-

The end of the Powell era and a hawkish pause: Jerome Powell's final meeting takes place under the shadow of rebounding inflation (oil above $100) and Middle East tensions, forcing the Fed to harden its rhetoric and pushing 2026 rate cut hopes further away.

-

The hopes and risks of the "Warsh effect": Kevin Warsh's nomination signals a shift toward technological optimism and a belief in the disinflationary power of AI, combined with a hawkish stance on balance sheet reduction (QT).

-

Wall Street at a crossroads: The US500 is balancing between record highs and a correction; the next move will be determined not only by the Fed’s communication but primarily by the quarterly earnings of tech giants and their tangible returns on AI investments.

-

The end of the Powell era and a hawkish pause: Jerome Powell's final meeting takes place under the shadow of rebounding inflation (oil above $100) and Middle East tensions, forcing the Fed to harden its rhetoric and pushing 2026 rate cut hopes further away.

-

The hopes and risks of the "Warsh effect": Kevin Warsh's nomination signals a shift toward technological optimism and a belief in the disinflationary power of AI, combined with a hawkish stance on balance sheet reduction (QT).

-

Wall Street at a crossroads: The US500 is balancing between record highs and a correction; the next move will be determined not only by the Fed’s communication but primarily by the quarterly earnings of tech giants and their tangible returns on AI investments.

As usual, the Fed will publish its decision at 8:00 PM CET. While no new macroeconomic projections will be released, this will be an extraordinary meeting. Firstly, it takes place at one of the most complex junctures in the history of modern central banking; secondly, it is likely Jerome Powell’s final press conference as Fed Chair.

The Federal Reserve faces the challenge of its dual monetary policy mandate: price stability and maintaining full employment. Inflation has rebounded significantly in response to the energy crisis linked to the situation in the Middle East, while the labor market remains stable, albeit clearly cooled compared to the situation one or two years ago.

All signs suggest the Fed will maintain a neutral stance amidst ongoing immense uncertainty, but simultaneously, Powell’s words may carry limited weight. Kevin Warsh may adopt a completely different approach to monetary policy and communication, though it must be remembered that decisions are made by the entire Federal Open Market Committee (FOMC), not a single individual. What should we expect from today’s decision and the near future with a new captain at the head of the Federal Reserve?

FOMC Communication and Monetary Policy Prospects Amid Mounting Risks

The macroeconomic situation at the start of the second quarter of 2026 is characterized by a high degree of divergence between hard indicators and inflation expectations. The primary dilemma for the Committee remains the fact that the disinflation process, which appeared stable in 2025, has clearly stalled. The main driver of this phenomenon is the situation in the Middle East—specifically the prolonged closure of the Strait of Hormuz and the impasse in US-Iran talks—which has propelled WTI crude oil prices above $100 per barrel.

Inflation Dynamics and the Redefinition of Risks

Inflation rebounded significantly in March, though it simultaneously came in lower than market expectations. It appears that pressure from the labor market and the broader economy is limited, and the inflationary resurgence is primarily supply-side in nature. Nevertheless, Jerome Powell himself recently indicated that elevated inflation is mainly linked to tariffs, while the impact of energy prices in March was still difficult to estimate.

An analysis of price growth components indicates a worrying trend. While core inflation (excluding energy) rose by a relatively mild 0.2% in March, the spike in energy prices threatens to de-anchor inflation expectations in the medium term. In its 2026 scenarios, the International Monetary Fund warns that in the event of a permanent disruption to oil supplies, global inflation could rise to 5.4%, while global economic growth could slow to 2.5%.

In this context, FOMC communication during the April meeting is likely to turn more hawkish. It is expected that the word "somewhat" will be removed from the statement regarding elevated inflation levels, leaving a categorical assertion that "inflation remains elevated." Such a change aims to signal to markets that the Committee is not reassured by recent data and does not plan a swift return to a cycle of rate cuts (at least until Kevin Warsh takes office in just over two weeks).

