI inference, offering significantly higher energy efficiency than traditional CPUs or GPUs.

The company operates under a fabless model, outsourcing manufacturing primarily to TSMC.

For many years AMD was viewed as a secondary option versus Intel and NVIDIA, but with the rise of artificial intelligence it has gained a new position as a supplier of both CPUs and GPUs for next generation computing infrastructure.

Quarterly results: a turning point

AMD’s latest Q1 2026 results confirmed that the company has entered a clearly accelerating growth phase driven by artificial intelligence.

Key figures:

-

Revenue: approximately 10.3 billion USD, up around 38 percent year over year

-

Data Center segment: approximately 5.8 billion USD, up more than 50 percent year over year

-

Net income: strong increase supported by operating leverage and improving AI profitability

-

Cash flow: very strong, maintaining high financial flexibility

-

Q2 2026 guidance: around 11.2 billion USD in revenue, indicating further expansion

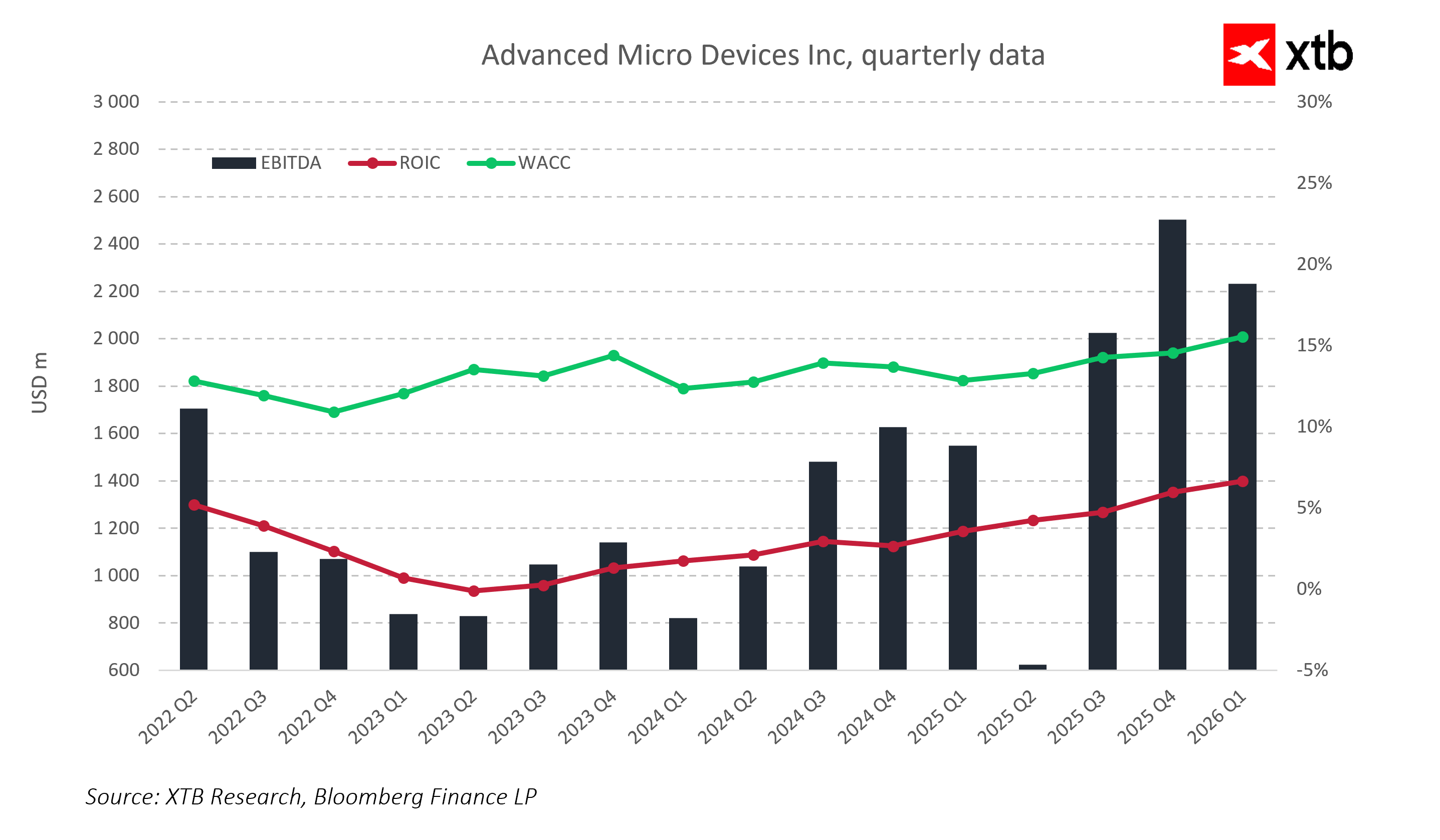

The most important part of the report was once again the Data Center segment, which has become the main growth engine of the company, gradually overtaking traditional businesses such as PC and gaming that historically defined AMD.

Even more important than the numbers was the tone of the communication. Management explicitly identified Data Center as the key growth driver and highlighted that demand related to AI, both on the CPU and GPU side, is growing faster than previously expected.

As a result, the market interpreted these results as confirmation that AMD is no longer a cyclical hardware company, but one of the main beneficiaries of the global AI infrastructure buildout.

Data Center: the new core of AMD

The Data Center segment has become the area where AMD has most clearly transformed its identity. What was once one of many business segments is now the main growth engine and the core of the entire investment narrative.

Data centers represent the backbone of the modern digital economy: hyperscaler infrastructure, cloud computing, AI model training, and increasingly complex inference systems. In this environment, AMD provides two fundamental building blocks: EPYC server CPUs and Instinct accelerators.

