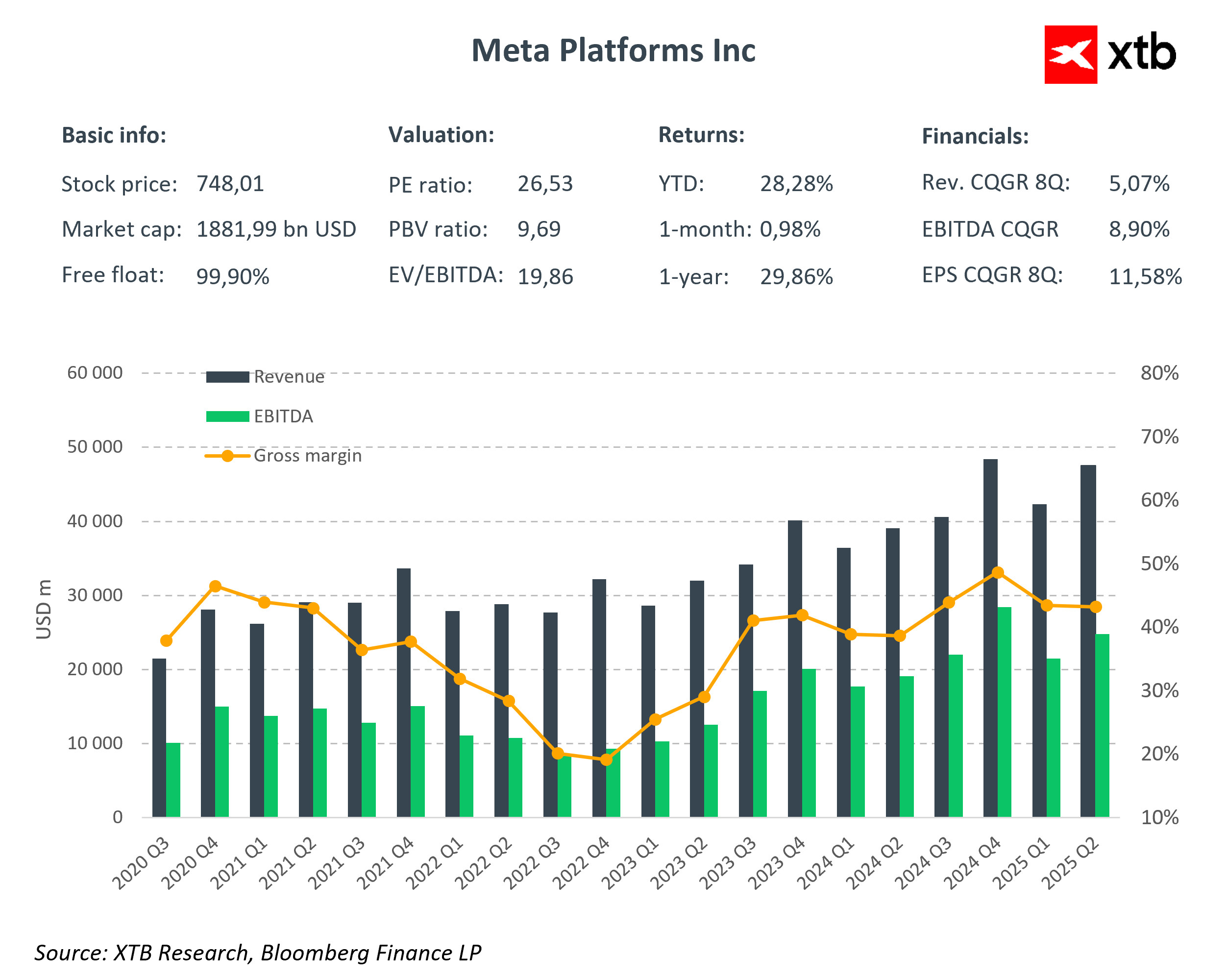

Meta Platforms (META.US) will publish its Q3 FY2025 earnings report today. The stock has seen a solid two-week rally of over 6%, though it is trading flat today. Year to date, Meta shares are up 27.41%, and since the early-April lows, they have surged 54.80%.

The company’s advertising business remains the key growth driver. The market expects double-digit increases in both volume and revenue. FactSet and Bloomberg consensus forecasts point to $49.5 billion in quarterly revenue. Investors will also be paying close attention to capital expenditures (capex). Meta traditionally provides updated capex guidance in Q3, and this time, the market expects a ~40% jump in spending next year, driven by heavy investments in data centers and AI infrastructure.

Key financial expectations

- Revenue (Q3): $49.5B, +22% y/y – the fastest growth rate this year.

- EPS: $6.72, +11% y/y.

- Ad impressions: +10.8%; average ad price: +10.5%.

- Operating margin: estimated at 39%.

- Capex 2025: around $69B, with potential guidance of $97–103B for 2026.

- Daily active users across Meta’s ecosystem: 3.48 billion.

AI investments under scrutiny

Meta’s ongoing transformation toward artificial intelligence is having an increasing impact on its balance sheet. This year’s capex of around $70 billion, combined with private financing of $27–30 billion from Blue Owl Capital and PIMCO, highlights the scale of the company’s ambitions. The funds will support the expansion of Hyperion data centers and long-term AI development projects. Unlike Microsoft or Amazon, Meta is building computing capacity solely for its own ecosystem, making these investments strategic but also riskier in the event of a slowdown in advertising revenue growth.

What the market is watching

Investors currently accept the rising capital expenditures, viewing them as justified by the potential benefits of greater user engagement and ad efficiency. However, the 2026 guidance could test that optimism. Analysts expect around $72 billion in capex for 2025, and possibly over $100 billion for 2026.

Outlook

Meta’s results are likely to confirm strong cash flow driven by advertising, but the balance between aggressive AI investment and profit growth will determine the market’s reaction. If the company signals excessive 2026 spending or shows signs of advertising slowdown, shares could correct after recent gains. Conversely, progress in AI initiatives or higher user engagement could strengthen Meta’s market position and justify its elevated valuation.

Stock of the Week: TSMC – The Manufacturing Engine Behind the AI Revolution

US Open: Alphabet and Tesla Weigh on Wall Street, While Oil Prices Renew Investor Concerns

Texas Instruments earnings: Growth without cash

Lockheed Martin and RTX raise guidance 🚀 Defense stocks move higher

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.