UnitedHealth Group shares rose by nearly 7% in premarket trading ahead of Thursday’s Wall Street session after the company posted Q2 2026 results that were significantly better than expected.

The biggest surprise was not revenue, but profitability. The market not only got the long awaited decline in medical benefit costs, but management also raised full year guidance once again.

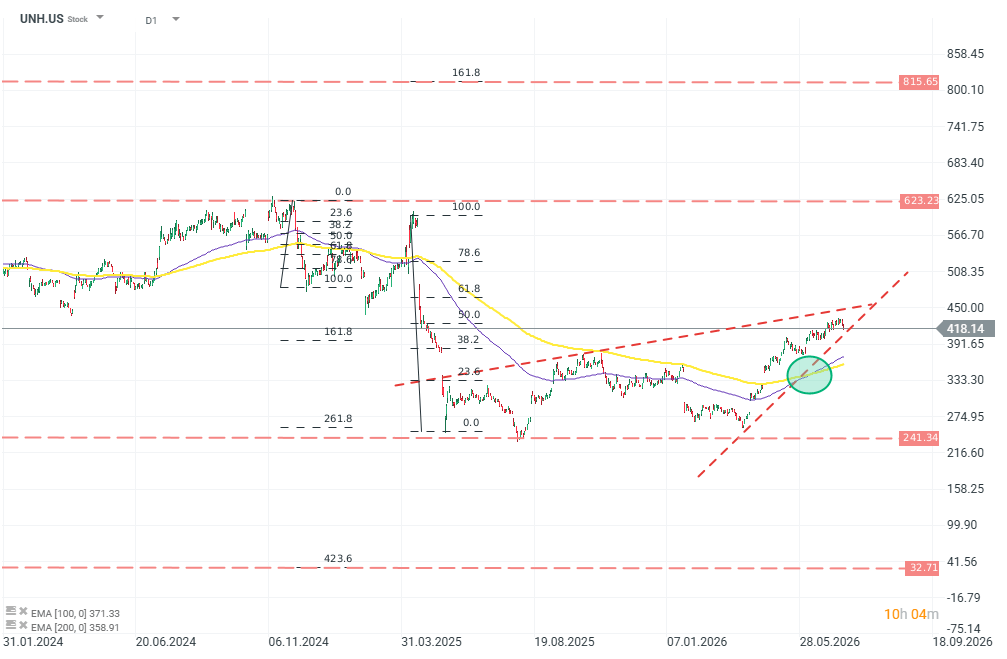

Technical analysis of UnitedHealth Group (D1)

The company’s shares remain well below late 2024 levels, but the technical picture is starting to look clearly more positive. The key shift is the generation of a “golden cross” signal (EMA100 and EMA200). Source: xStation5

Results

- Adjusted EPS came in at $6.38 versus roughly $4.90 expected by the market. Revenue reached $112 billion, slightly above $111.6 billion a year ago, and above consensus.

- Operating profit increased from $5.2 billion to $8 billion.

- Operating cash flow totaled $11.1 billion.

- The most important item in the report was the medical cost ratio (the share of premiums allocated to covering medical benefits). It fell to 86.7% from 89.4% a year earlier, while the market had expected around 88.5%.

- The UnitedHealthcare segment generated $86 billion in revenue, and operating profit rose from $2.1 billion to $3.9 billion. The operating margin increased from 2.4% to 4.6%.

- However, the improvement in profitability was achieved partly at the expense of scale: the number of customers served fell by 525,000 during the quarter.

- Optum also recorded a clear improvement. The segment generated about $4 billion in operating profit, and its margin increased by 160 basis points. Management pointed to stronger performance at Optum Insight and the use of AI tools.

- At the same time, management acknowledged that a full return to Optum revenue growth remains a multi year process and is expected only in 2028.

Guidance

UnitedHealth raised its full year 2026 adjusted earnings outlook to $19.50 to $20.00 per share, versus the prior assumption of more than $18.25.

At the same time, the operating cash flow forecast was raised to around $24 billion, and the share buyback plan was doubled to at least $5 billion. The revenue forecast, however, was left unchanged at more than $439 billion.

Outlook

The earnings call delivered plenty of positive information, but the company’s situation has not become unambiguously good. UnitedHealth’s profitability recovery is progressing faster than the market had assumed.

- Revenue remains nearly flat, and the customer base is shrinking.

- However, the company is effectively cutting back its least profitable contracts and regaining control over costs.

Daily Summary 🗽 Wall Street Holds Firm Despite Weakness in Memory Stocks, Rising Oil Price

Moderna shares slide despite mFlusiva success 📉 What's next for the mRNA vaccines market giant?

Stock of the Week: Arista Networks—A Second-Tier Technology with Top-Tier Results

US Open: S&P 500 shows strength as semiconductor lags 🚩 Western Digital down 12%

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.