Source: ADM.COM Instict series 350

EPYC handles general compute, system logic, and workload management, while Instinct focuses on the most demanding AI computations. As AI models scale and workloads become more complex, these two components increasingly function as a unified system rather than separate products.

Source: ADM.COM Processor series Zen

The most important change in recent quarters is that AI demand is no longer limited to GPUs alone. Hyperscalers are now building full compute platforms in which CPU, GPU, memory, and networking must be carefully balanced. In this environment, AMD gains a unique position as one of the few companies offering both CPU and GPU within a single ecosystem.

As a result, Data Center is no longer just a product segment. It has become a participation in the construction of entire AI systems composed of thousands of interconnected components.

The CPU comes back into play

The first phase of the AI revolution was a GPU story. Accelerators became the symbol of the boom, driving model training and defining investment cycles across the industry. CPUs remained in the background, mainly supporting GPU workloads.

Source: ADM.COM Processor series Ryzen 9000

This picture is now changing as the market enters the next phase of AI development.

Inference is becoming more important, meaning the phase where models are actually used in production. At the same time, AI agents are emerging, capable not only of generating responses but also of planning actions, using tools, and executing complex workflows across systems.

In this environment, compute architecture looks very different. GPUs still handle heavy computation, but CPUs are becoming the orchestration layer of the entire system. They manage data flow, coordinate accelerators, handle memory and networking, and support real time decision logic.

The more complex AI systems become, the more important CPU efficiency becomes.

AMD is uniquely positioned to benefit from this trend, as it is one of the few major companies offering both advanced CPUs (EPYC) and GPUs (Instinct), designed to work together within a unified compute ecosystem.

