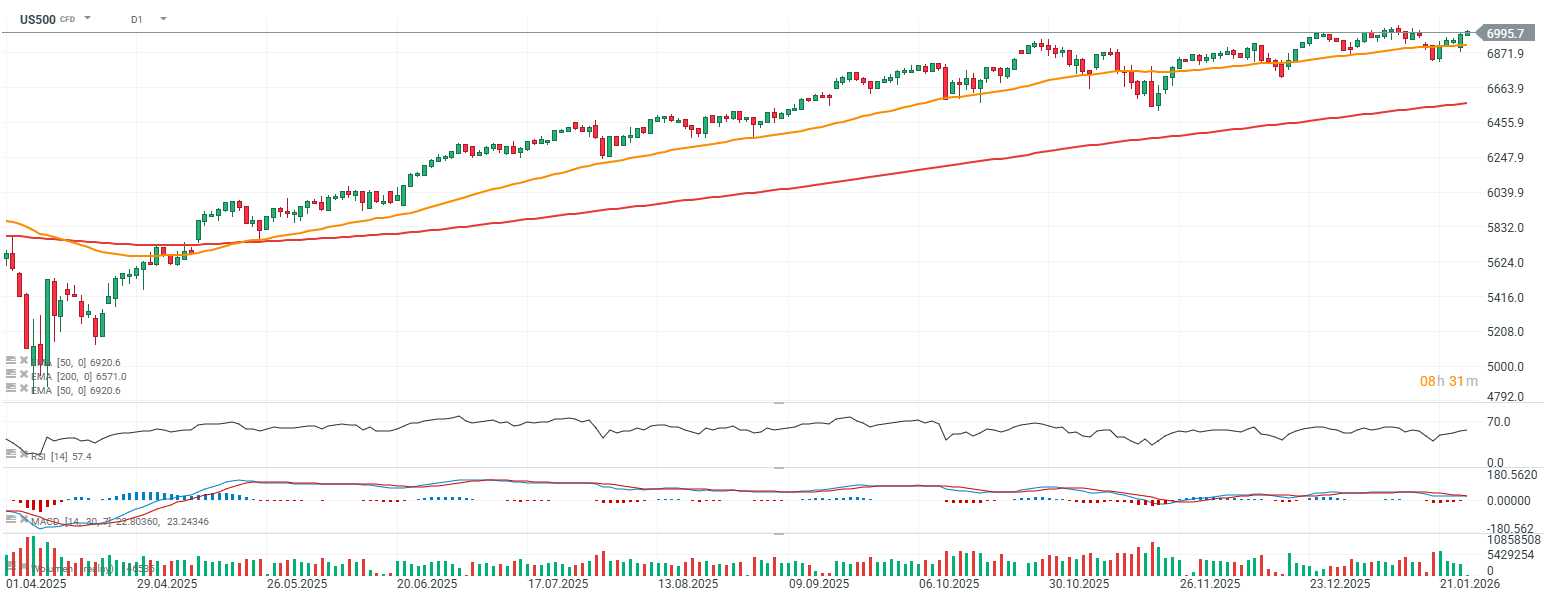

The US stock market is posting gains at the start of Tuesday’s session, with investors gradually positioning ahead of tomorrow’s Fed decision and Jerome Powell’s press conference. That event risk is likely to trigger some reshuffling in index and dollar positioning. On the macro side, today’s key release is the Conference Board index, which will offer a fresh read on US consumer sentiment. This morning’s US housing data surprised to the upside: home prices rose 0.6% m/m versus 0.3% expected and 0.4% previously, while prices across the 20 largest US metro areas increased 1.4% y/y versus 1.2% expected and 1.3% previously. In addition, the weekly ADP employment change came in at 7.5k jobs versus 8k previously. US500 is pushing toward the 7,000 level, an area that triggered two downside impulses in December.

