- Why rising global bond yields could crush the gold price

- G7 implied yields have reached their highest levels for more than 2 decades

- Why a 10-year US Treasury yield is bad news for gold

- Gold loses its shine as next move for Fed is likely to be a hike

- Why rising global bond yields could crush the gold price

- G7 implied yields have reached their highest levels for more than 2 decades

- Why a 10-year US Treasury yield is bad news for gold

- Gold loses its shine as next move for Fed is likely to be a hike

The recent spike in global bond yields has left investors pondering whether the gold price may have passed its peak. Fundamentals are also starting to turn against gold bulls.

The market reaction to the US producer price report for April, which saw producer prices rise 1.4% last month, the largest monthly gain since 2022, has been moderate so far. The annualized producer price index rose to 6%, driven, unsurprisingly, by a sharp rise in energy prices. However, gains were broad based, with a 2.7% gain for trade services. This suggests that higher energy costs and tariffs are having a large impact on prices as we move through Q2.

Yields on the 10-year Treasury yield may have only rose 3bps, but today’s move is significant since the 10-year yield is now back above 4%, the highest level of the year so far. We are living in a high inflation environment, and the US economy is also showing signs of strength, for example, a robust labour market. This is likely to give the Fed pause for thought, even if the incoming Fed chair, Kevin Warsh, who will take up his new position later this week, is a Trump faithful and reportedly has dovish leanings.