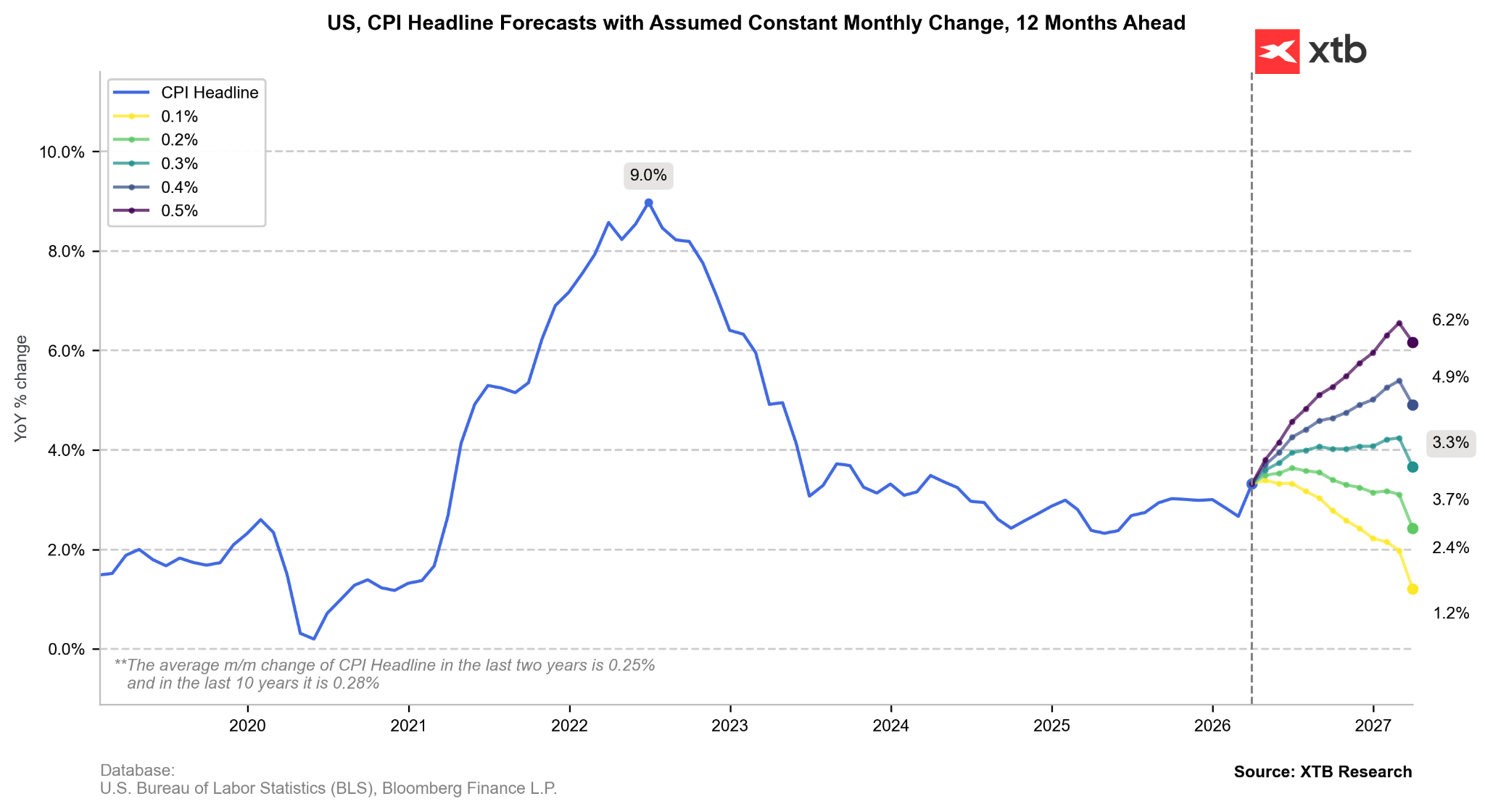

If inflation were to grow at an average of 0.3% now, we would soon breach the 4.0% level, but inflation would eventually stabilize. Conversely, an increase of just 0.2% per month would mean that inflation will soon return to a year-on-year decline. Such a scenario is possible if oil prices fall. Source: Bloomberg Finance LP, XTB

