The market mood is very different at the start of the week compared to Friday. US futures are lower, and markets in Europe are in the red, the Dax and the Cac are both down more than 1%, while the FTSE 100 is more resilient and is lower by 0.4%, as energy majors rise on the back of a higher oil price. BP and Shell are both higher, by 3.5% and 2.5% respectively. Volatility is back, and the oil price is higher by more than 5%, Brent crude is back above $95 per barrel, up from $90 a barrel on Friday’s close.

Financial markets have been jostled by news flow over the weekend. On Friday the Strait of Hormuz was back open and tankers were passing through the waterway. Iran halted all traffic through the Strait on Saturday, claiming that the US had broken the terms of their agreement, and then on Sunday the US Navy intercepted an Iranian ship on the coast of Oman, fired at it and boarded the vessel.

The situation has deteriorated and once more traffic through the Strait of Hormuz is at a standstill. Today’s jump in oil prices and the pullback in stocks is a reminder that the current ceasefire that expires on Wednesday is fragile. The latest round of peace talks in Pakistan scheduled for Monday are now in jeopardy. Although a US delegation is in the region, Iran has rebuffed these talks, and it is unclear if they will take place. Failed negotiations at this stage is problematic since it is an obstacle to negotiating a longer ceasefire, the current one expires on Wednesday. Unless relations between the US and Iran improve in the next two days, we could see a resumption of the bombing campaigns from both sides, and more volatility for financial markets.

The diplomatic setback has knocked market confidence at the start of this week, and we expect to see an unwinding of some of Friday’s positions as the market rapidly prices out the prospect of energy supplies returning to normal. This has big implications for bond yields and interest rate expectations. However, it is worth noting that not all of Friday’s decline in oil prices and surge in stock prices has been reversed, about half of Friday’s fall in the oil price has been clawed back early on Monday. This suggests that there is some residual hope in the market that the ceasefire will hold, and the Strait will reopen. The fact that the oil price has not yet crossed the psychological barrier of $100 per barrel is also significant.

The reality is anything could happen this week. Is Trump escalating the conflict to deescalate it in the coming days? This is one of his well-known tactics. Will he post something on Truth Social to say that peace talks are back on? One thing we know, the Iranians are not rolling over for the President, which makes this a tricky war for the US to end.

In this environment, markets are likely to remain focused on geopolitics this week although there are economic data releases and earnings report to be aware of. The S&P 500 ended last week at a record high, led by the tech titans. However, we doubt that the index will be able to keep hold of the 7,000 handle for long, if the situation between Iran and the US does not move in a more positive direction soon.

Chart 1: Nasdaq 100 could give back gains on Monday

Source: XTB

Events to watch:

1, UK economic data

The UK is in focus this week, as we get the latest labour market report and the March CPI reading. The unemployment rate is expected to remain steady at 5.2% for the three months to February, and average earnings excluding bonuses are expected to recede to 3.5% from 3.8% in January. The bounce back in GDP in February makes this labour market report hard to predict, however, there are few people who expect a strengthening of the jobs market, which has weakened substantially in recent months.

The CPI reading for March is arguably of greater importance for UK asset prices, since it will give us an early sign of how the energy price spike impacted the inflation outlook. Analysts expect headline CPI to rise to 3.3% from 3% in February, and core prices are expected to remain stable at 3.2%. Rising petrol and diesel costs are likely to be the biggest driver of the increase in the CPI reading last month. Surging oil and gas prices have been felt by those not on the energy prices cap, which could also add upward pressure to the inflation reading. Producer prices are also reported on Wednesday, and they should tell us how quickly businesses are passing on rising costs to consumers. We think that output prices could rise sharply as businesses cannot absorb more cost pressures in the current environment.

