European and U.S. defense companies are reporting further orders that point to sustained demand for military equipment. After many months of persistent declines, this may be the pretext the market has been waiting for to consolidate and return to gains on the back of record defense spending.

Europe

The single biggest piece of news from Europe is Saab’s contract with Sweden’s FMV agency for 16 Gripen E fighter jets intended for Ukraine. The value of the agreement is approximately SEK 24.6 billion, and the order is to be booked in Q3 2026. Deliveries are scheduled for 2029–2030, and the package includes not only the aircraft themselves but also spare parts and related equipment. The company’s shares are up more than 3%.

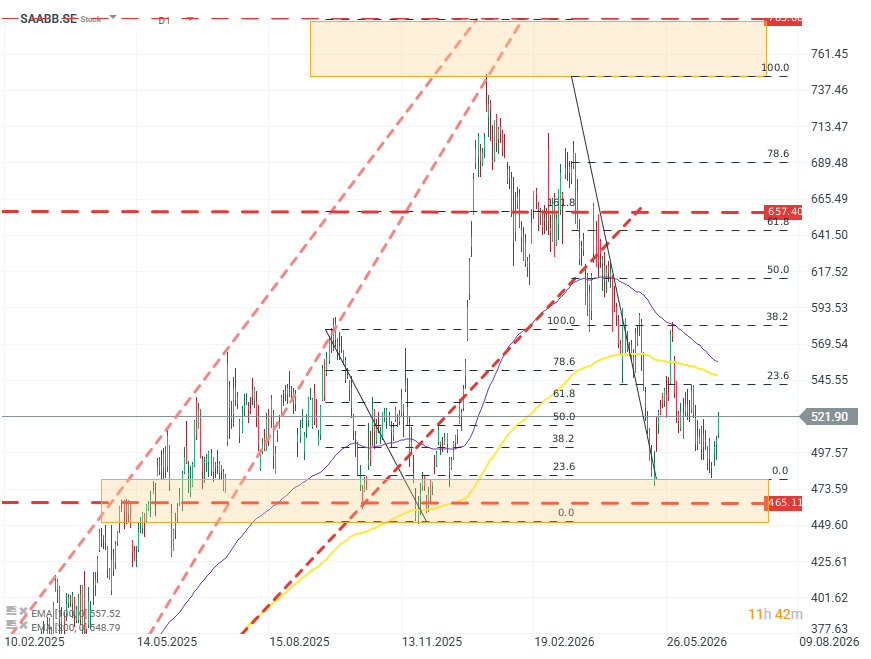

SAABB.SE (D1)

After two waves of strong gains that took the price from around SEK 165 to about SEK 750, the stock saw a sharp pullback and has now entered a consolidation phase around SEK 500. Holding above the lower boundary of the resistance zone near SEK 465 may indicate buyers trying to regain the initiative and push the price at least above SEK 600. Key to watch remains the behavior of the 100/200 EMAs, where there is a risk of a so‑called “Death Cross.” Source: xStation5

In parallel, Rheinmetall reported an order from Ukraine for artillery shells and propellant charges. The contract value was described as “high tens of millions of euros,” and execution is to be completed in Q1 2027. Production has already started at the company’s facilities in Spain. The group’s shares are up more than 4%.

The defense sector is also facing the upcoming IPO of KNDS. The manufacturer (among other things) of Leopard 2 tanks is expected to debut on the Paris stock exchange within a few months. This will be an important test of investor sentiment toward defense stocks, or potentially a source of support. Source: Bloomberg Finance

