September has already thrown up some big surprises for financial markets. The Non-Farm payrolls report at the end of last week saw a 22k increase in payrolls for last month, well below expectations. This ignited fears about the outlook for the US economy. It triggered a rally in government bonds, particularly at the short end of the curve, and US and European stocks sold off at the end of last week. Futures are pointing to a mildly higher open for stock markets later today, the gold price is lower and the yen is weak across the G10 FX space after the Japanese PM resigned.

Momentum could pause as stock market assesses the outlook for the US economy

The stock market is starting to show signs of concern about the outlook for the US economy, as the jobs market deteriorates. The prospect of a slowing economy saw a rotation out of momentum stocks on Friday, like some big tech names including Nvidia, and into smaller cap indices and value stocks. For example, Nvidia’s share price dropped 2% on Friday and is down by 6% in the past week. Cracks are starting to appear in the AI trading narrative, as investors fret that a weak US economy could see the uptake of AI slow. This would be a major threat to the AI trade and for big tech, and we expect momentum in the US indices to pause, as investors assess the US economic outlook.

50bp September cut now on the cards

The payrolls report triggered a big recalibration in interest rate expectations in the US. There is now a growing chance of a 50bp rate cut in the US on 17th September, and the Fed Fund Futures market is pricing in 6 rate cuts in the next 18 months. This also triggered a sharp drop in Treasury yields, the 2-year yield is back at early 2024 levels at 3.5%.

The expected drop in borrowing costs did not propel global stock markets to fresh highs, and US and European stocks sold off by a similar amount last week. The S&P 500 fell 0.3%, while the Eurostoxx index was down 0.6%. The FTSE 100 eked out a 0.2% gain, due to big gains for gold miners including Fresnillo, which rose by 18% last week and Endeavour Mining, which was higher by 8.6%. Sometimes it pays off to be an index of dinosaurs.

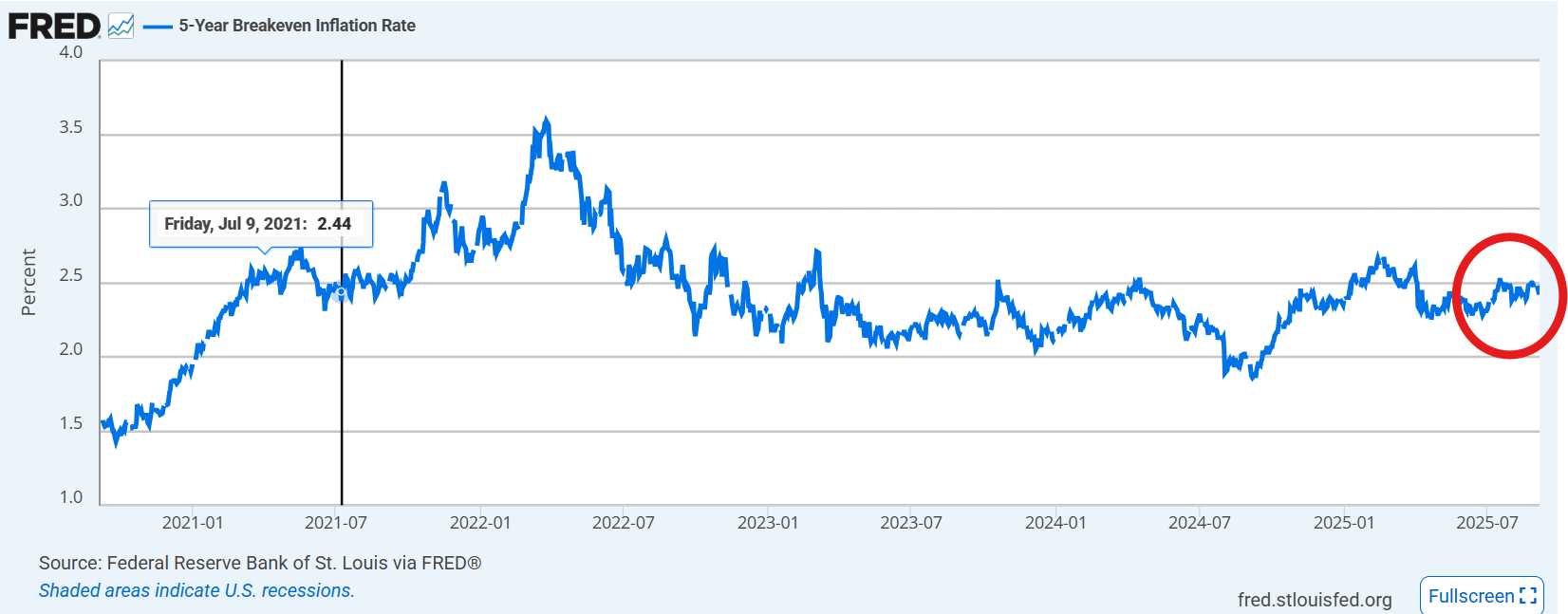

The gold price was a clear winner last week, and it rose by 4%. The yellow metal made multiple record highs and rose by $40 to $3,586 after the big miss for US payrolls. As mentioned, this sent the gold miners flying, and it is also suggested that there are lingering concerns about stagflation in the US economy. Bond yields are tumbling, and a rapid pace of interest rate cuts are being priced into the Federal Funds Futures market. The gold price is stabilizing at the start of this week, but we expect it to remain close to record highs. Interestingly, even as the gold price has surged, market-based inflation expectations have remained stable. The 5-year US Breakeven Inflation Rate is within its recent range, as you can see in the chart below.

