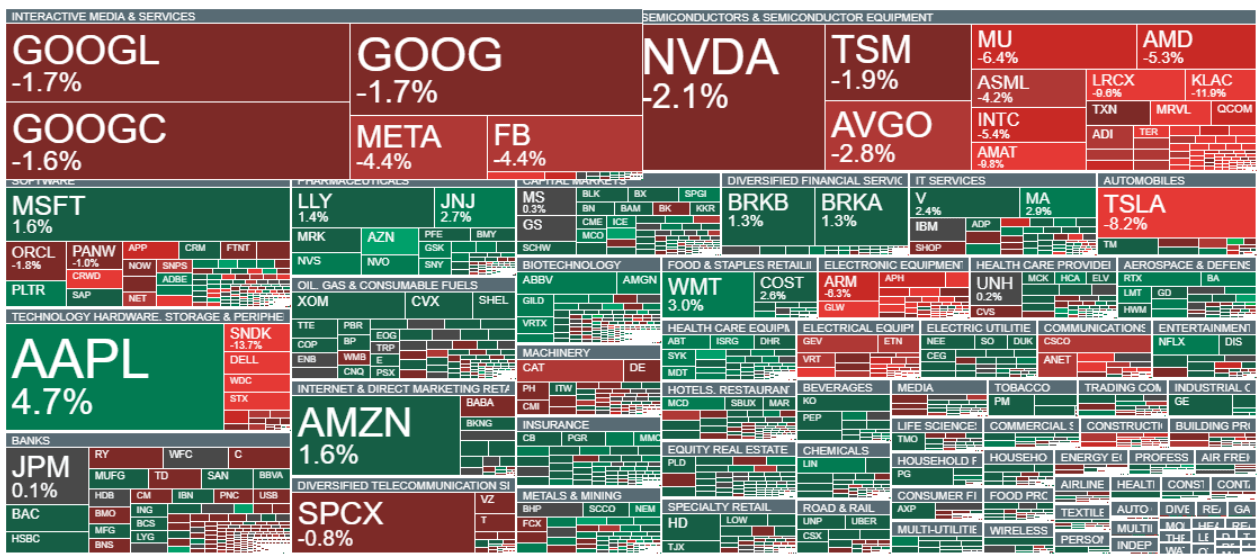

- Semiconductor stocks are under heavy selling pressure, with SanDisk plunging more than 13%.

- Nasdaq 100 (US100) futures have fallen by nearly 700 points in less than an hour, extending losses to almost 2%.

- The S&P 500 is down 0.4%, while the Dow Jones Industrial Average gains more than 0.6%, highlighting deteriorating market breadth as "old economy" stocks increasingly outperform the technology sector.

- Pharmaceutical, entertainment, defense, and oil & gas companies are significantly outperforming the broader market amid the technology sell-off.

- Semiconductor stocks are under heavy selling pressure, with SanDisk plunging more than 13%.

- Nasdaq 100 (US100) futures have fallen by nearly 700 points in less than an hour, extending losses to almost 2%.

- The S&P 500 is down 0.4%, while the Dow Jones Industrial Average gains more than 0.6%, highlighting deteriorating market breadth as "old economy" stocks increasingly outperform the technology sector.

- Pharmaceutical, entertainment, defense, and oil & gas companies are significantly outperforming the broader market amid the technology sell-off.

Technology stocks came under heavy selling pressure during Thursday's afternoon session, with semiconductor companies leading the decline. Nvidia and TSMC are down nearly 2%, while Sandisk and Micron have fallen approximately 13% and 6.5%, respectively. Tesla has also dropped more than 8%, as a nearly 25% year-over-year increase in vehicle deliveries failed to sustain bullish sentiment. Meanwhile, Nasdaq 100 futures have unexpectedly fallen by more than 700 points to around 29,500, while some semiconductor names have suffered even steeper losses. Applied Materials (AMAT), for example, has declined by more than 20% since June 29.

- Meta Platforms is down nearly 4.5%, while weakness extends across much of the electronic component supply chain, from Dell to Arm Holdings. On the other hand, Apple is outperforming, gaining nearly 5%, alongside Microsoft, while pharmaceutical, healthcare, IT services, and defense stocks such as Lockheed Martin and RTX Corp. are trading higher.

- Despite today's sell-off, HSBC doubled its price target on Intel to $200 from $100, reiterating its Buy rating. The bank expects stronger server CPU shipments and rising demand for Intel Foundry services, forecasting increased customer commitments from the second half of 2026 that should support earnings growth over the longer term. Nevertheless, Intel shares are down more than 5% today, trading below $120.

