During earnings season, there are companies whose reports are followed mainly by their shareholders. However, there are also companies that attract the attention of virtually the entire market. ASML has belonged to this group for years. The Dutch company’s results provide insight not only into the condition of its own business but also into the pace of investment carried out by the world’s largest semiconductor manufacturers. Every new forecast, order level, or management comment becomes an important signal showing the state of demand for the most advanced technologies used in chip production.

The second-quarter report delivered exactly what investors had been hoping for. The company presented very strong financial results, raised its full-year guidance, and maintained a positive outlook for the coming quarters. The market interpreted these announcements as confirmation that spending on semiconductor infrastructure development remains high and that the current investment cycle still has room for further growth.

In the case of ASML, a single quarterly report rarely changes the way the company is perceived. Much more often, it reinforces investors’ belief that its position within the global supply chain remains exceptionally strong. This is precisely why the company’s earnings releases attract so much attention. For many market participants, they represent one of the best indicators of the overall health of the semiconductor industry.

Why ASML Remains One of the Most Important Companies in the Semiconductor Market

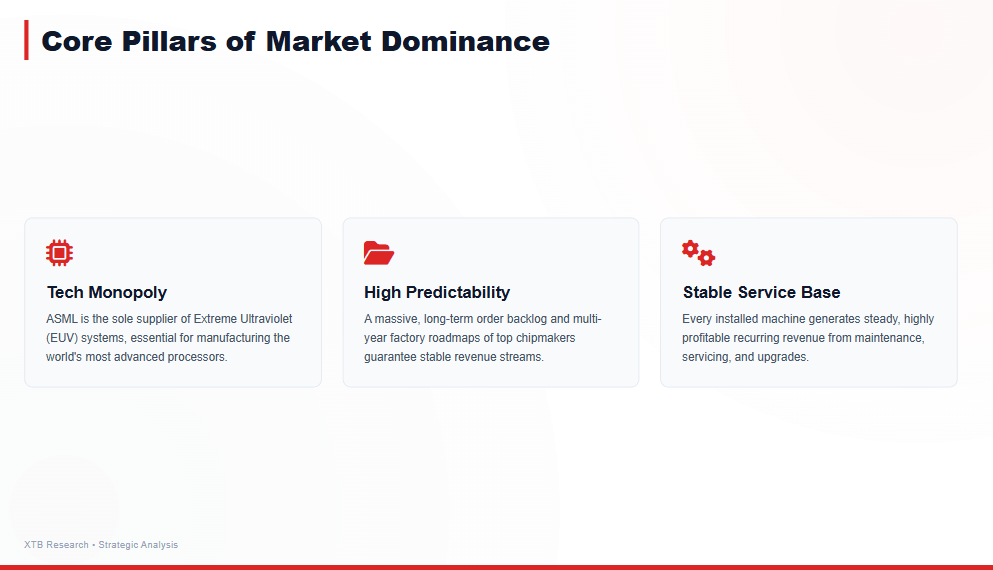

A great deal has already been written about ASML’s competitive advantage. For years, the company has remained a key supplier of technologies used in the production of the most advanced semiconductors, and its market position has not changed. Today, however, a more interesting question goes beyond simply describing the business model: how long will the current investment cycle continue, and will ASML remain one of its biggest beneficiaries?

For now, there are no clear signs of a significant slowdown. The largest chip manufacturers continue to invest billions of dollars in new factories, while data center operators are consistently increasing their spending on computing infrastructure. Behind each of these decisions are new orders for increasingly advanced manufacturing technologies. This is where ASML comes into play. The greater the ambitions of semiconductor manufacturers, the stronger the demand becomes for the solutions offered by the Dutch company.

ASML’s business model fits perfectly into this market environment. The company does not compete through low prices or short-term promotions. Instead, it sells solutions that become part of long-term investment plans of the world’s largest chip manufacturers. Orders placed today often translate into revenue recognized in future quarters, while the company’s extensive backlog provides significant visibility and predictability. This is one of the characteristics that has distinguished ASML from many other technology companies for years.

The current cycle also has another important feature. In previous years, semiconductor market growth was driven mainly by smartphones, personal computers, and consumer electronics. Today, the primary driver of investment is data centers and infrastructure used for training and operating artificial intelligence models. This market requires increasingly advanced chips, and with them, greater investment in cutting-edge manufacturing technologies. From ASML’s perspective, this creates an environment in which demand may remain elevated for much longer than during a typical economic cycle.

What Will Drive ASML in the Coming Quarters

For ASML, the most important factor is not the result of a single quarter, but the direction in which the entire semiconductor market is heading. Producing the most advanced chips requires ever-increasing capital investment, and the technological race between the largest chip manufacturers has clearly accelerated. Each new generation of processors means a more complex manufacturing process, more technological steps, and higher spending on factory equipment. This is exactly the environment in which ASML builds its competitive advantage.

It is also worth paying attention to the structure of ASML’s revenue. Sales of new systems remain the company’s most important business segment, but services have been playing an increasingly important role every year. Each delivered machine generates additional revenue for many years through maintenance, upgrades, and technical support. As a result, ASML’s business is not based solely on winning new orders. Over time, the installed base of equipment creates a growing stream of recurring revenue, improving earnings stability and reducing the impact of short-term fluctuations in the semiconductor cycle.

The order backlog also remains a key factor. Production of the most advanced lithography systems takes many months, meaning customers’ investment decisions occur well before revenue recognition. This gives ASML relatively strong visibility into future quarters and allows the company to plan production capacity more effectively. In the current market environment, where leading semiconductor manufacturers are implementing multi-year investment programs, this business model becomes an additional advantage.