If inflation were to grow at an average of 0.3% now, we would soon breach the 4.0% level, but inflation would eventually stabilize. Conversely, an increase of just 0.2% per month would mean that inflation will soon return to a year-on-year decline. Such a scenario is possible if oil prices fall. Source: Bloomberg Finance LP, XTB

Economic Health and Labor Market Resilience

Despite price pressures, the real economy shows remarkable resilience, granting the Fed the space to maintain restrictive rates. Although consumer spending in the first quarter of 2026 shows signs of weakening, it is being effectively offset by an investment boom in the technology sector, particularly in data center infrastructure and equipment.

The labor market remains the cornerstone of the argument against rate cuts. March employment data surprised to the upside (an increase of 178,000), and the unemployment rate fell to 4.3%. Christopher Waller noted that the number of new jobs needed to stabilize unemployment is currently near zero, suggesting that the risk of a sharp deterioration in the labor market is low—though a sustained escalation in the Middle East could quickly reverse this. This diagnosis leads most FOMC members to believe that risks to the employment mandate have taken a back seat to inflationary risks.

Interest Rate Outlook: The End of 2026 Rate Cut Hopes?

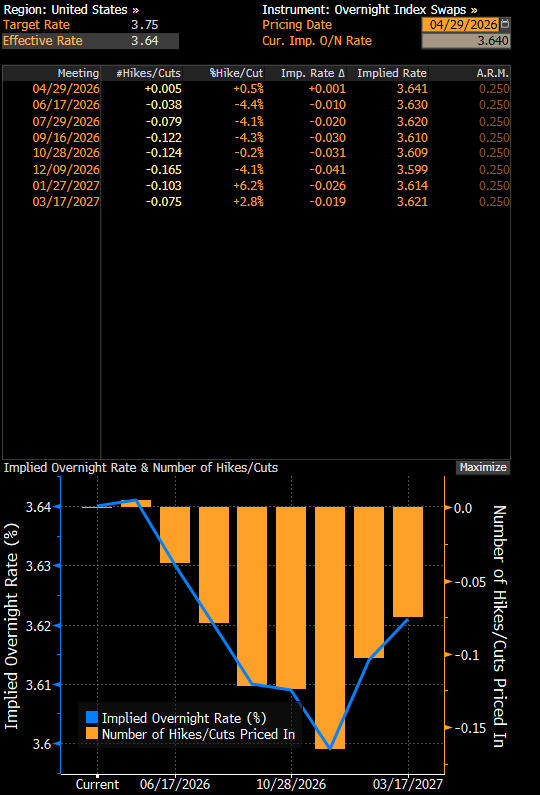

The shift in rhetoric and macroeconomic data has led to a sharp change in the market’s interest rate path. As recently as January 2026, markets were pricing the federal funds rate at approximately 3.0% by year-end; currently, Overnight Index Swaps (OIS) indicate an effective rate level of 3.6%, which essentially implies no real cuts.

Had a dot chart been published at the April meeting, it would likely have shown a median expectation of no rate changes through the end of the year, representing a hawkish shift from the March forecast of one cut. Furthermore, some Committee members, such as Lorie Logan and Beth Hammack, have begun publicly emphasizing the "two-sidedness" of risks, suggesting that if inflation continues to rise, the option of a rate hike could return to the table, even if it is not currently the base case. A significant unknown remains the policy of Kevin Warsh, who has hinted at more frequent rate movements alongside balance sheet reduction.

