Wall Street started the week on a positive note, although investor sentiment remains far from euphoric. Following the long weekend, market attention is focused primarily on developments in the Middle East. The situation surrounding Iran and the Persian Gulf remains highly uncertain, with recent days bringing renewed tensions and exchanges of threats between the parties involved. At the same time, signs of progress in diplomatic negotiations have helped sustain hopes for de-escalation, encouraging investors to cautiously return to risk assets.

Despite elevated geopolitical risks, major U.S. equity indices are posting modest gains. Markets appear to be increasingly pricing out the worst-case scenario for the Middle East conflict. While the tensions have already disrupted global trade flows and commodity transportation, investors are now shifting their focus toward the prospect of a gradual normalization of conditions. Expectations of de-escalation and the eventual restoration of smooth transit through the Strait of Hormuz are supporting sentiment, although market participants recognize that repairing disrupted supply chains and reversing the economic impact of recent events will take time.

Investor confidence has also been supported by reports of progress in negotiations between Washington and Tehran. U.S. Vice President J.D. Vance described the latest round of talks as having achieved "significant progress," a development that markets interpreted as increasing the likelihood of further de-escalation across the region. While the situation remains fluid, investors are increasingly focused on the possibility of a lasting agreement rather than scenarios involving a broader regional conflict.

The economic calendar remains relatively light at the start of the week, prompting investors to look ahead to several key events scheduled for the coming days. Thursday’s release of the PCE inflation report, the Federal Reserve’s preferred inflation gauge, will be closely watched for clues regarding the future path of U.S. interest rates. With Fed officials recently signaling a cautious approach toward further monetary easing, any indication of persistent inflationary pressures could have a meaningful impact on market expectations.