In the coming quarters, another factor will become increasingly important. A growing share of the largest chip manufacturers’ spending is focused on infrastructure supporting artificial intelligence. The construction of new data centers and the development of next-generation processors and chips require continued expansion of manufacturing capacity. For ASML, this means operating in an environment where demand is not driven by a single product or a short-term trend, but by a long-term investment cycle affecting virtually the entire semiconductor industry.

The Market Received Exactly What It Was Looking For

The strong momentum in the semiconductor sector is reflected in the figures reported by ASML. The second quarter delivered results clearly above market expectations, while management’s comments regarding the coming months made an even stronger impression. The company not only maintained a high pace of growth but also raised its full-year guidance, confirming that demand for its solutions remains exceptionally strong.

Key Takeaways Following the Earnings Report

-

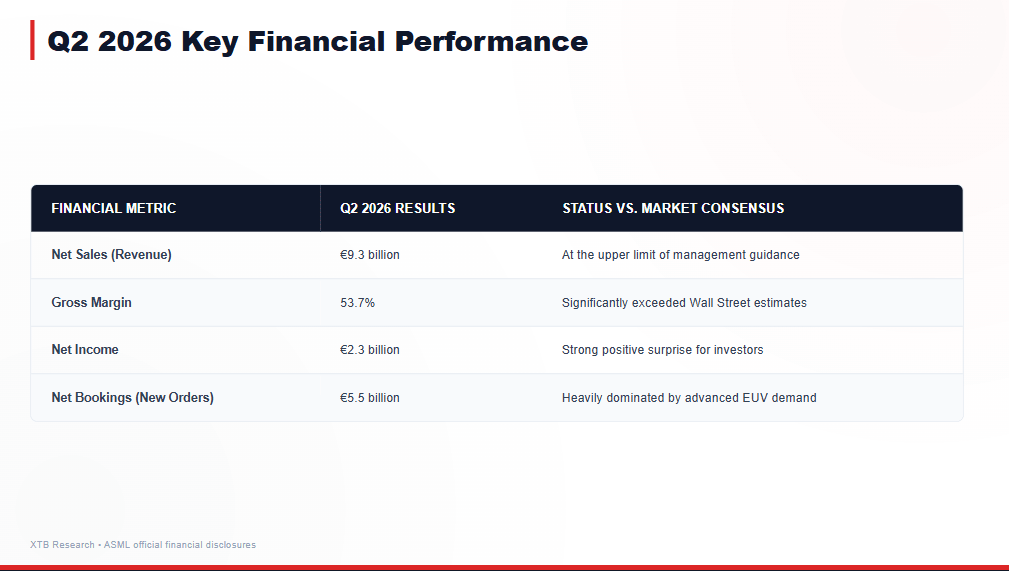

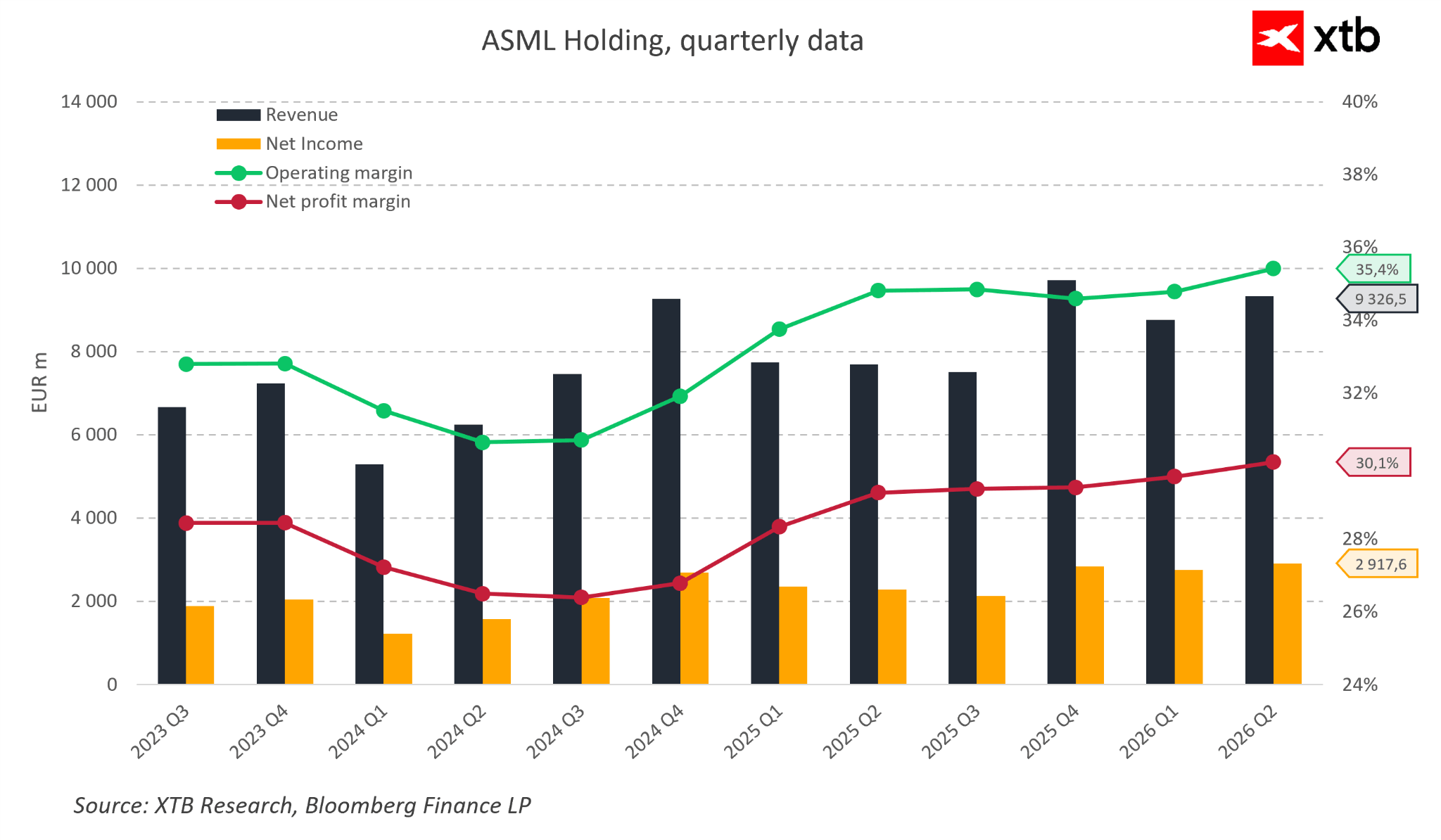

Revenue reached €9.3 billion, hitting the upper end of previous guidance.

-

Gross margin increased to 53.7%, remaining at a very high level.

-

Net income amounted to €2.3 billion.

-

New bookings reached €5.5 billion, with a significant share coming from EUV systems.

-

Management raised its revenue forecast for the full year 2026.

-

The company maintained its positive outlook for 2027 and 2028, pointing to continued high levels of investment across the industry.

In practice, the report delivered several important signals. The first was the continued strength of the order pipeline. For a company operating based on long-term investment projects, this is one of the most important indicators of future business activity. It shows that the world’s largest semiconductor manufacturers are not reducing spending despite the record levels of investment made in recent years.

Margins also remain highly encouraging. Once again, ASML demonstrated that it can combine business expansion with exceptional profitability. This is an important signal for investors because it shows that rising demand is not coming at the expense of business quality. The company continues to successfully convert its technological advantage into highly attractive financial results.

Management communication also deserves attention. The biggest surprise was not the quarterly results themselves, but rather the optimism surrounding future quarters. Raising guidance and maintaining a positive outlook for the coming years suggest that the current semiconductor investment cycle remains in a growth phase. This was the element most positively received by the market and was a major factor behind the strong share-price reaction following the earnings release.

However, quarterly results represent only one part of the broader story. A single report can show how the company performed over the previous three months, but only an analysis of the underlying fundamentals can answer whether the current valuation is justified by the quality of the business. Therefore, the next section takes a much broader look at ASML’s financial profile rather than focusing only on one quarter.

Financial Analysis: The Fundamentals That Continue to Support the ASML Story

A unique technological position alone is not enough to justify a high valuation. In ASML’s case, financial performance is equally important, as it demonstrates whether the company’s competitive advantage is truly translating into lasting shareholder value. An analysis of revenue growth, profitability, and cash generation provides a clearer view of the quality of the business and helps determine whether the current growth narrative is supported by actual financial results.

