- Peace talks stalemate, but hopes grow a deal can be found

- Will Iran be forced to negotiate as oil storage reaches capacity?

- US stocks priced for perfection, can Warsh news push them higher?

- US stocks outperform Europe

- Tech overtakes defense as top sector

- Central bank meetings: are they still willing to look through the energy price spike as tensions persist?

- Earnings to watch: big week for the Magnificent 7

- Peace talks stalemate, but hopes grow a deal can be found

- Will Iran be forced to negotiate as oil storage reaches capacity?

- US stocks priced for perfection, can Warsh news push them higher?

- US stocks outperform Europe

- Tech overtakes defense as top sector

- Central bank meetings: are they still willing to look through the energy price spike as tensions persist?

- Earnings to watch: big week for the Magnificent 7

As we start a new week, we have a central bank bonanza to look forward to, including potentially the last FOMC meeting where Jerome Powell is chair, a Bank of Japan meeting, and an ECB and BOE meeting to digest. There is also a swathe of economic data releases, including the first reading of Q1 GDP in the US and ISM data for April, along with inflation data from the Eurozone, and money supply and house price data from the UK. However, the focus for markets will still be the news flow coming from the Iran conflict.

Crude oil prices have climbed at the start of the week, and Brent is higher by more than 1.5% this morning and is above $106 per barrel. It had been above $107 per barrel earlier today, but it pared gains after reports that Iranian officials have proposed a new plan to the US to reopen the Strait of Hormuz. We need to hear from the US to see if this plan will bear fruit and reopen the Strait, but as the conflict drags on, investors are getting worried about the impact on energy prices. There are growing expectations that the oil price will remain higher for longer, as the blockade on the Strait enters its third week. Goldman Sachs has increased its Q4 oil price target to $90 per barrel, from $80, as disruption to production persists for the coming months.

Will latest Iran plan reopen the Strait?

Peace talks stalled at the weekend, and we need to hear whether the US will accept Iran’s proposal around the Strait. The most likely scenario is that more talks are scheduled to discuss this latest plan. The global economy will be counting on this latest proposal to finally open the Strait. Stock markets have been resilient so far to the blockade of the Strait, especially in the US. If there is no flow of traffic for another week, sentiment might show signs of weakening. Futures prices are pointing to a mildly positive open for the main European indices, and US futures prices are little changed, which suggests that investors remain optimistic that a solution can be found.

Will Iran be forced to negotiate as oil storage reaches capacity?

The longer the blockade lasts for the bigger risk there is to Iranian oil fields. They differ from other wells in the region because they work on low pressure. If they are shut down due to the blockade and a lack of storage, it could cause permanent damage to Iran’s energy infrastructure. Estimates of Iran’s oil storage are around 20 million barrels, this means that Iranian storage facilities could reach capacity in the next few days. If this happens, then the Iranian regime might be compelled to negotiate with the US and find a way to reopen the Strait of Hormuz.

US stocks priced for perfection, can Warsh news push them higher?

The S&P 500 and the Nasdaq are priced for perfection, both US indices closed at record highs at the end of last week on hopes that the US and Iran would restart talks at the weekend. Although the talks failed to materialize, we doubt that stock markets will fall sharply, as there is expectation that talks will resume soon. Markets could also be cheered by the news that the Department of Justice dropped a criminal investigation into the Chair of the Federal Reserve Jerome Powell. Senator Thom Tillis also said on Sunday that he would support President Trump’s pick to be Fed chair, Kevin Warsh. This means that Warsh’s confirmation to lead the Federal Reserve after Jerome Powell steps down in May, is all but assured.

Now that Warsh has a clear path to replacing Jerome Powell, it reduces the chance of President Trump firing Powell, who had promised to stay on as Fed chair on an interim basis, until a new chair was voted into position. This could have led to fears about Fed independence, and weighed on US Treasuries, and market sentiment more broadly. With that risk now eradicated, the focus will be on what Fed chair Powell does after his term expires next month. He remains a voting member of the Fed until 2028, without the threat of prosecution hanging over him, will he opt to retire? If so, this will mean that President Trump can choose another member of the FOMC board. Trump does not hide his preference for rate cuts, so there could be some expectation of a dovish shift at the Fed in the coming months, which may bolster risk sentiment in the short term.