Financial analysis

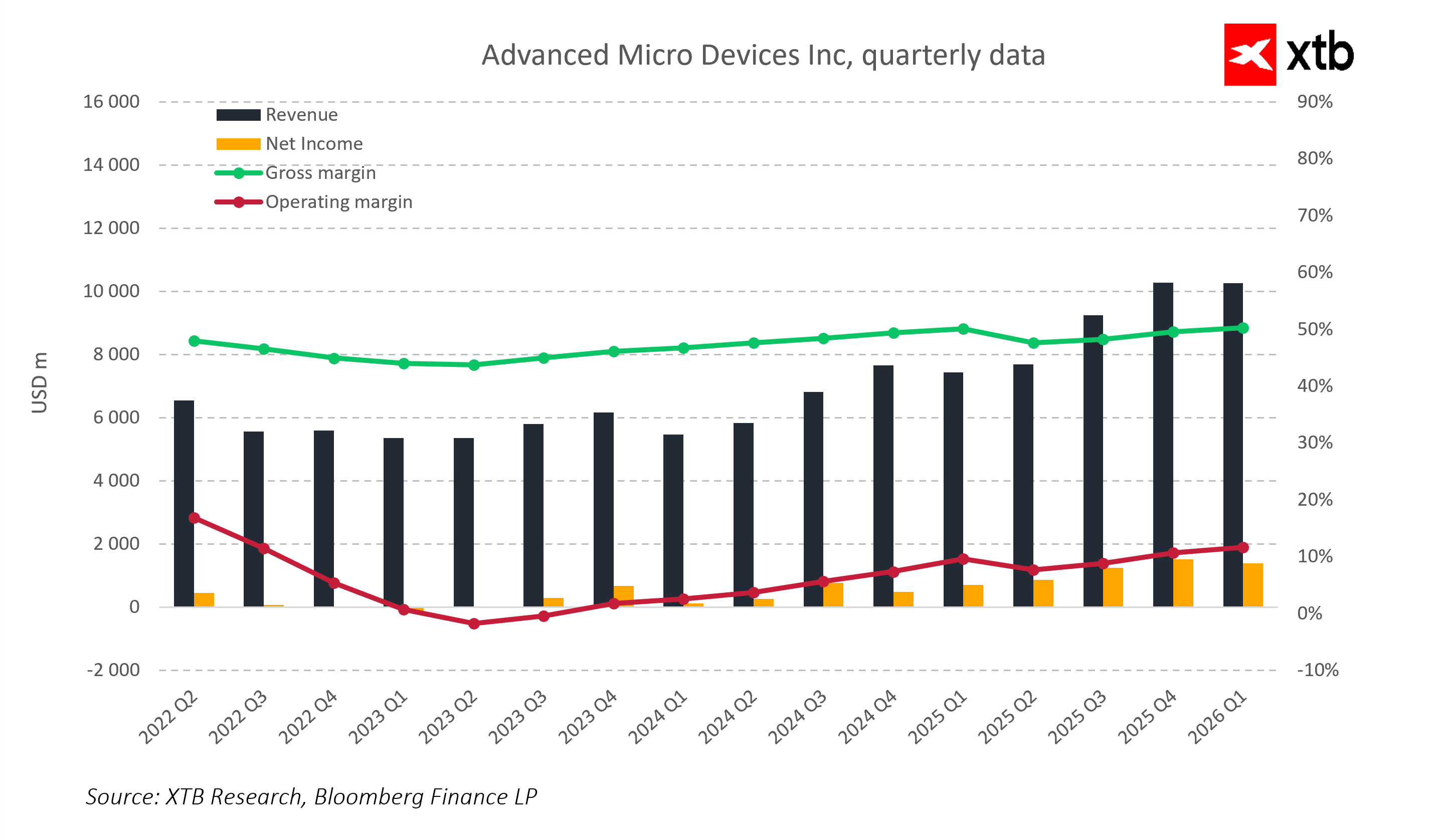

Looking at AMD’s financial data on a quarterly basis, the company is clearly transitioning from a cyclical business model to a more structural growth trajectory driven by Data Center and AI related products.

Revenue momentum stands out first. The company has moved from roughly 5 to 6 billion USD per quarter to consistently higher levels above 9 billion USD, with a clear break above the 10 billion USD mark. This is not a one off spike, but a gradual trend of higher and higher base levels.

Profitability has also improved. Gross margins remain stable around 50 percent, supported by a higher mix of advanced products. Operating margins, after earlier pressure, are gradually recovering as scale improves and the business mix shifts toward higher margin AI workloads.

Net income has moved from weak or near break even levels into consistently positive territory, reflecting strong operating leverage. Revenue growth is increasingly translating into bottom line expansion.

