US CPI surprised on the downside for June, with headline CPI falling 0.4% last month, and the annual rate moderating to 3.5% from 4.2% in May. The core rate of price growth also moderated to 2.6% from 2.9% in May, which is adding to market confidence that price pressures in the world’s largest economy could be temporary.

Fed rate hike expectations put to bed

This was the largest moderation in US price growth for 6 years and it drastically reduces the chance of a rate cut at this month’s FOMC meeting. There is now a 15% chance of a rate hike from the Fed on the 31st July, compared to a 40% chance before the CPI reading. Fed Governor, Chris Waller, said on Monday that if the inflation print was hotter than expected, then he would vote for a rate hike. However, this downside surprise suggests that Waller and others at the Fed may prefer to extend the pause on rates rather than rush into hikes when core inflation is slowing.

CPI: the detail and what could come next

Digging deeper into the detail, the index for energy prices dropped by 5.7% after oil prices fell sharply last month, and the energy index was, unsurprisingly, the largest contributor to the monthly all items decrease in the CPI index last month.

Outside of energy, there were also some encouraging signs that service sector inflation has passed its peak in the US. Indices that decreased last month included car insurance, communication, clothing, medical care and used cars and trucks. Shelter and housing costs rose at their slowest pace for 2026 so far, rising 0.1% last month, and services less energy, which includes shelter, transport and medical care, was flat.

It is not only energy prices that declined last month, super core inflation, which is closely followed by the Fed, was also stable, which could give the Fed confidence that rates do not need to rise to stem inflation in the coming weeks. The Fed is laser focused on inflation under the chairmanship of Kevin Warsh, and the CPI report is now critical data each month. Today’s report suggests that the Fed will use this as evidence to justify a wait-and-see approach at their next meeting.