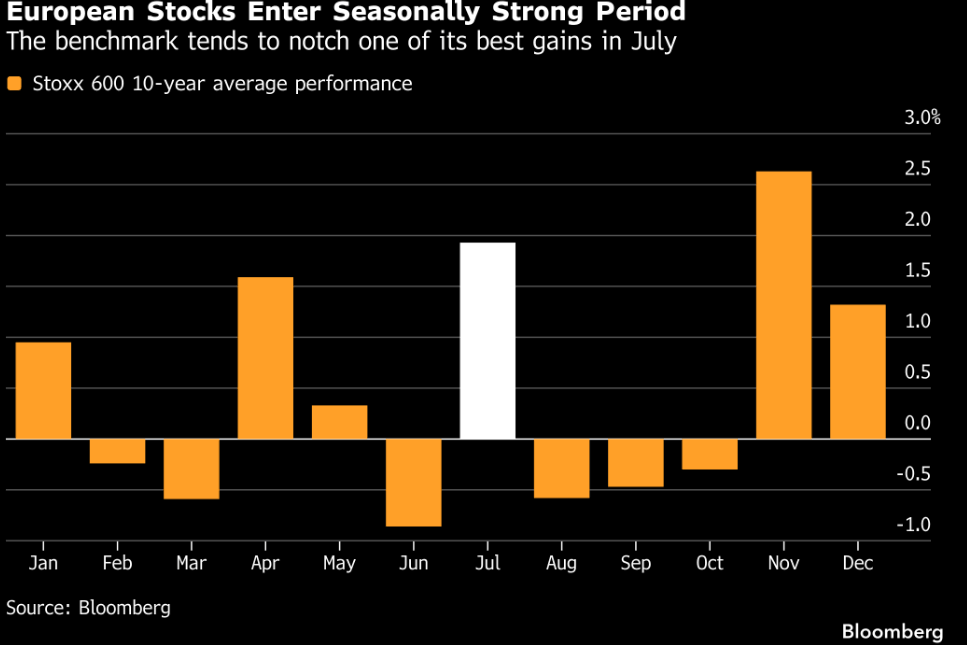

In the context of the broader European market, it is worth remembering that July has historically been a growth period for equities in Europe. Source: Bloomberg Finance

USA

On the U.S. side, the most important item is a package of contracts for Lockheed Martin with a total value of more than USD 3.1 billion. The largest portion of this amount is a USD 2.99 billion contract for the production of Sentinel A4 radars and engineering services. Work is to continue until June 2031. Lockheed also received a contract related to the modernization of Spain’s Álvaro de Bazán-class frigates. In pre-market trading, the valuation does not appear to be reacting to the news, which may indicate that investors had already priced in a similar contract earlier.

Northrop Grumman received three contracts totaling about USD 68 million. The largest of them, worth USD 49 million, concerns the maintenance of the Joint Tactical Ground Station program, including logistics support and engineering services. The company is up about 1% in pre-market trading.

Boeing, meanwhile, received a USD 49.5 million contract for work related to controllers for air-launched cruise missiles. The agreement includes test sets and the refurbishment of controllers needed to sustain the ALCM system. Project completion is scheduled for June 2033. This company also is not reacting in pre-market trading, though the situation may change after the session opens.

From a capital market perspective, the most important element is the overall picture: the defense sector continues to benefit from a long cycle of military investment. In Europe, the main driver remains the war in Ukraine and the rebuilding of NATO capabilities, while in the United States there is continued funding for radar, missile, and modernization programs, and more recently, expectations of replenishing ammunition stockpiles used during operations in Iran.

New contracts do not immediately change the entire earnings picture for the largest companies in the sector, but they may strengthen market sentiment which, based on forecasts and valuation multiples, may still be underestimating the real growth potential of these companies.

The challenge for firms, however, will still be not only maintaining the inflow of orders, but also converting them into revenue quickly, sustaining margins, and expanding production capacity without excessive cost growth.

Kamil Szczepański

Financial Markets Analyst, XTB

Daily Summary: Failure of negotiations in the gulf, oil and gas prices soar

Berkshire earnings: What do the reports say about the market’s direction?

US OPEN: Debt and the Strait of Hormuz fuel growing concerns.

Intel Needs $15 Billion. Is It a Financial Problem or the Price of an Ambitious Expansion?

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.