Source: xStation5

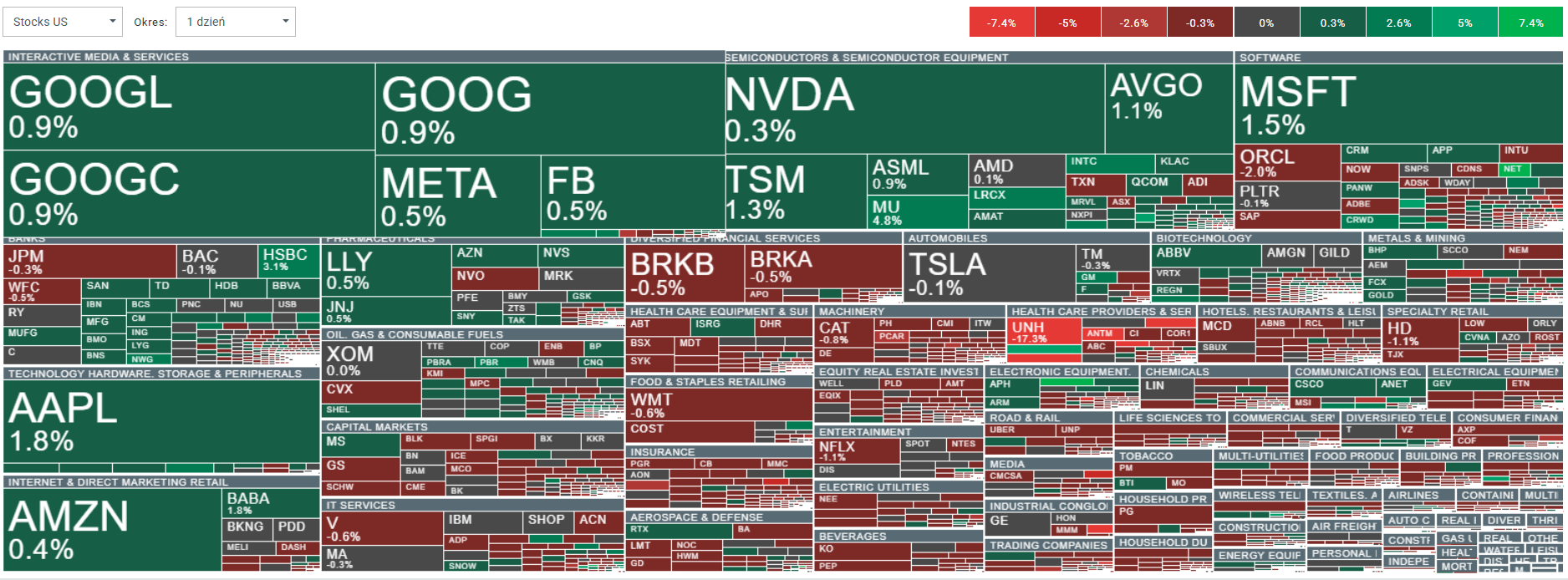

UnitedHealth shares are down more than 17%, but broader market sentiment is being supported by strength in Big Tech. Apple, Amazon, Alphabet, Meta Platforms, and Nvidia are higher, alongside semiconductor supply-chain names from Micron and Lam Research to cybersecurity player Cloudflare.

Source: xStation5

US stock market news

- US equities are showing clear sector selectivity today, with healthcare as the main source of pressure. Health insurers are sliding after the US proposed holding payments to private Medicare plans flat next year. Investors had expected mid-single-digit increases, so the market reaction has been sharp. Humana (HUM.US) is down around 15%, UnitedHealth (UNH.US) is off 17%, and CVS Health (CVS.US) is lower by 13%. Adding to the negative tone, UnitedHealth said it expects revenue to decline in 2026, which would mark its first annual contraction in more than three decades.

- In hospitality software, Agilysys (AGYS.US) is down 12% after posting fiscal third-quarter adjusted EPS that missed expectations, a typical repricing when results fail to justify valuation. Airlines are mixed: American Airlines (AAL.US) is up about 3% after fourth-quarter results, while JetBlue (JBLU.US) is down 3% after reporting a wider-than-expected loss, underlining the challenges of moving upmarket.

- In AI and cloud infrastructure, CoreWeave (CRWV.US) is up 4%, extending Monday’s rally after Nvidia invested an additional $2 billion in the company. Following the news, Deutsche Bank upgraded the stock to Buy, supporting sentiment across the AI infrastructure space.

- Sanmina (SANM.US) is among the notable laggards, down 8% after a second-quarter revenue outlook below consensus. In logistics, United Parcel Service (UPS.US) is up 3% after forecasting full-year sales above Wall Street expectations, while continuing its plan to remove less profitable package volume from its network.

- In autos, General Motors (GM.US) is up roughly 4% after guiding for profit growth of up to $2 billion this year and signaling a higher dividend and buybacks. In defense, Northrop Grumman (NOC.US) is down 1% after issuing a full-year adjusted EPS outlook below consensus, while small, space sector company Redwire (RDW.US) is up 15% after winning a contract tied to a US missile defense program. The biggest, US defense contractor, RTX Corp. (RTX.US; formerly known as Raytheon Corp) is gaining about 3% after beating expectations on fourth-quarter adjusted EPS.

Source: xStation5

Daily Summary: Wall Street Regains Ground; Another Intervention in the Yen Market❓

Three Markets to Watch Next Week (July 31, 2026)

What July can tell us about where stocks go next

Market Wrap: European equities at 3-week highs! Apple dips in US premarket!

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.