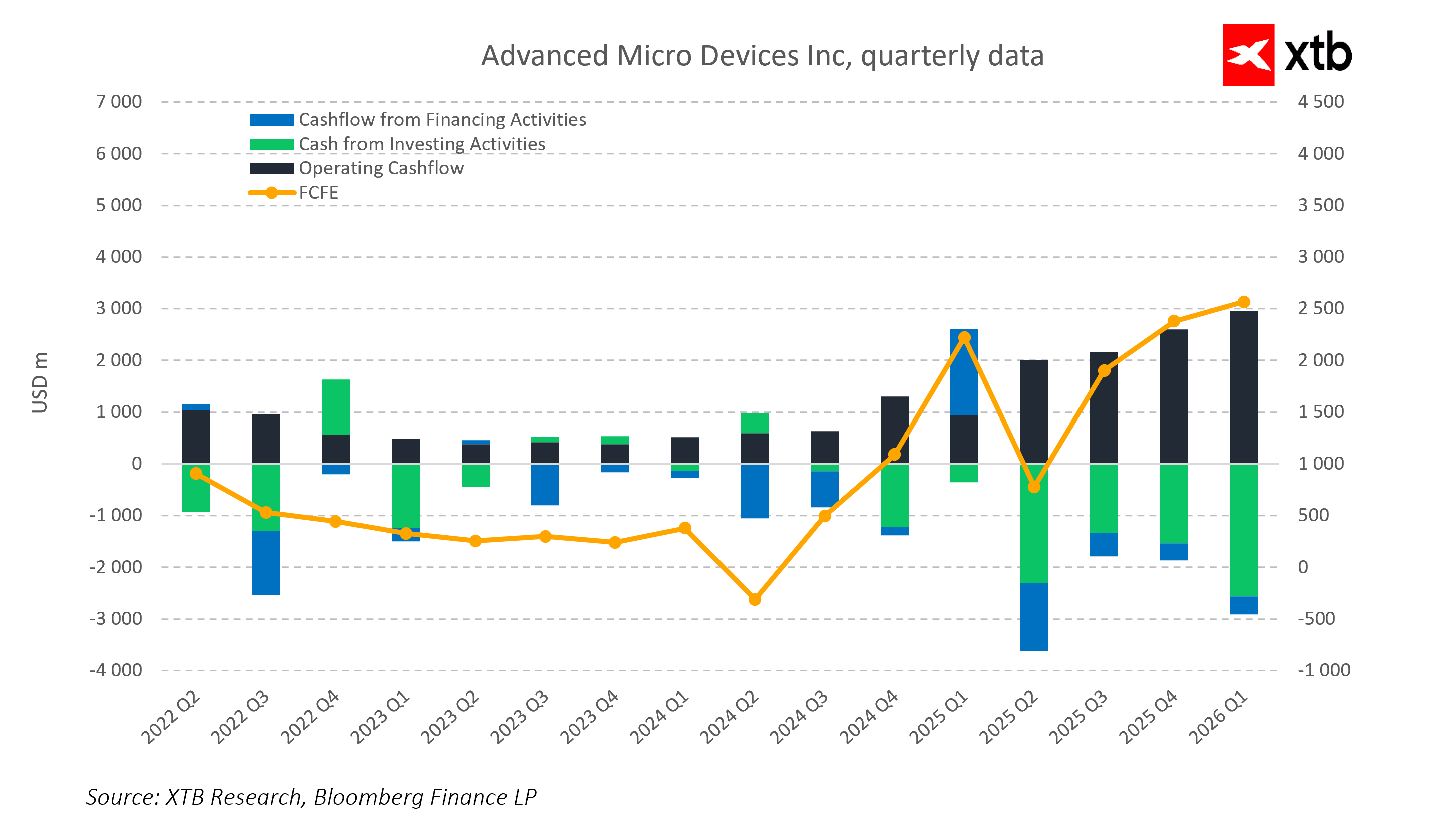

Cash flow is another key strength. Operating cash flow and free cash flow are trending higher, with AMD now generating several billion USD per quarter. Despite some volatility in investing and financing cash flows, the overall picture remains one of improving financial strength.