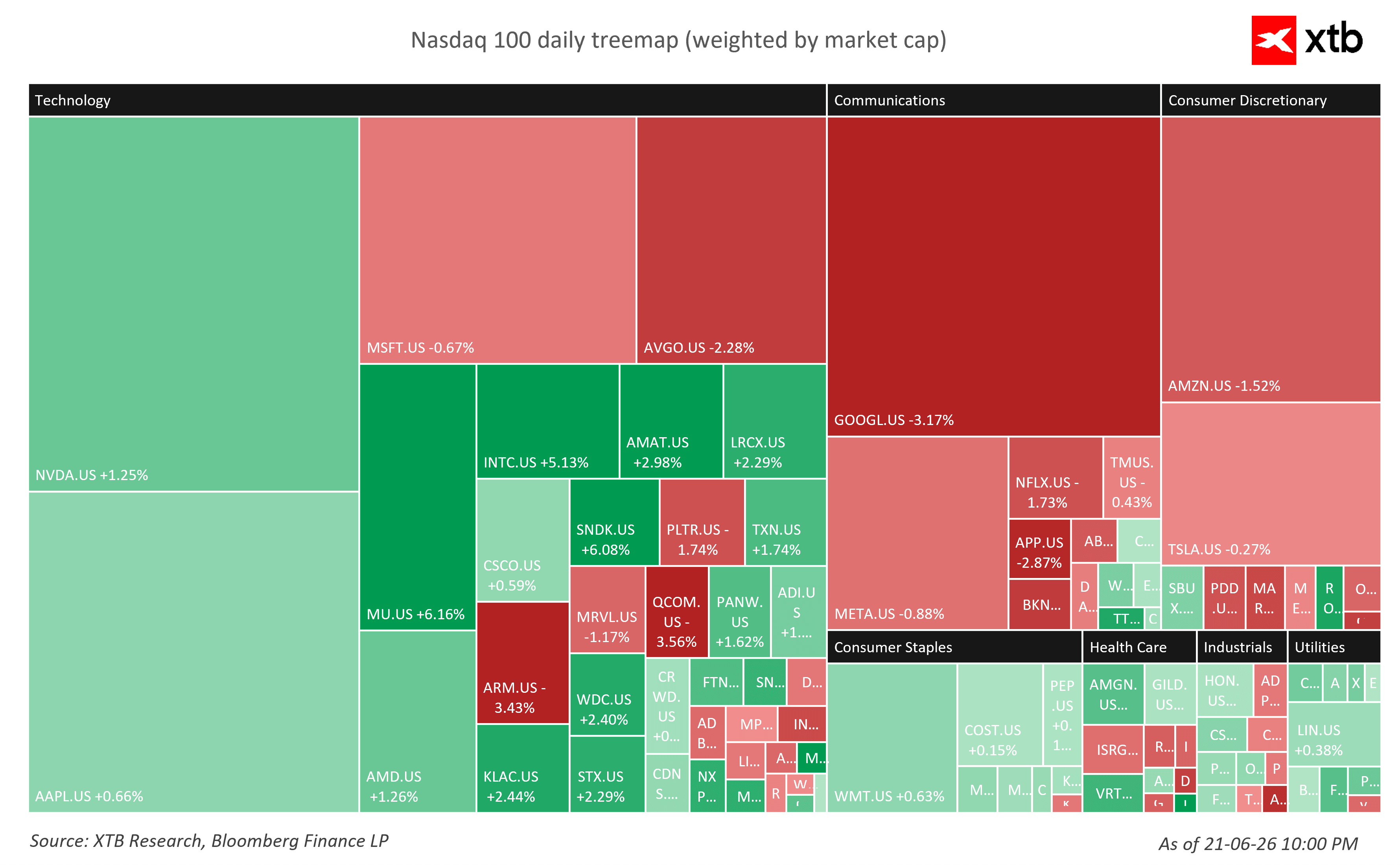

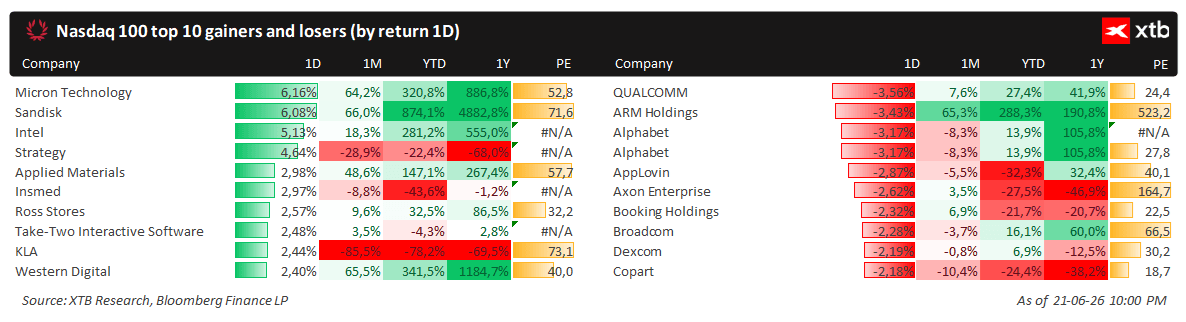

Micron’s upcoming quarterly earnings report is also drawing considerable attention and may prove to be one of the most important events of the week for the semiconductor sector. Investors are looking for confirmation that strong demand tied to artificial intelligence infrastructure, data centers, and advanced memory solutions remains intact. Solid results could provide another catalyst for the technology sector, which has been one of the market’s strongest performers in recent months.

For now, investors are opting for cautious optimism, betting on further geopolitical de-escalation while maintaining confidence in the resilience of corporate earnings. The start of the week suggests that markets remain focused on a gradual normalization of conditions in the Middle East, although a more meaningful test of sentiment may arrive later this week with key macroeconomic releases and corporate earnings.