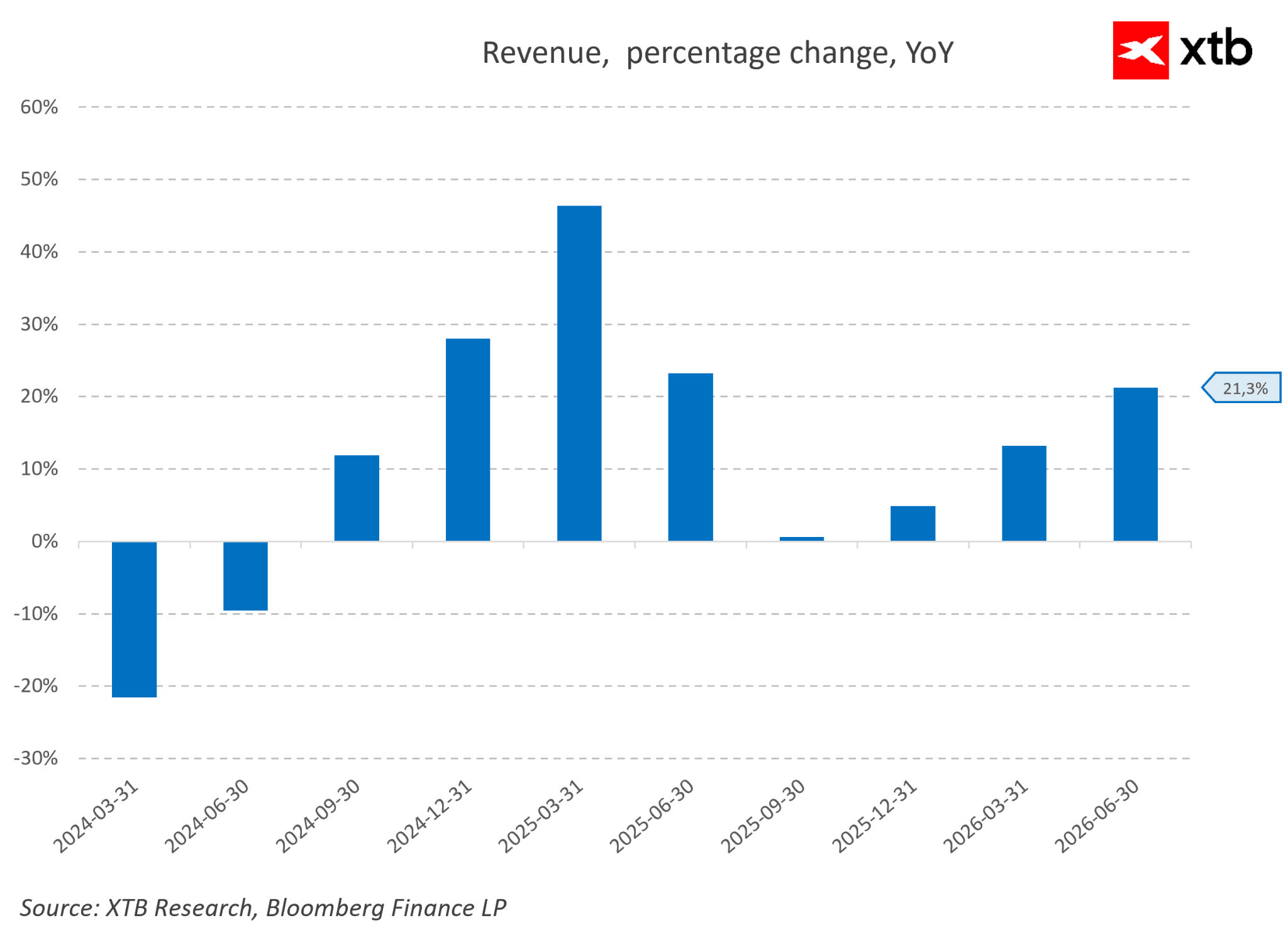

The first positive signal is the company’s return to strong growth momentum. After a weaker start to 2024, ASML gradually rebuilt its growth trajectory, and results began to look significantly more stable from 2025 onward. In the latest annual figures, revenue increased by 21.3%, showing that the company continues to benefit from favorable market conditions. Importantly, revenue growth has been accompanied by the maintenance of very high profitability.

ASML has distinguished itself for years through its ability to generate above-average margins. In the second quarter of 2026, operating margin reached 35.4%, while net margin stood at 30.1%. Such levels confirm not only the exceptional quality of the business but also the strength of the company’s competitive position. ASML does not need to compete primarily through pricing because it provides solutions that are a critical part of manufacturing the most advanced semiconductors.