- Additional pressure on the semiconductor sector may have come from reports published yesterday suggesting that Apple is considering sourcing memory chips from Chinese manufacturers. Such a move could raise concerns about the long-term competitive position of U.S., South Korean, and Taiwanese memory suppliers. According to Bloomberg, Apple is in discussions with ChangXin Memory Technologies (CXMT) and Yangtze Memory Technologies (YMTC) to diversify its supply chain and ease the effects of the global memory shortage, despite both companies appearing on the Pentagon's blacklist over alleged ties to China's military sector.

- Bloomberg also reported that Apple has sought support from the Trump administration to reduce the potential political consequences of such cooperation. Expanding its supplier base would help Apple secure memory chip availability while reducing the cost pressures that have recently forced the company to raise prices across parts of its product lineup.

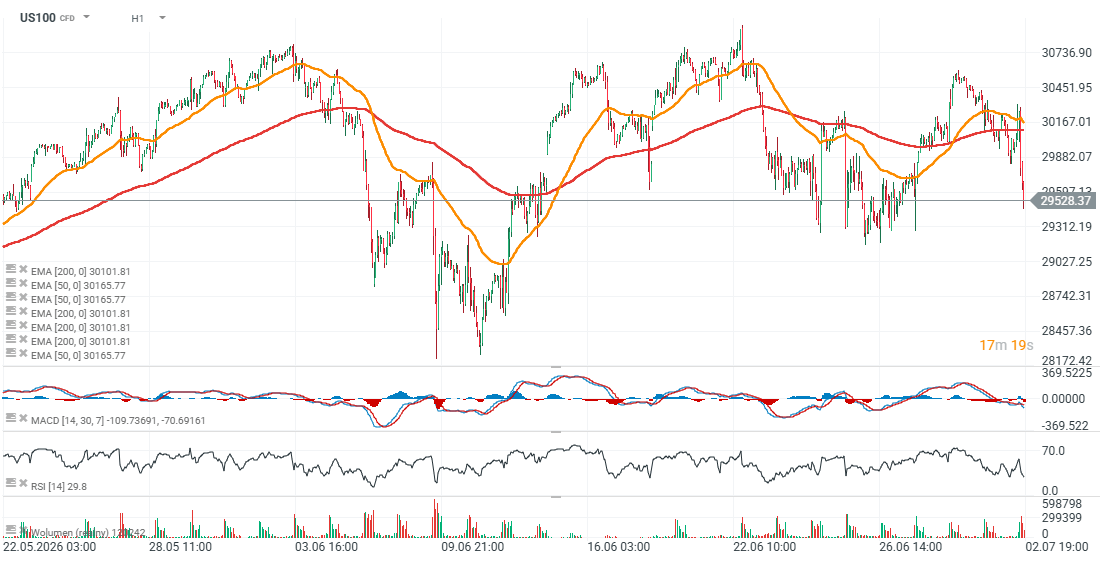

S&P 500 volatility

Source: xStation 5

On the hourly timeframe, the US100 RSI has dropped to just below 30, signaling deeply oversold conditions. The index has also failed to sustain trading above both the 50-period and 200-period EMAs, suggesting that bullish momentum has weakened considerably. It is worth noting, however, that semiconductor and memory stocks have delivered gains of several hundred percent over recent months—and, in some cases, more than 1,000% over the past year (including SanDisk and Micron)—while simultaneously reporting record growth in revenue and earnings, in some cases rising by several hundred percent year over year. As a result, the current decline may ultimately prove to be a healthy profit-taking correction rather than the beginning of a long-term bearish trend.