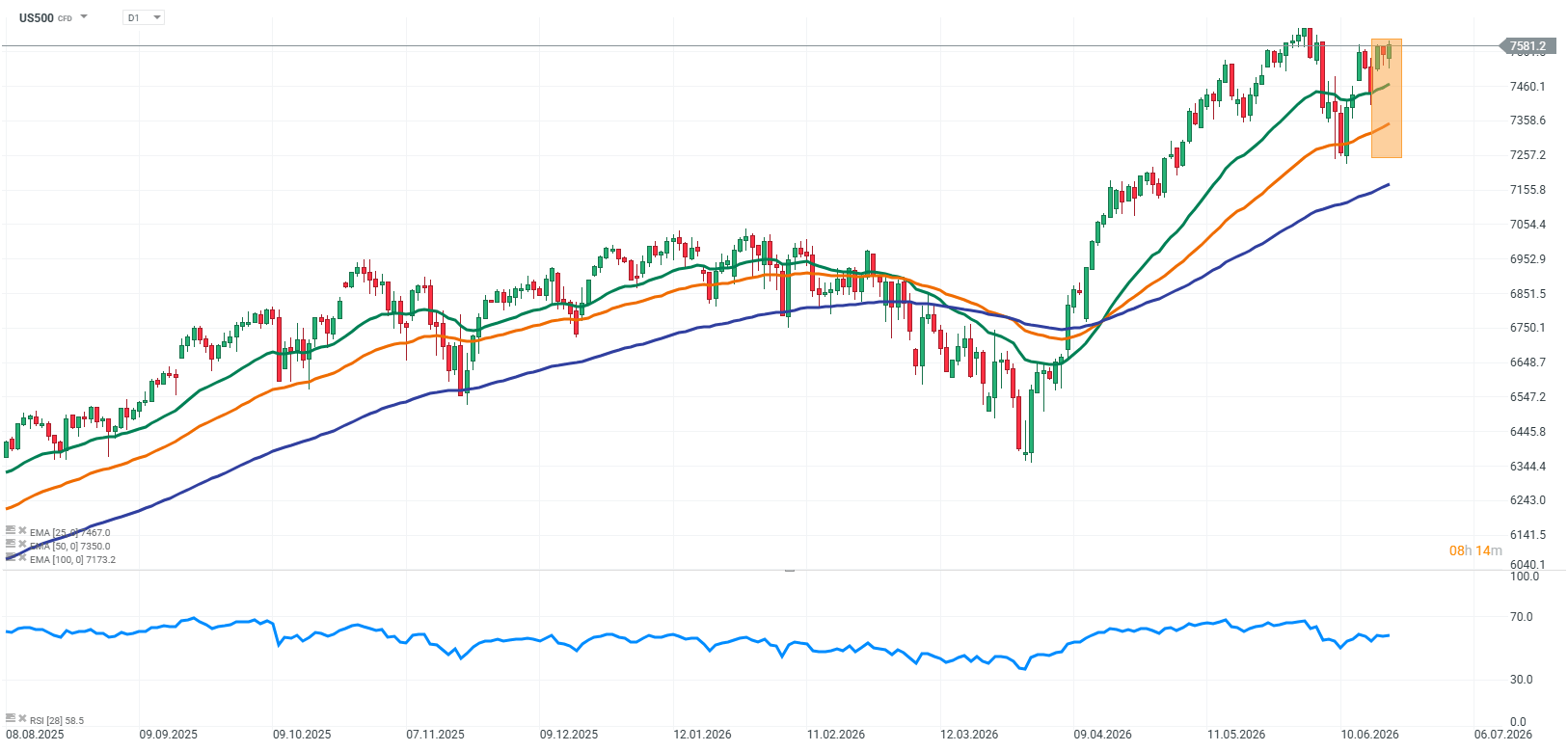

S&P 500 (US500) futures are moving higher as investors increasingly embrace the prospect of a lasting de-escalation in the Middle East. Reports of progress in U.S.-Iran negotiations and growing expectations that a formal agreement could be reached are supporting global risk appetite. Markets are betting that a potential truce would pave the way for a gradual normalization of conditions across the region, including the restoration of unrestricted shipping through the Strait of Hormuz, one of the world's most important energy trade routes.

Source: xStation5

Company News

Micron (MU.US) is gaining ahead of its quarterly earnings release, which is expected to be one of the key events this week for the semiconductor industry. Investors are looking for further evidence of improving conditions in the memory market, where strong demand continues to outpace supply growth. The ongoing expansion of artificial intelligence infrastructure remains an important tailwind, driving demand for advanced memory solutions used in data centers. The results could serve as a key indicator of the broader health of the AI ecosystem.

SpaceX (SPCX.US) shares remain under pressure following the announcement of the company’s inaugural corporate bond offering. The move comes after a strong post-IPO rally and is being viewed by some investors as an opportunity to lock in profits. At the same time, the additional capital could support future expansion initiatives and strategic investments, which remain central to the company’s long-term growth plans.

Super Micro Computer (SMCI.US) is trading higher as investors adopt a more constructive view of the company’s outlook. Concerns surrounding shareholder dilution appear to be fading, while attention shifts back toward strong demand for AI-focused server infrastructure. Expectations for continued growth in orders related to high-performance computing and artificial intelligence remain a key driver of sentiment toward the stock.

Cerebras Systems (CBRS.US) remains in focus ahead of its upcoming earnings release. Investors are closely watching the company’s ability to execute on its growth strategy and maintain strong business momentum. Confidence in the company’s outlook has been supported by major strategic partnerships announced in recent months, helping to alleviate concerns about future demand for its AI computing solutions.

Daily Summary: Wall Street Regains Ground; Another Intervention in the Yen Market❓

Three Markets to Watch Next Week (July 31, 2026)

What July can tell us about where stocks go next

Market Wrap: European equities at 3-week highs! Apple dips in US premarket!

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.