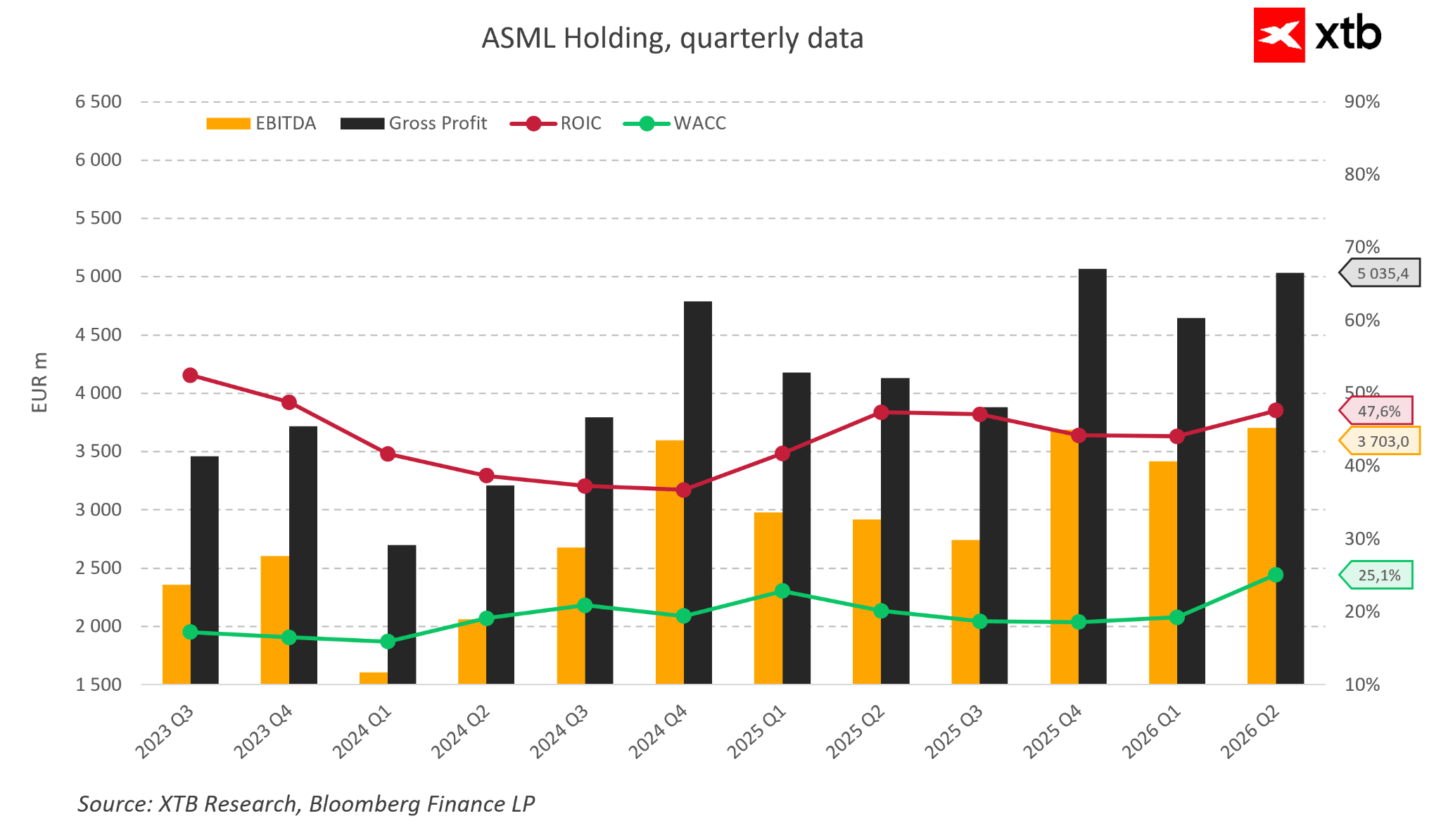

The improvement in results is also confirmed by operating profit metrics. EBITDA reached €3.7 billion in the latest quarter, while gross profit amounted to €5.0 billion. After a weaker period in 2024, the company has clearly returned to a growth path, benefiting from rising demand for its technologies. This shows that ASML is not only benefiting from increased semiconductor industry investment but is also highly effective at converting that demand into financial performance.

One of the most important indicators of business quality remains the relationship between return on invested capital and the cost of capital. In ASML’s case, ROIC remains significantly above the company’s cost of capital, which stood at 25.1%. This means that the company