Source: xStation 5

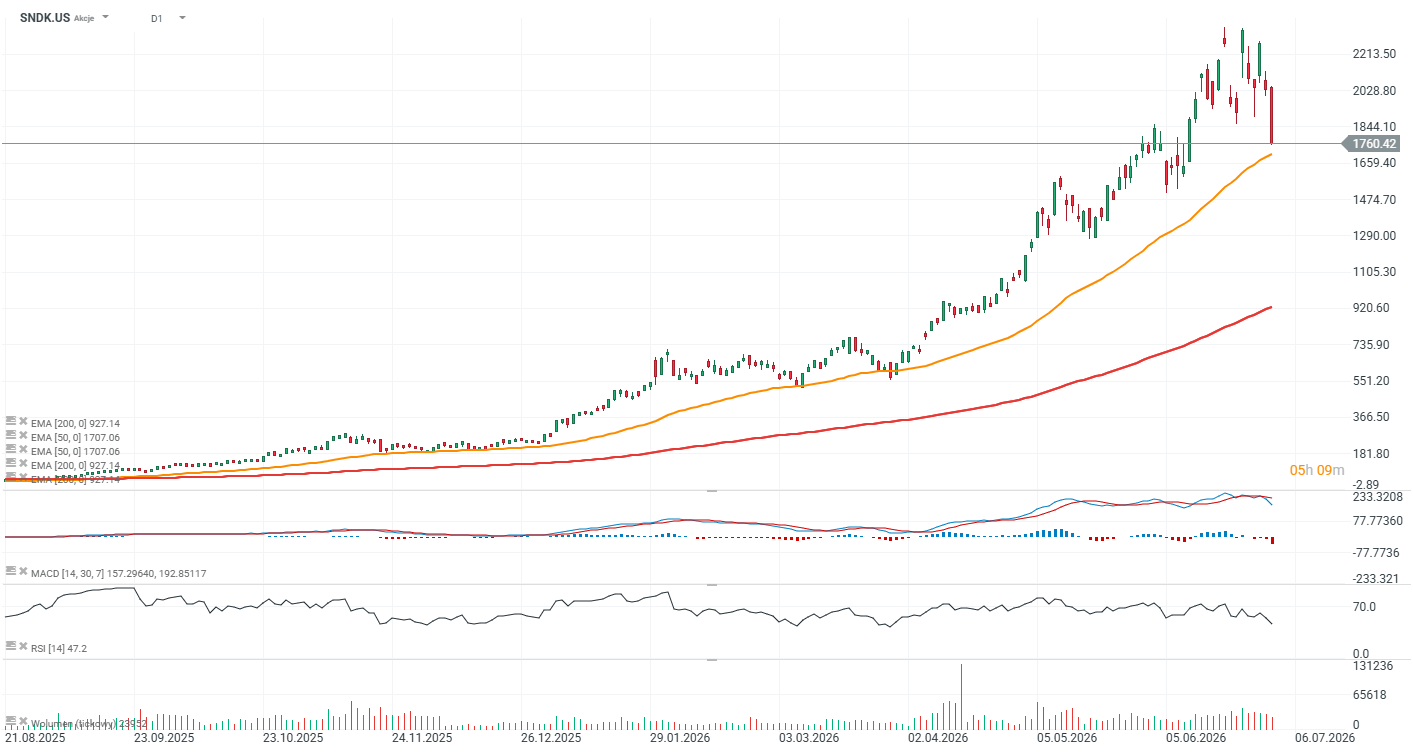

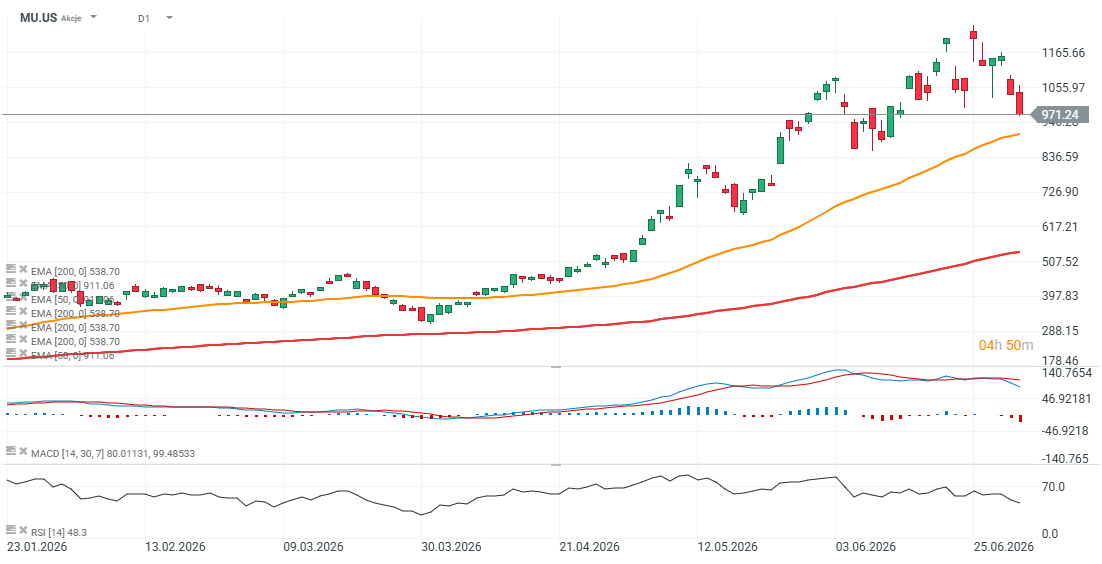

SanDisk and Micron (D1)

The Roundhill Memory ETF (DRAM), which provides exposure to the memory semiconductor industry, is down nearly 20% during the shortened trading week after an extraordinary rally that saw the ETF almost triple from its April 2 launch to its late-June peak. Over the same period, Micron has fallen almost 15%, while SanDisk has plunged more than 20% in just two trading sessions.