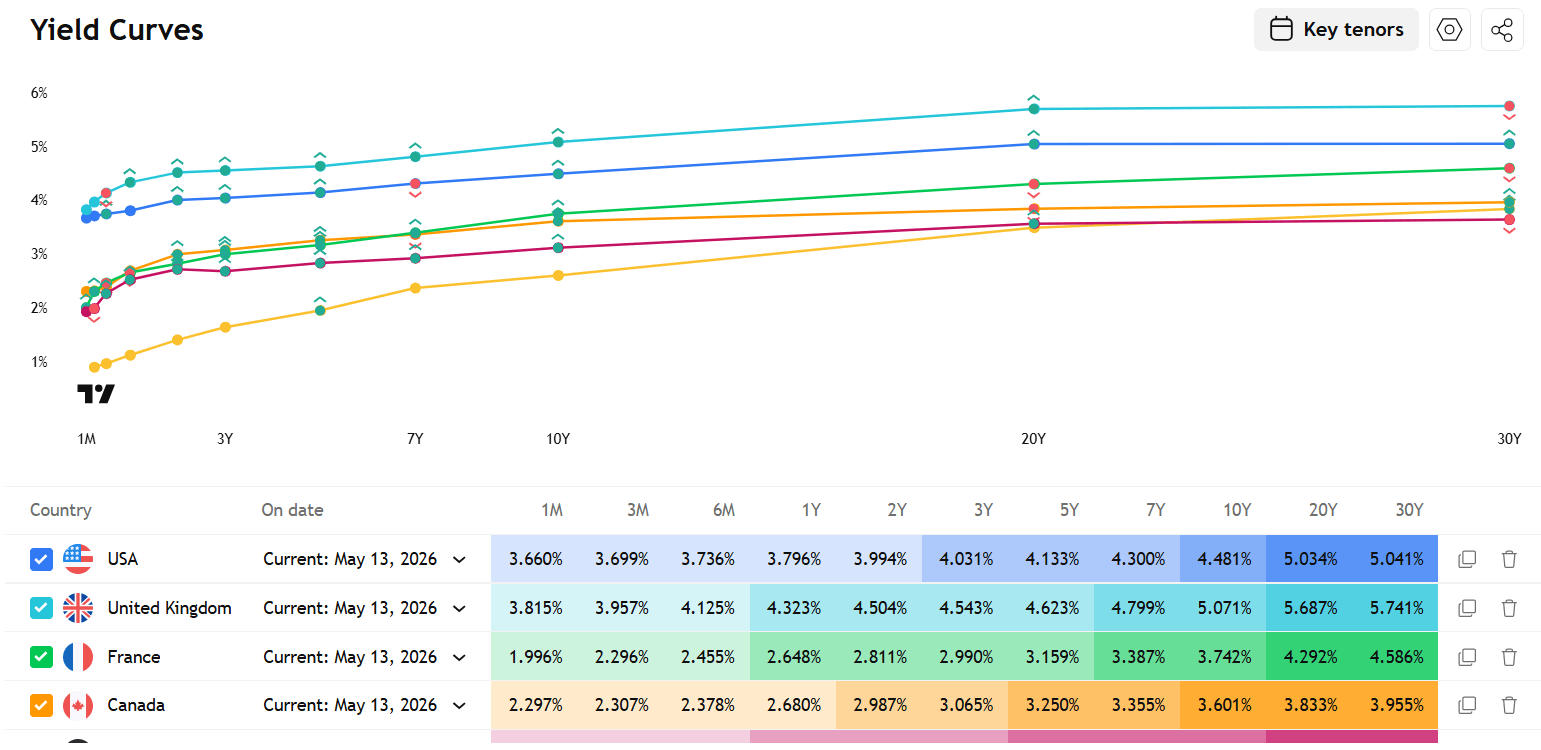

This week’s US inflation data, including a hotter than expected 3.8% reading for April CPI, will make it almost impossible for the Fed to cut rates in the foreseeable future. In May, the US CPI rate is expected to rise to 4%, double the Fed’s target rate. The Fed Fund Futures market is pricing in a 30% chance of a 25bp rate hike by the end of this year, with an 80% chance of a hike in rates in 12 months’ time. The US is not the only country now facing rate hikes, there are also hikes expected from the ECB and the BOE, and the implied yield on long term borrowing costs for the entire G7 is at elevated levels for the long term, as you can see below.

Chart 1: G7 bond yield curves, implied rates are at elevated levels compared to recent history

Source: XTB and Trading View

This bond market problem is likely to become a big problem for the gold bulls. The issue with gold is that it does not yield anything. It produces no income, no interest and no dividend, so when you hold gold, you give up gains that you could earn elsewhere. Gold can outperform when yields are rising, but only if real yields (when adjusted for inflation) are negative. Right now, yields are higher than inflation rates, including in the US and the UK, which could weigh on gold’s attractiveness.

Gold also suffers from a strong dollar. The US dollar has been one of the strongest global currencies so far this year, and when it rallies it can weigh on the price of gold. This is because the yellow metal is priced in USD, so you need fewer dollars to buy it. A strong dollar can also dampen foreign demand for gold.

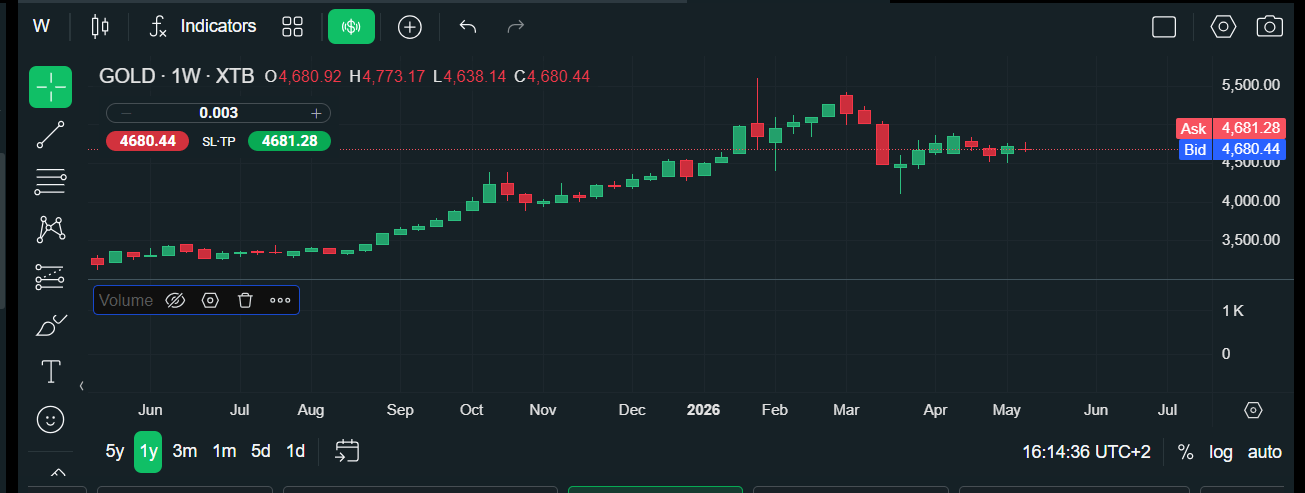

The gold price is more than $500 from its early March peak. It has backed away from March’s record high above $5,200 per ounce and has not acted like a safe haven during the war in the Middle East. The rise in bond yields that was triggered by the energy price spike has made gold unattractive in the current environment. With the US -10-year Treasury yield potentially staying above 4% for the long term, the gold price is at risk, with a break below recent lows at $4,575 an ounce a clear bearish signal that could open the gates to further losses in the coming months.

Chart 2: The Gold price

Source: XTB

Overall, there are growing signs that a prolonged energy price spike, inflation risks and political issues could keep global bond yields higher for longer. Rising yields mean that assets like bonds start to pay more, so gold, which pays nothing to its owners, starts to lose its shine.

Daily Summary: Chip War Weighs on Wall Street as Oil Plunges After US–Iran Ceasefire ⭐

Nasdaq-100 under pressure after chip sell-off

China Is Building Its Own Chip-Making Machines. ASML Under Pressure as the Technology War Enters a New Phase

US Open: Wall Street Rebounds After US Iran Ceasefire

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.