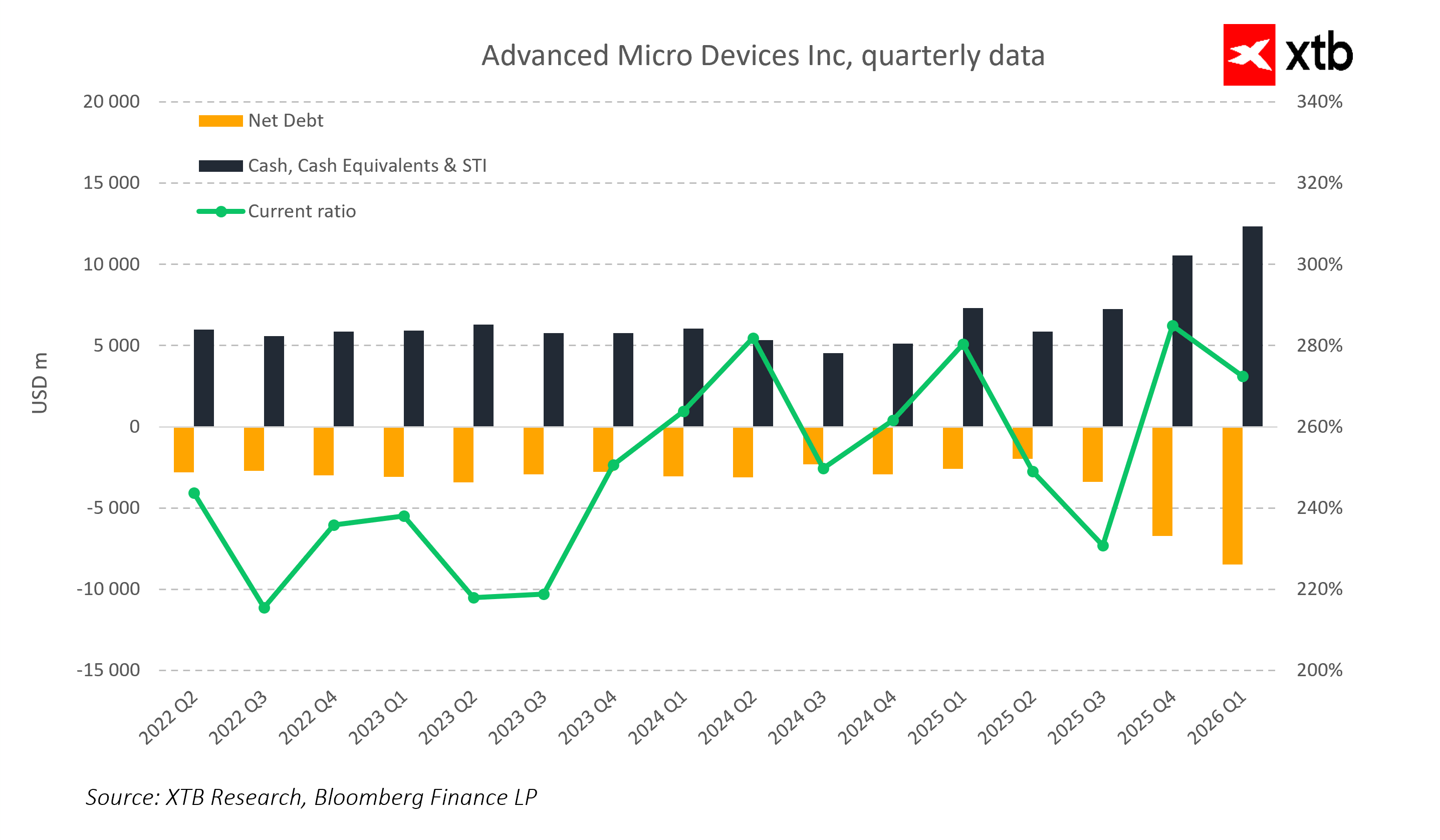

The balance sheet remains healthy, with strong cash reserves and manageable net debt levels. Liquidity ratios are stable, giving the company flexibility to continue investing in R&D and ecosystem development.

Overall, AMD is not only growing in revenue terms but also improving the quality of that growth. The increasing share of Data Center and AI related products is pushing the company toward a more predictable, scalable, infrastructure oriented business model.

Market, sentiment, and AMD as AI infrastructure

AMD’s recent quarters are not only about financial improvement but also about a clear shift in how the company is perceived by the market. It is increasingly moving away from the narrative of a cyclical semiconductor manufacturer and toward being seen as a key beneficiary of the long term AI investment cycle.

The market is re rating AMD primarily through growing interest in Data Center and AI related products. It is no longer viewed as a cheaper alternative to NVIDIA, but as a provider of a full compute stack including both CPUs and GPUs. This shift is important because valuation is increasingly based on platforms rather than individual products.

At the same time, the broader AI sector continues to attract capital toward infrastructure companies. Investors are less focused on application layer AI and more on the foundational layer that provides compute power, memory, and system architecture.

AMD sits at the intersection of two major narratives: GPU driven AI training demand and the growing importance of CPUs in AI agents and complex inference systems. This combination allows the company to participate in multiple growth waves simultaneously.

As a result, AMD is increasingly perceived as part of the AI infrastructure layer rather than just a component supplier. This represents a structural shift in perception that typically unfolds gradually through financial results, product development, and repeated validation from the market.