is successfully creating value for shareholders and maintaining high efficiency despite requiring substantial investment. In an industry that demands enormous spending on technological development, this represents a particularly important advantage.

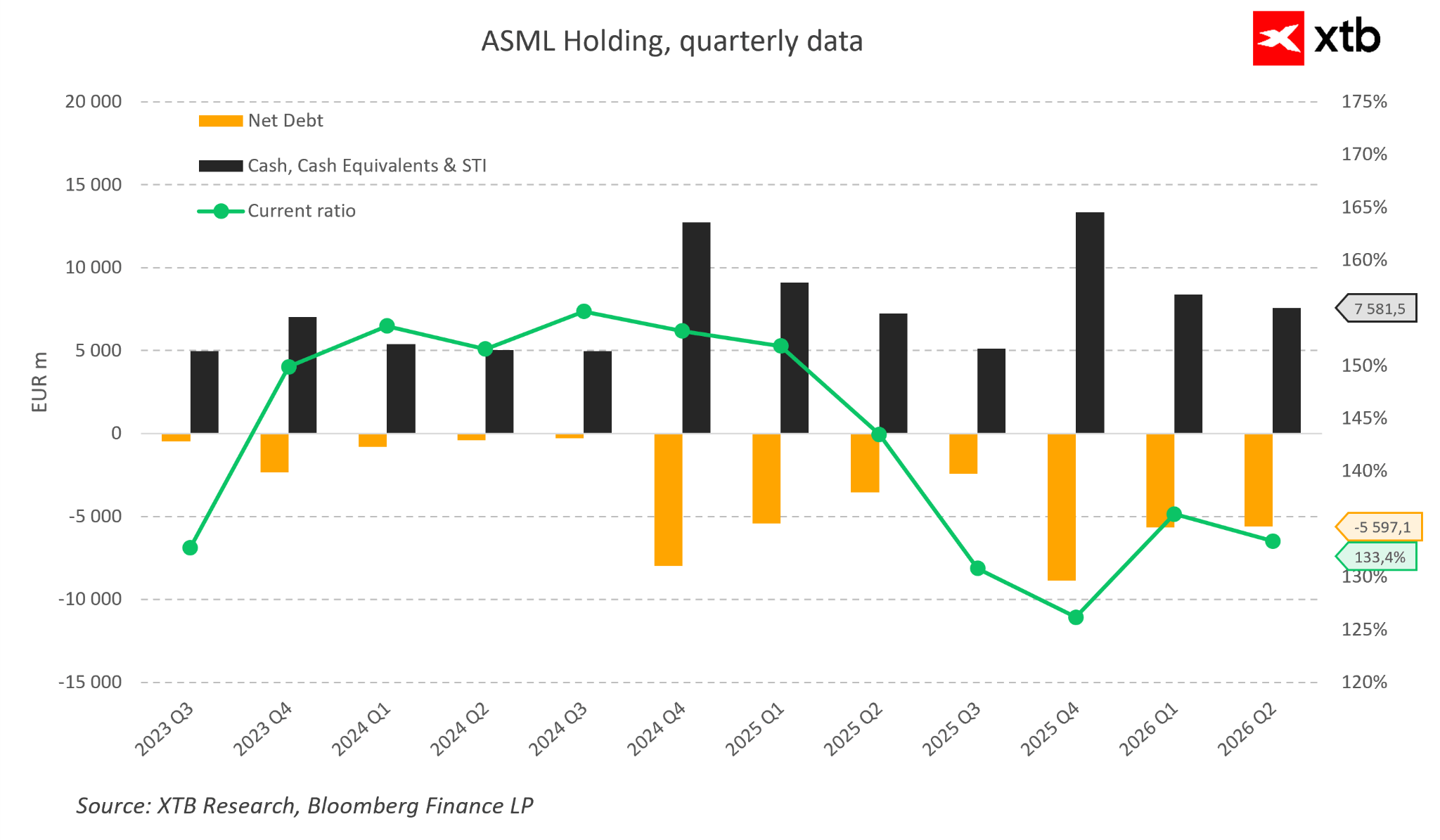

The company’s financial position is another major strength. ASML holds €7.6 billion in cash and cash equivalents, while its current ratio indicates a healthy balance-sheet structure. Controlled debt levels provide the company with significant flexibility to pursue further investments and maintain its technological advantage. This is especially important in the semiconductor industry, where progress requires continuous increases in spending on research, manufacturing capacity, and new solutions.