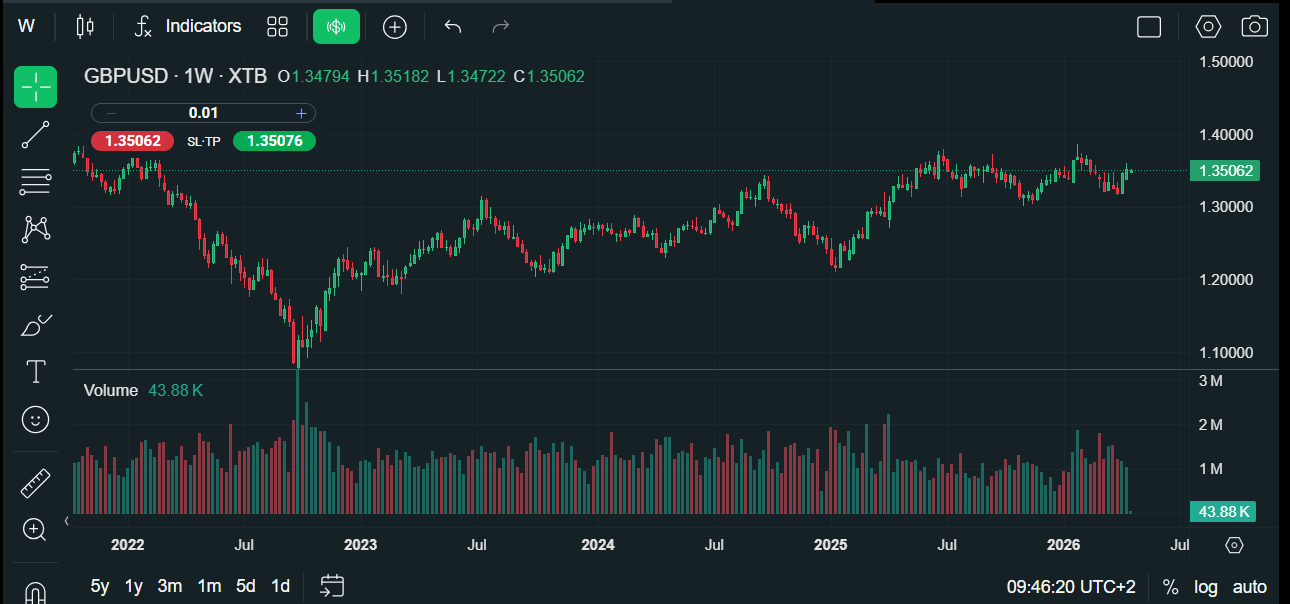

Geopolitics continue to be the biggest driver of UK asset prices right now. Added to this, inflation could fall back quickly if the decline in the oil price is maintained. The oil price plunged below $90 per barrel at the end of last week, and although it has risen on Monday, it is still below $100 per barrel. The market may choose to look through a spike in inflation in March, as it may not continue in the coming months. Any knee jerk reaction higher in the pound, which is already trading above $1.3500, could be faded if the price of oil manages to stay below $100 per barrel in the next few days.

Chart 2: GBP/USD

Source: XTB

2, Kevin Warsh Senate Confirmation Hearing

This Tuesday, 21st April, we get the first Senate Confirmation hearing for Kevin Warsh, who is President Trump’s pick to the be the next chair of the Federal Reserve once Jerome Powell steps down in May. This is a market moving event, and investors and traders will be eagerly watching to see what Warsh has to say about inflation and the direction of monetary policy. The focus will be whether Warsh is willing to look though the recent energy price shock and continue to support lower interest rates, which could boost US Treasuries and weigh further on yields, which fell sharply on Friday on news that the Strait of Hormuz was reopen. If Warsh sounds like he continues to support lower interest rates, a position favoured by the President, it could boost the short end of the US Treasury curve, although the long end may come under pressure, as the yield curve steepens.

There is a risk that a dovish Warsh could spook financial markets if a potential Fed chair does not take the threat of inflation seriously. This could damage the future Fed’s credibility. Warsh will need to walk a narrow path on Tuesday. On the one hand, he needs to show that he is attentive to upside inflation risks, on the other hand he may point to productivity gains as justification for future monetary policy easing.

Warsh’s comments this week could disrupt the view that he is a dove, which may set the stage for a volatile day for markets, especially Treasuries. The ideal outcome for markets would be commentary from Warsh about the potential for a lower terminal rate, while setting a high bar for rate cuts in the near term. If he can keep the door open to rate cuts while also hinting at future easing, then the market reaction could be limited, and he would also prove his communication skills.

Warsh’s nomination to the position of chair is not straight forward. Even if he passes Tuesday’s Committee hearing, a full Senate vote is required. The Republicans hold a narrow majority in the Senate, and a single defection could make it impossible for Warsh to take the reins when Powell steps down on 15th May. Ironically, it is Republican Senator Thom Tillis who could hold up Warsh’s nomination. He has vowed to block all Fed nominees until the Department of Justice drops its criminal investigation into Jerome Powell. This is unlikely to happen, due to the feud between Trump and Powell. While the focus is on what Warsh has to say, if his nomination is delayed then Powell has vowed to stay on as interim chair until a new nomination is passes. However, Trump has threatened to fire him if he does this. If this were to happen, concern about Federal Reserve independence could come back to the fore, weighing on the dollar and US asset prices more broadly.

3, Earnings to watch

While geopolitics remains centre stage at the start of this week, there are some key earnings reports to watch out for, including the first Q1 earnings update from the Magnificent 7. 88 S&P 500 members will report results this week, including Tesla and Boeing, along with Intel. So far, earnings season has been strong, with 86% of the companies who have reported results beating expectations.

Wednesday will be the main day to watch, with both Boeing and Tesla reporting results. Tesla will report earnings after the US closing bell. Last quarter, Tesla’s earnings topped estimates, but overall 2025 was disappointing for Tesla and annual revenue fell for the first time. Analysts expect the company to bounce back in 2026, and YoY earnings growth is expected to come in at 40% for Q1. Tesla has already reported deliveries of 358,023 vehicles in Q1, which is higher than deliveries in Q1 2025. This suggests that demand for EVs could rise on the back of the conflict in the Middle East and surging gas prices. Model Y was the top selling Tesla car last quarter, and demand for Tesla vehicles surged in Europe after weak demand last year.

The key for investors is capex spend. Tesla has spent huge amounts of money on building out its AI capabilities, and its latest guide for capex this year was $20bn. However, some analysts are concerned that this is too low and does not include the potential spend for Musk’s latest projects including Terafab and Solar fab, both are likely to come with hefty price tags.

Tesla’s share price surged on Friday and is up 15% in the past week as US stocks reached record highs. However, its share price is still lower by 12% YTD. Its share price has fallen after two of the last three reports, and Tesla does not have a great near term track record of boosting investor demand for the stock after announcing earnings and future forecasts. A liberal increase in capex plans for this year could knock investor sentiment once again.

Intel is also worth watching, last quarter its stock price fell sharply after its guidance was weaker than expected. Analysts are negative on revenue for Q1 and expect to see a sharp deterioration compared to Q1 2025. However, some analysts see the bar as too low coming into this earnings season, so Intel has the potential to surprise on the upside. PC demand is expected to remain resilient, and the company’s CPU demand has surged on the back of continued AI growth. Its AI unit was able to put up prices last quarter, which should maintain profit margins, and the company could give favourable forward guidance.

However, it is worth noting that the stock has a tendency to fall after earnings reports and has done so after 4 of the last 5 earnings updates.

Live Market Update: UK Economy & Fed

ASML sell-out: Dreams and rumors will not break the monopoly

AI trade loses momentum, as LVMH fails to impress

Chart of the Day: Who suffers from the oil price drop? (28.07.2026)

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.