At this stage, AMD is in a phase where fundamentals are starting to support the new narrative rather than merely follow it. Historically, this has been a key transition point for companies moving from cyclical hardware players to strategic infrastructure providers in new technology cycles.

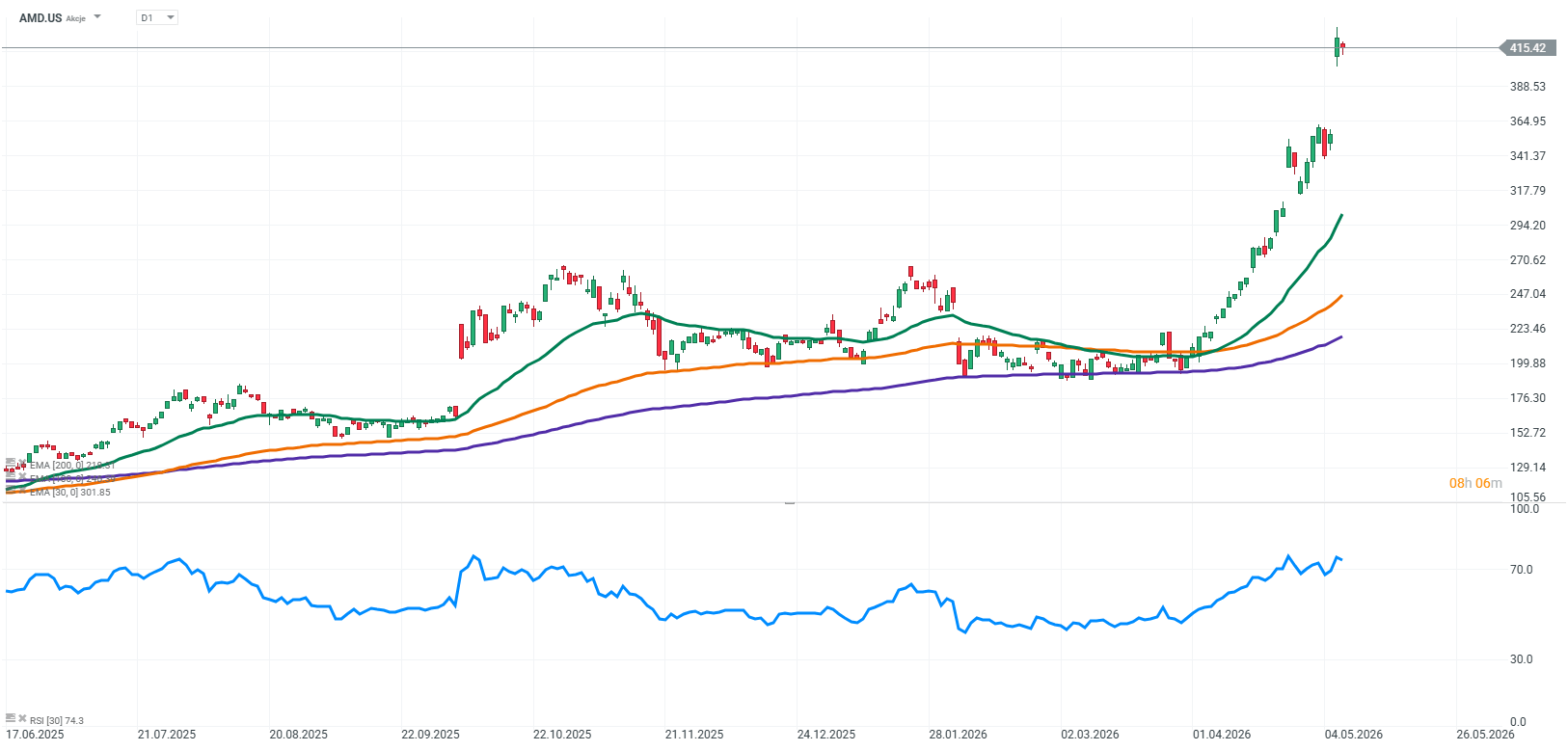

Source: xStation5

ASML sell-out: Dreams and rumors will not break the monopoly

AI trade loses momentum, as LVMH fails to impress

Economic Calendar: PayPal, Visa and Coca-Cola to overshadow macro data (28.07.2026)

Morning Wrap: US halt to attacks balanced by semiconductor sector declines (28.07.2026)

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.