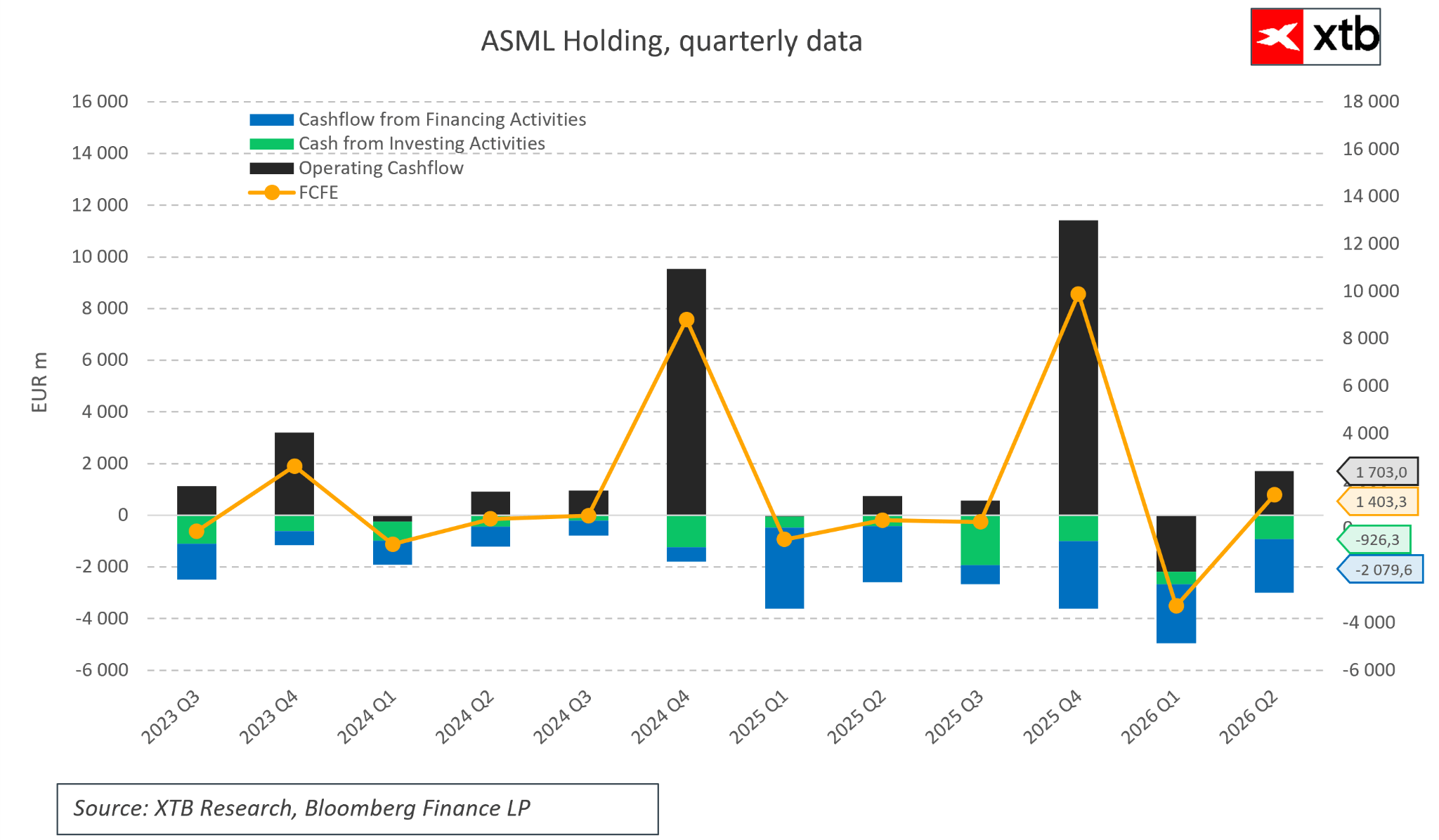

The cash-flow situation also remains strong. ASML’s core operations consistently generate positive cash, allowing the company to finance further growth without excessive reliance on external funding. Higher volatility in free cash flow available to shareholders is a natural consequence of large investment cycles and the characteristics of the industry, but it does not change the fact that ASML remains a highly effective cash generator.