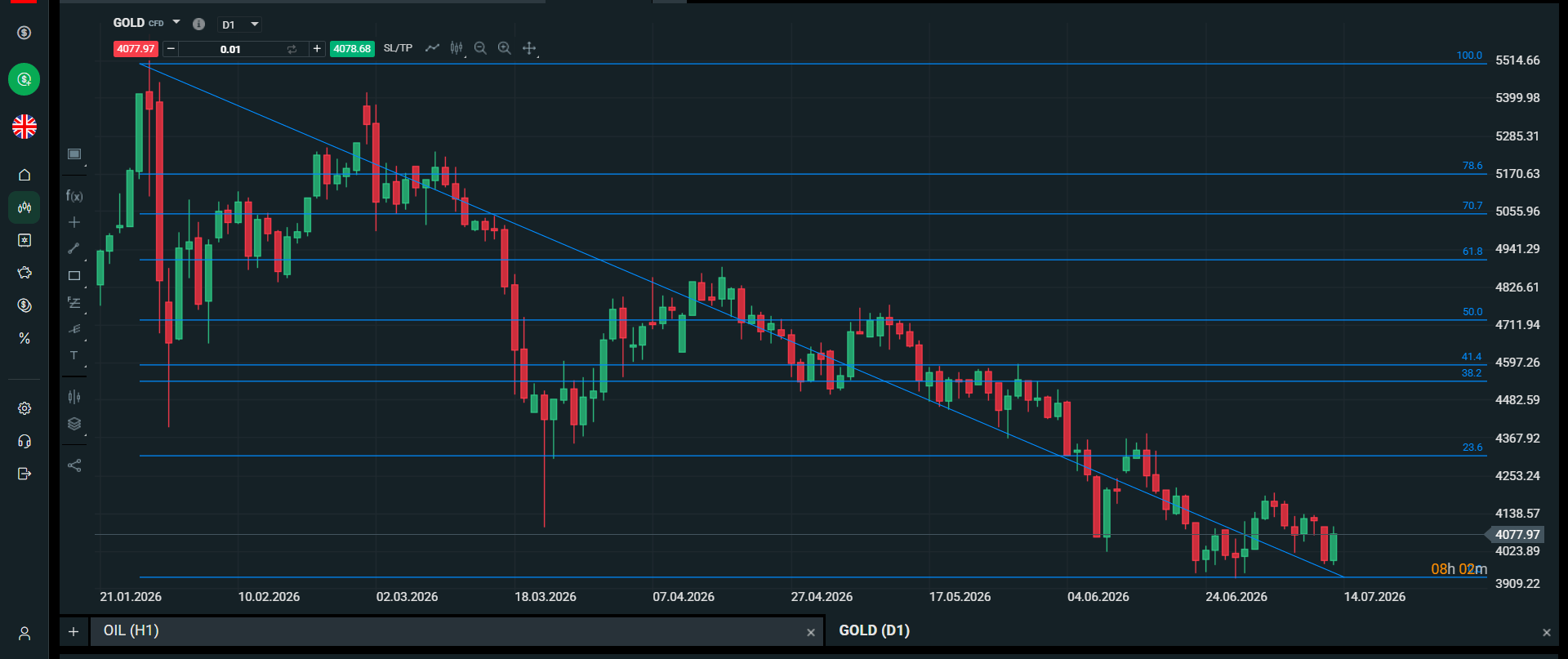

The gold price recovery continues, but for how long?

The market reaction has been immediate. The gold price rallied strongly and rose nearly 2% in the aftermath of this report. This has pushed the price back above $4,080 per ounce, but due to the severity of its losses so far this year, it is still far from key resistance levels, as you can see in the chart below. If it can break above $4350, this would suggest a mild upward bias, however, for now the longer-term downtrend remains in place, even if there is some short term movement higher.

All US stock futures are in the green on Tuesday and are rising as we start the US trading session. Chip stocks are making a comeback, and SanDisk is higher by 6% so far this morning, reversing most of Monday’s 12% losses. IBM is a major decliner, after it reported weak sales due to the clients scaling back purchases of AI hardware and directing more money towards memory chips. This is bad for IBM, and it said that its profit levels would take a hit for Q2; the stock price is lower by more than 23% today, which is limiting some of the upside for the S&P 500. However, it is great news for memory chip makers like SanDisk as it suggests that demand remains robust.

Bond market recalibration

Global bond yields have reversed course on the back of the US CPI report. UK 10-year yields are now down 1 bp, and are back below 5%. US Treasury yields are falling sharply, the 2-year yield, which is most sensitive to interest rate expectations, has dropped nearly 10bps so far today, and the 10-year yield is lower by 5bp, as the US yield curve steepens.

Will this shift the Fed’s approach?

The CPI report has made the macro backdrop more comfortable for risky assets, hence the large reaction to this report. However, the question now is, how long can moderation in inflation last? The surprise moderation in core price growth suggests that subdued inflation is not just an energy story. We will be looking closely at the incoming US economic data over the next few weeks to see if it signals any weakness in demand. So far, US economic data has remained solid, even though payrolls were weak for June. The question now is, does the Fed need to focus on demand, and take a more balanced approach towards inflation risks?

The latest flare up in Middle East tensions and the 10% increase in the oil price in July will keep inflation risks on the horizon, however, it could also weigh on consumer sentiment. Although US consumer sentiment picked up in June on the back of falling oil prices, the University of Michigan consumer sentiment index is still at depressed levels.

Overall, the regime shift at the Fed may not be as hawkish as some feared on the back of today’s CPI report. Will this be enough to placate a market that is jittery due to geopolitical risks? We shall have to see, but the sharp decline in bond yields in the past hour, combined with a pickup in the gold price and a recovery in equities suggests that the Fed, along with tensions in the Middle East, are both key drivers of financial markets this week.

Chart 1: The gold price bounces back after the weaker than expected US CPI report

Source: XTB

Stock of the Week: Arista Networks—A Second-Tier Technology with Top-Tier Results

📉 Natural gas tumbles as US EIA inventories rise

Oil climbs back above $80 per barrel 🔼

US Open: S&P 500 shows strength as semiconductor lags 🚩 Western Digital down 12%

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.