The US stock market returns to trading after the end of the long weekend. The session open is not bringing clear moves in the main indices. US100 futures are up by around 0.2% and are slightly below the 30,000 level.

On Monday, the market lacks major impulses from corporate news, but it is still closely watching semiconductor companies, which fell noticeably last week. Macro data releases related to the non-manufacturing sector are in focus.

Company news:

- Broadcom (AVGO.US): One of the leaders in the semiconductor sector is posting strong gains at the start of the US session, improving sentiment in the sector. Shares are up about 5%. The move is driven by news of expanded cooperation between the company and Apple. The partnership is intended to run through 2031 and includes the development of new ASIC chips for Apple.

- TeraWulf (WULF.US): The Bitcoin mining company has signed a long-term lease agreement for one of its sites with Anthropic. The stock is up more than 15%.

- Seer (SEER.US): The protein research company is up more than 30% after the CEO proposed taking the company private at a clear premium to the market price.

- MicroStrategy (MSTR.US): The company’s valuation is down about 1.5% after news emerged of additional tranches of Bitcoin sales to pay dividends to investors. The company also reports unrealized losses of USD 8.32 billion on digital assets. Bitcoin falls on the news, dropping below USD 62,000.

- Zim Integrated (ZIM.US): The share price is down more than 6% after Israel’s prime minister commented on a long-rumored potential sale of the company, stating that it is not planned.

- DataDog (DDOG.US): The company received an updated recommendation from Bernstein, after which it is down more than 4%.

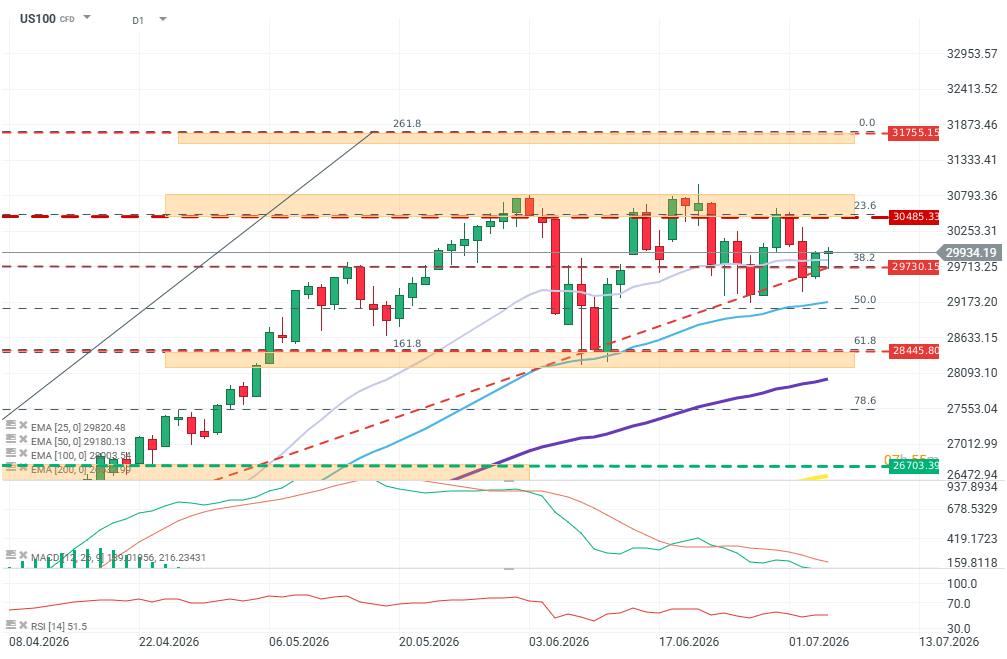

Technical analysis of US100 (D1)

Price is oscillating around resistance at the 38.2 Fibonacci level, but supply is clearly entering the resistance zone. The correction remains shallow, and the RSI has normalized in the meantime. The momentum of the EMA averages also remains clearly bullish. If sellers keep the initiative, the next target level would be the 61.8 Fibonacci level, around 28,445 points. Source: xStation

Macroeconomic data:

- The services PMI came in slightly below expectations (51.2 vs 51.4), but it still represents an increase from the previous reading of 50.7.

- The ISM non-manufacturing index came in at 54, slightly below market expectations (54.2). The prices subcomponent was above expectations, pointing to higher-than-forecast price growth (67.7 vs 67.5). These readings may be treated with more attention than before due to K. Warsh’s departure from the “forward guidance” policy. The same applies to today’s conference by FOMC’s Christopher Waller.

When will the rise in oil prices reach us?

Daily Summary: Equities Diverge as Tech Lags, Europe Rallies on Earnings & PMIs (24.07.2026)

Three markets to watch next week (24.07.2026)

Oil Slides Ahead of the Weekend!

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.