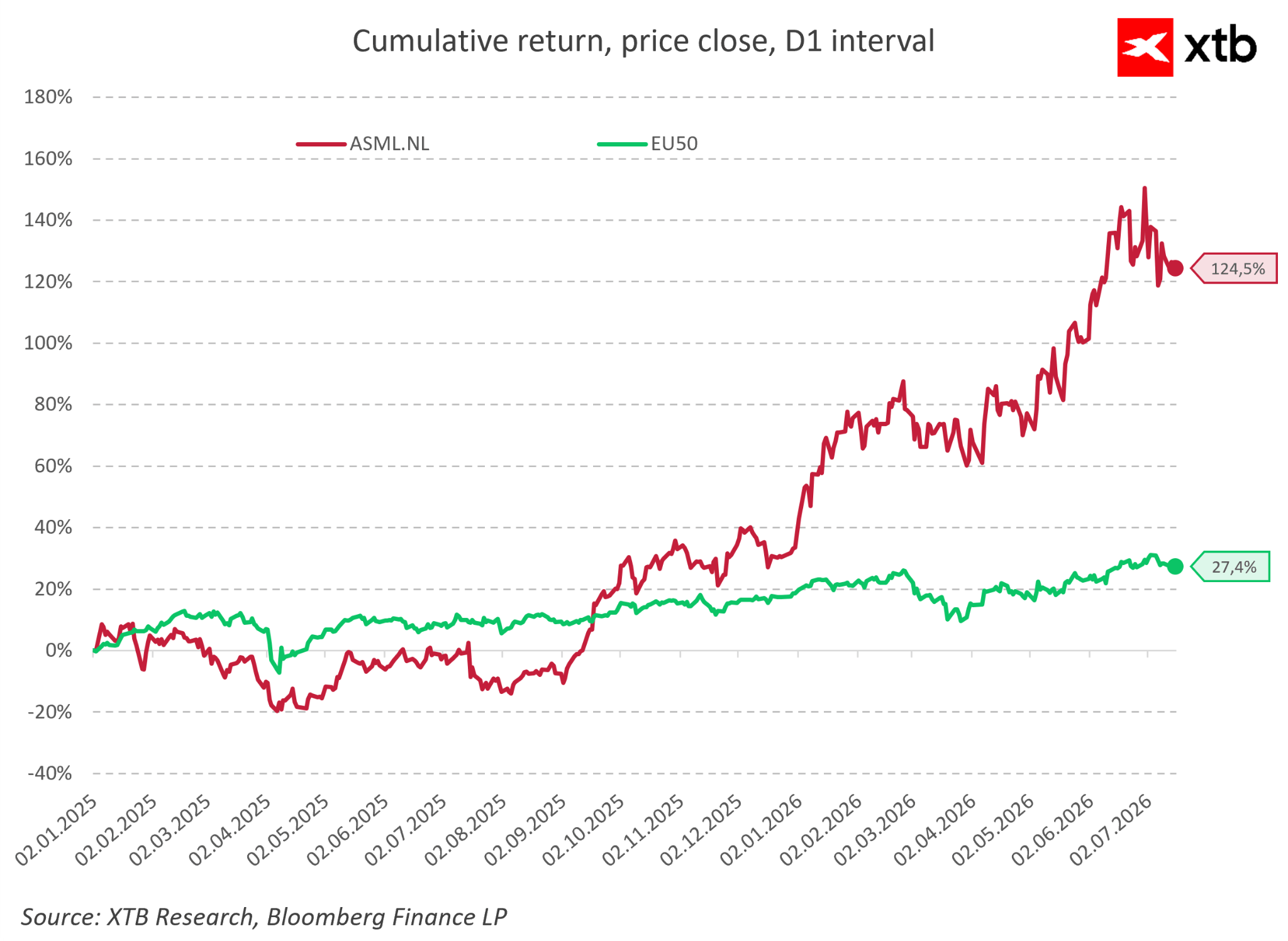

Investors have also recognized the strength of the business. Since the beginning of 2025, ASML’s share price has increased by more than 120%, while the EU50 index gained approximately 27%. Such a significant difference shows that the market values not only improving financial results but also the strategic importance of ASML for the entire semiconductor ecosystem. At the same time, such a strong share-price performance means expectations for the company’s future remain extremely high, and future earnings will need to continue confirming the current growth trajectory.

What Could Threaten ASML’s Further Growth?

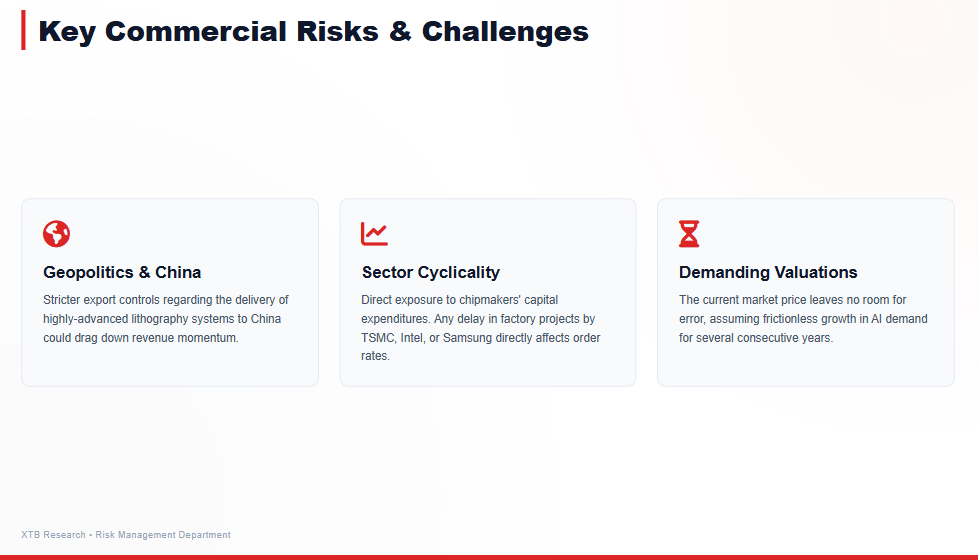

ASML is one of the highest-quality companies operating in the semiconductor sector. However, even such a strong competitive position does not mean that the business is completely immune to external factors. The biggest risks facing the Dutch company do not currently come from the possibility of losing its technological advantage, as developing competitive solutions in advanced lithography would require enormous financial resources, many years of research, and the creation of an entire supplier ecosystem. Much more important are factors related to the cyclical nature of the semiconductor market, customers’ investment decisions, and geopolitical developments.