US stocks outperform Europe

This may also help US stocks to continue to outperform their European counterparts. The Nasdaq closed higher by nearly 2% on Friday, led by Intel, which jumped 23% after a positively received earnings report that cements its position as a key AI player in 2026. The Nasdaq rose by 2.4% last week, the S&P 500 was higher by 1.28%. This compares with a 2% decline for the FTSE 100 and a 0.1% drop for the Dax. Tech is leading the market higher in the US, and the issue for Europe is that it is light on tech. The European market is also a growth taker market, this means that it relies on strong global growth and global themes to drive returns. With the oil price remaining elevated, and global growth threatened, this will limit European stock market upside. In contrast, US tech is rising on the back of lower interest rates, a falling oil price, continued AI spend and hopes that the AI theme has further to run.

Chart 1: S&P 500 vs. FTSE 100

Source: XTB

Tech overtakes defense as top sector

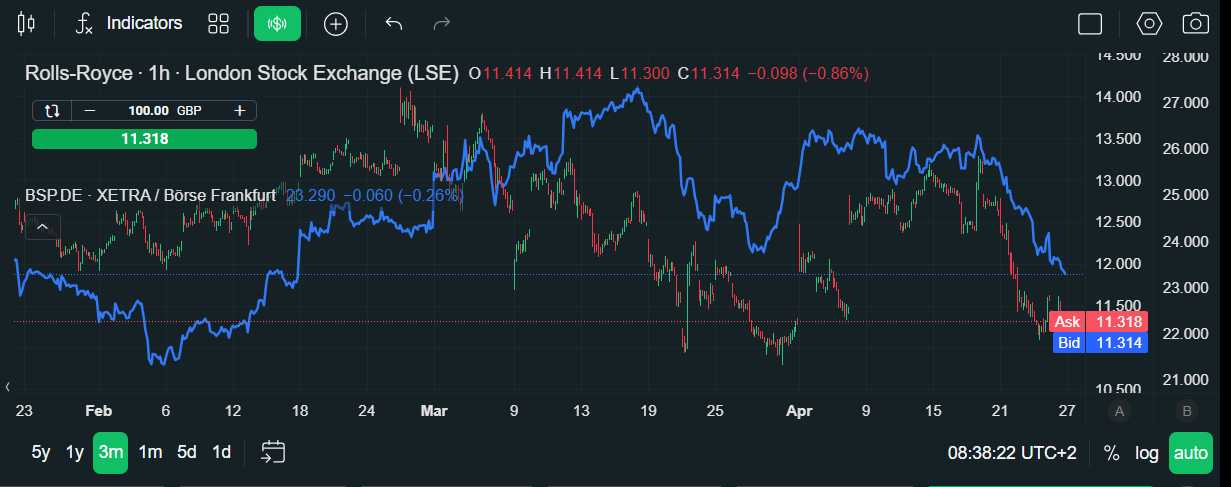

The top performers on the Nasdaq last week were solid AI names. Chipmakers Arm Holdings and AMD were the top two performers last week, rising 40% and 23% respectively. In contrast, defense stocks have been sold off as investors have rotated back into tech, and Lockheed Martin was the weakest performer on the S&P 500 last week, falling 3%. This is another reason why European indices are underperforming their US counterparts; they have several defense names that are coming under pressure. In the UK, Rolls Royce and BAE Systems both fell more than 9% and acted as a major drag on the FTSE 100. Rheinmetall also dropped 11% last week and hindered the Dax index.

US stocks are also benefitting from a strong earnings season. Of the 28% of companies in the S&P 500 that have reported earnings, 84% have reported earnings that were higher than expected, which is above the 5-year and the 10-year averages. There have been upside-earning surprises for the financial, industrial, communication services, and the tech sectors. These have balanced out earnings misses from the energy sector. Ironically enough, the energy sector has been a drag on the US index this year, however, that is unlikely to last into Q2 after the massive surge in the oil price.

Chart 2: Rolls Royce and BAE Systems fall out of favour even though the conflict in the Middle East is ongoing

Source: XTB

Earnings will be a key theme in the coming week, as five of the Magnificent 7 report. Below we look at two key themes that will drive price action in the coming days.