Chart 1: 5-year US Breakeven Inflation Rate

Source: The Federal Reserve Bank of St Louis

Bond yields are tumbling, stocks have rolled over but remain close to all-time highs, and the gold price is soaring, yet inflation adjusted bonds are not flashing red. This does not add up, and it suggests that something may have to give. Either gold is overvalued, and stagflation fears are overdone, or the rest of the market needs to play catch up. The US CPI release later this week will be pivotal to determine what happens next as stocks are poised on a precipice as we move into the second week of the new month.

Opec + sends oil tumbling again

One of the reasons why the bond market may not be worried about inflation is due to the oil price. Over the weekend, Opec+ confirmed that they would add to their scheduled production increase next month. This move was expected by the market and the price of WTI oil fell 4% last week, while the price of Brent dipped by 3.8%. The Brent crude price is struggling to gain traction above $65 per barrel, and momentum is to the downside. A break below $65 per barrel would open the door to a deeper decline, back to the lows of May around $60 per barrel.

Ahead this week the focus will be on the US CPI report for August and the ECB meeting. Politics will also be in focus, as the French PM faces a key vote on his future on Monday, the markets will also be digesting the news that the Japanese Prime Minister Ishiba will step down. Below, we analyze what these events mean for markets.

1, French political risks

The French Parliament will hold a no confidence vote on the government of Francois Bayrou on Monday, which is likely to force Bayrou out of office. This would mean that France will have four governments in a year, as politicians try to push through Budget cuts to get the public spending. Last month, a French government minister said that the country may need an IMF bailout because its finances were so bad.

French political risks have weighed on asset prices in recent weeks. The Cac 40 is down 0.88% in the past month and has underperformed US and European indices. Added to this, French long-term debt has underperformed its peers, including the debt-laden UK, and 30-year yields have surged by 24bps in the past 4 weeks. Does this mean that all the political turmoil is priced in? The prospect of more budget deadlock is almost certain, and Bayrou’s near EUR 44bn of cuts are likely to be shelved by his replacement. There could also be growing calls for President Macron to resign, which could lead to a far-right replacement.

All of this could lead to further stock market weakness in France and higher bond yields. Already French stocks are trading at a discount to German stocks, the price to earnings ratio of the Cac 40 is 15 times, while the P/E ratio for the Dax is 17 times earnings. This gap could widen if France experiences a prolonged period of political turmoil.

Overall, there is a lot resting on this vote, and the markets will be taking notice of the outcome, as highly indebted nations cannot hide anymore.

2, US CPI could cause bond market ructions

This is undoubtedly the data highlight of the week. The market is expecting headline CPI to rise to 2.9% from 2.7% in July, and the core rate is expected to remain at 3.1%. Monthly increases in prices are expected to be 0.3%, which is uncomfortably high. Inflation has not been seen as a barrier to rapid rate cuts from the Federal Reserve. The options market has rushed to price cuts since the July payrolls report, the August report made a 50bp cut from the Fed more likely.

The options market is also expecting further gains for the US stock market, however, there is one risk that the market does not seem to be pricing in yet, the chance of an upward surprise in Thursday’s CPI report.

Tariffs and Donald Trump’s trade wars have clouded the outlook for inflation. This makes each report extremely meaningful. It also increases the chance of volatility. Over the summer, volatility in US stocks surged by more than 50% over key data releases including CPI and NFP reports along with Fed meetings.

The risk is that a hot inflation print could cause a rapid scaling back of rate cut expectations in the coming months, and this could trigger volatility for stocks, bonds and the dollar. This could be a sign that as we progress through 2025,the focus is switching back to the macro data, and away from politics and Donald Trump’s tariffs.

While we expect a rate cut at this month’s Fed meeting, the bigger risk is that an upside surprise in CPI will lead to a recalibration of expectations around how far and how fast the Fed will cut rates in the coming months.

3, ECB meeting: deliberately uninformative

Thursday is a busy day for financial markets. The US CPI report and the latest ECB meeting will be released on Thursday afternoon. The ECB is expected to hold rates steady at 2%, the highlight will be ECB President Lagarde’s press conference at 1345. There is less than one rate cut priced in for the ECB for the rest of this year, and rates are expected to bottom out at 1.73% by the middle of next year. Thus, we are getting extremely close to the ECB’s neutral rate, and we do not expect the ECB to give any clear direction on where rates will go next, suggesting that rates could be on hold for some time.

The ECB is likely to face questions about France and what could happen if there is a debt crisis in the second largest economy in the currency bloc. The ECB is no stranger to dealing with debt crises; however, the scale of the French fiscal challenge could even test the strength of the ECB.

The ECB will also release their latest staff forecasts this week, and the will include the impact on inflation and growth from the trade deal with the US that set tariffs on European exports to the EU at 15%. We expect the main message from the ECB to be that they are on hold for the long term, as the Bank waits to see how the economy absorbs US tariffs and how underlying inflation develops in the coming months. Thus, we expect the ECB to be deliberately uninformative in this week’s meeting.

The euro managed to eke out a small gain vs. the USD last week, but EUR/USD has been range bound for most of the past month. The 50-day sma is acting as strong support at $1.1660, and if the ECB sounds concerned about the outlook for prices, or raises their inflation forecasts for the coming year, then we could see a return to the highs from early July at $1.1830.

Daily Summary: Will the S&P 500 close the week with a loss❓Find out what drove the market today ⬇️

Three Markets to Watch Next Week: EURUSD, Gold, S&P 500 (26.06.2026)

Fed's Kashkari says AI will force a rate hike; EURUSD and USD reverse early moves ❗

University of Michigan sentiments lower than expected

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.