ASML’s business model is directly linked to the spending plans of the world’s largest chip manufacturers. Purchasing advanced lithography systems is part of long-term factory expansion strategies and requires enormous capital investment. This means that the company benefits from structural trends such as artificial intelligence development, data center expansion, and growing demand for computing power, but at the same time remains vulnerable to periods when semiconductor manufacturers reduce or postpone their investments. Even the most advanced technology cannot generate growth if customers decide to delay the construction of new production facilities.

One of the most frequently discussed risks for ASML’s future remains China. In recent years, Chinese semiconductor manufacturers have become important customers for the technologies offered by the Dutch company, particularly in more mature manufacturing processes. At the same time, tensions between the United States and China have resulted in export restrictions affecting the most advanced lithography systems. At first glance, limiting sales to China may appear to be one of the greatest threats to ASML’s future growth.

However, the situation is more complex. The value of ASML does not come from exposure to one specific market, but from the fact that it provides technology required by the entire global semiconductor industry. The largest chip manufacturers, including TSMC, Samsung Electronics, and Intel, continue to invest in future generations of chips, while the growing importance of artificial intelligence requires increasingly advanced manufacturing processes. From this perspective, the key question is not whether ASML will maintain every individual market, but whether global demand for the most advanced semiconductors will remain strong enough.

This does not mean, however, that China-related risks can be ignored. Export restrictions may affect the pace of sales growth and contribute to greater short-term earnings volatility. In addition, China continues to invest heavily in developing its own semiconductor industry, meaning that over the long term it may attempt to reduce its dependence on foreign suppliers. Nevertheless, ASML’s current technological advantage remains enormous, and creating an alternative to the most advanced lithography systems would require many years of development and the recreation of a highly complex supply chain that the company has built over decades.

Ultimately, the greatest challenge for investors is not the risk that ASML will lose its technological advantage. The much more important question is whether current market expectations are too ambitious. The company is now viewed as one of the biggest beneficiaries of artificial intelligence development and the ongoing digital transformation of the global economy. As a result, its valuation assumes that high growth rates, exceptional margins, and strong demand will continue for many years. If the semiconductor investment cycle slows faster than the market expects, even a business of outstanding quality may struggle to maintain its current valuation levels.

The investment risk in ASML is therefore not primarily related to the possibility of losing its competitive advantage. The more important question is whether the entire semiconductor market will continue expanding quickly enough to justify current investor expectations.

Does ASML’s Current Valuation Still Leave Room for Further Growth?

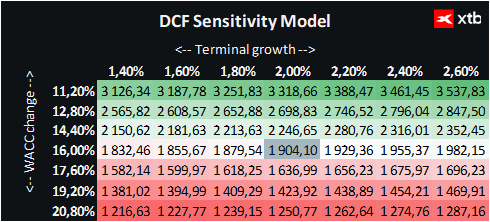

We present an ASML Holding valuation based on the discounted cash flow (DCF) method. It should be emphasized that this valuation is provided for informational purposes only and should not be treated as an investment recommendation or a precise estimate of the company’s intrinsic value.

ASML is a company whose value is driven primarily by its unique position within the global semiconductor ecosystem. The company remains a key supplier of the most advanced lithography systems, and its business benefits from long-term trends related to artificial intelligence, data centers, and rising demand for increasingly sophisticated semiconductor solutions.

In the prepared base-case scenario, the DCF valuation indicates a fair value of approximately €1,904 per ASML share. With the current market price of around €1,546, this implies potential upside of approximately 23%.

The result suggests that, under the adopted assumptions, the market may not be fully pricing in ASML’s long-term growth potential. The company possesses several characteristics that justify a premium valuation: exceptional technological leadership, extremely high barriers to entry, the ability to maintain above-average margins, and exposure to one of the most important technological trends of the current decade.

At the same time, it is important to remember that in the case of high-quality companies, an attractive business does not automatically mean an attractive investment opportunity. ASML’s valuation depends heavily on whether the company can maintain its current growth rate, high profitability, and continued demand for the most advanced semiconductor manufacturing technologies.

The most important factor influencing ASML’s future value remains the continued expansion of the semiconductor market. If investments related to artificial intelligence, data centers, and next-generation chips continue in line with current expectations, ASML has the potential to further increase revenue and create additional shareholder value.

On the other hand, the very high quality of the business means that investor expectations remain extremely elevated. Therefore, maintaining strong results alone may not be enough — the company may need to continue exceeding market expectations in order to support further valuation growth.

A Strong Business Facing High Expectations

ASML remains one of the most important companies in the entire semiconductor market. Its significance comes not only from its unique position in advanced lithography but also from the fact that its results provide insight into the health of the broader technology ecosystem.

The current investment cycle driven by artificial intelligence, data centers, and rising demand for computing power creates a highly favorable environment for ASML’s continued development. High margins, a strong balance sheet, and enormous barriers to entry make ASML a business of exceptional quality.

At the same time, investors must remember that such a strong competitive position is already reflected in market expectations. The key question is not whether ASML is an excellent company, but whether the semiconductor market will grow quickly enough to justify further increases in valuation.

ASML’s future will depend on the balance between two forces: the extraordinary strength of its business model and the very high expectations already embedded in its share price.

Daily Summary 🗽 Wall Street Holds Firm Despite Weakness in Memory Stocks, Rising Oil Price

Moderna shares slide despite mFlusiva success 📉 What's next for the mRNA vaccines market giant?

Stock of the Week: Arista Networks—A Second-Tier Technology with Top-Tier Results

US Open: S&P 500 shows strength as semiconductor lags 🚩 Western Digital down 12%

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.