1, Central bank meetings

There is a whole suite of central bank meetings coming up this week, including the Fed, the BOJ, the ECB and the BOE. Analysts do not expect there to be any major change to rates this week from these meetings, and we may need to wait until May/June before central bankers will give their updated view on forward guidance. Energy prices remain elevated and there are concerns that supply chain disruption will increase stagflationary risks as the Strait of Hormuz has remained effectively closed for the best part of 2 weeks now. Investors will be scrutinizing central bankers’ views on the ongoing blockade and what it means for the future of policy and markets are likely to be extremely reactionary to these meetings, especially around the Fed meeting and the BOE meeting on Thursday.

This is likely to be the final meeting for Fed chair Jerome Powell. No new forecasts or Dot Plots are expected, which leaves asset prices vulnerable to the Fed’s views on the growth concerns versus inflation considerations. The market still expects the Fed to cut interest rates this year, and Warsh at the helm of the Fed is expected to reinforce the view that rate cuts are likely in the US by year end. For now, rates are on hold, but signs that the Fed will look through this period of elevated energy costs could boost sentiment in a market that is already optimistic about the future.

In the Eurozone, the ECB is also expected to remain on hold, however, the ECB could be more focused on the inflationary impact from the war due to its single mandate for price stability, and the fact that the Eurozone is an energy importer and could import inflation due to this price spike. A rise in inflation is expected across the currency bloc in April, and this could focus minds on the need to hike rates later this year if the Strait of Hormuz does not reopen soon.

The BOE will also announce its latest policy decision on Thursday. The market expects two rate cuts from the BOE this year, and it will be interesting to see if the Governor reacts to market expectations. So far, although inflation has risen in March, growth has held up well, including stronger retail sales and a drop in the unemployment rate. However, we think that the governor will take a cautious stance as the underlying UK economy remains weak, and rising energy prices could knock it even further. A hike could be coming if we see second round inflation effects like rising wages, however, there is no sign of that so far, and UK wages are at their lowest level in 5 years.

2, Earnings to watch

There are 160 S&P 500 members reporting earnings this week, including Meta, Apple, Amazon, Alphabet and Microsoft. General Motors and Robinhood will also be highlights. The biggest tech firms have a high bar to clear, given that there remains lingering concerns in the market about AI spending and investments. These companies need to show that revenues justify the level of capex the companies want to spend. Added to this, their stock prices have already rallied into earnings season, and they have all seen gains of more than 10% this month, with Apple rising 6%.

Alphabet is expected to report revenue growth of more than 20% YoY. There are expectations that the company will report improving monetization from its AI expenditure, particularly with greater uptake of Gemini. The risks to its earnings report are fears about future profit margins, and concerns about capex plans. Alphabet’s stock price tends to rally on the back of earnings reports, with an average gain of 1.3%.

Meta will also report results on Wednesday evening. Earlier in the year, Meta’s share price jumped after it reported stronger forward guidance, we will now see if Meta can deliver. YoY revenue growth is expected to be strong, and $55.5bn is expected. The company has beaten earnings expectations in every quarter for the last three years, so expectations are high that they will do so again. Investors want to see bottom line gains from its massive AI expenditure, and a clear strategy about what Meta’s newest AI mode, its Muse Spark, will do and how it will enhance customer experience at the tech giant.

Wednesday is heaving with earnings, as Meta also reports results. Microsoft has had a tough 2026 so far, and is down 12% YTD, after a tough Q4 earnings report and underwhelming earnings guidance. This quarter could be about redemption. The company is expected to report double-digit earnings growth for Q1 relative to a year ago. Its share price is higher by 12% in the past month, as excitement comes back to the market about the AI theme. On average, Microsoft’s shares tend to flatline during earnings reports, so hopes are high that this earnings report can buck the trend.

Apple is also in focus, however, it won’t just be revenues that investors want to hear about. We have already heard that Tim Cook is stepping down in September and John Ternus will succeed him. The company is expected to report revenues of $109.45bn for last quarter, but investors may want to get some sense of what Ternus will bring to Apple when he takes over later this year. Will he push Apple down the AI route, something Cook was unwilling to do?

Apple is also known for its shareholder sweeteners, and share buybacks and dividends could also be on the cards. This may boost enthusiasm for the stock, which is basically flat YTD.

Cocoa rises on a wave of rebounding demand in Asia. Europe remains in retreat

A win for England: first half growth on positive track, keeps pound buoyant

Chart of the day: Nasdaq futures dip 0.6% despite TSMC earnings beat! AI sanity check? (16.07.2026)

Gold Holds Above $4,000 🚩 What's Next for the Precious Metal?

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.