Source: xStation 5

One of the strongest performers in the memory sector is now experiencing a sharp reversal, with profit-taking overwhelming buying interest despite the company recently reporting record quarterly results and substantially raising its forward guidance. The stock has retreated to levels last seen on June 11.

Source: xStation 5

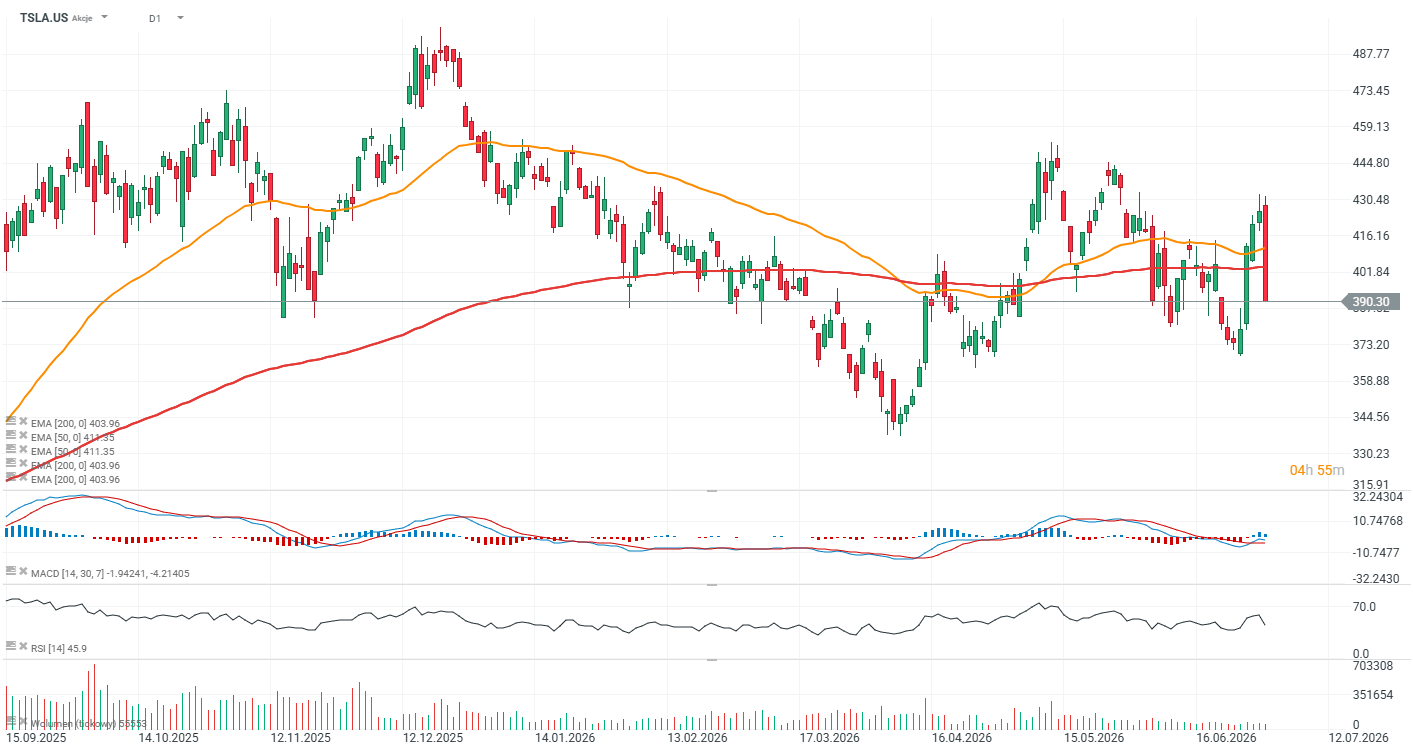

Tesla under pressure as shares fall 7%

Tesla is down more than 7% despite reporting exceptionally strong second-quarter delivery figures. The company delivered 480,126 vehicles, well above Wall Street's consensus estimate of 406,600, while production reached 451,758 units. The negative market reaction may reflect profit-taking after Tesla shares had rallied more than 13% over the previous four trading sessions. In addition, although Tesla's energy storage deployments improved to 13.5 GWh, the result fell short of William Blair's 20.6 GWh forecast.

From a technical perspective, Tesla shares have fallen below the 200-day EMA (red line). If the stock closes below $403, it could confirm a bearish trend reversal.

Source: xStation 5

Daily Summary: Wall Street Stabilizes Despite Higher Oil Prices

All or nothing: ServiceNow earnings preview

Cocoa loses 5% amid rising inventories on ICE

Oil gains 3% amid US - Iran escalation and supply disruption on the Black Sea

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.