Expectations for interest rates suggest no movements until at least the end of 2026. Source: Bloomberg Finance LP

Expectations for interest rates suggest no movements until at least the end of 2026. Source: Bloomberg Finance LP

Summing Up Jerome Powell’s Tenure

Jerome Powell’s tenure as Chair of the Federal Reserve, which formally ends on May 15, 2026, will be remembered as one of the most turbulent periods in the central bank’s history. Powell, who took office in February 2018, moved from being perceived as a "non-economist" to the architect of radical changes in monetary strategy and a defender of institutional independence in the face of unprecedented political pressure. Key points of his chairmanship include:

- Employment Priority: Powell’s legacy is built on redefining the Fed’s mandate toward an inclusive labor market. He oversaw the longest period of unemployment below 4% since the 1950s and record-low unemployment among minorities.

- The "Transitory" Inflation Error and the Fight Against High Prices: The greatest shadow over his tenure is the delayed reaction to inflation in 2021 (labeling it transitory). However, he rectified this with the most aggressive rate-hike cycle since Paul Volcker, while avoiding a deep recession.

- Defense of Independence: Powell repeatedly resisted political pressure from the Donald Trump administration, emphasizing that decisions are made solely based on data.

- DOJ Investigation: The Department of Justice's criminal investigation into the $2.5 billion renovation costs of the Fed headquarters was closed on April 24, 2026, due to a lack of evidence of criminal activity.

- Continuing Role: Despite his term as Chair ending on May 15, Powell may remain on the Board of Governors until 2028, intended to ensure institutional stability during the transition.

The Era of Kevin Warsh

The nomination of Kevin Warsh to succeed Jerome Powell marks a fundamental shift in the philosophy of monetary policy. Warsh, a former member of the Board of Governors (2006–2011) and a figure closely linked to the tech sector, brings to the Fed a conviction that traditional inflation models must be replaced by an approach accounting for the rapid surge in productivity driven by Artificial Intelligence.

- Technological Optimism: Warsh believes that AI will trigger a sharp jump in productivity. In his view, AI is "structurally disinflationary," allowing the economy to grow faster without generating price pressure.

- A Shift in Stance (Hawk to Dove): Although he was a hawk during 2006–2011, Warsh currently presents a more dovish approach to interest rates, suggesting they may be too restrictive in the new technological reality.

- Hawkish Balance Sheet (QT): Warsh is a strong critic of Quantitative Easing (QE). As Chair, he is expected to favor further balance sheet reduction (QT), aiming for a return to the "modest reserves" model of the pre-2008 era. While this provides fuel for future responses, it may initially be viewed negatively by Wall Street.

- New Inflation Metrics: He proposes a formal shift to alternative indicators, such as trimmed mean or median inflation, to "filter out" transitory price shocks resulting from war or tariffs.

- Political Risk: Warsh’s nomination has raised concerns regarding potential compliance with the White House. However, Warsh declared "absolute independence" before the Senate, though he allows for closer coordination of Fed policy with other administrative areas (e.g., AI regulation).

Conclusions and Market Implications

The upcoming FOMC meeting in April 2026 is effectively the final act of the "Powell era," characterized by the struggle against classic supply shocks and the attempt to preserve the central bank's institutional dignity. Investors should expect communication that is mindful of mounting inflationary pressures but effectively deadlocked by the leadership transition.

Prospects under Kevin Warsh paint a picture of a Federal Reserve that will attempt to revolutionize the understanding of inflation. If the thesis regarding an AI-driven productivity jump proves correct, markets could experience a period of low interest rates alongside solid GDP growth. However, the risk of error is immense if Warsh cuts rates based on "technological hopes" while hard inflation (energy, tariffs) remains high. The United States could enter a period of deep stagflation, which would undermine confidence in the dollar as a reserve currency and simultaneously lead to a crisis in the labor market.

The key date to watch will be June 17, 2026—the first policy meeting after Warsh formally takes office. This is when we will learn if "AI optimism" translates into real easing of financial conditions, or if the hawkish reality of the balance sheet and geopolitics will force the new Chair to continue the restrictive path set by his predecessor. In the short term, the market must brace for a period of "information noise" and a potential power struggle within the Board of Governors, which may increase volatility at the long end of the yield curve.

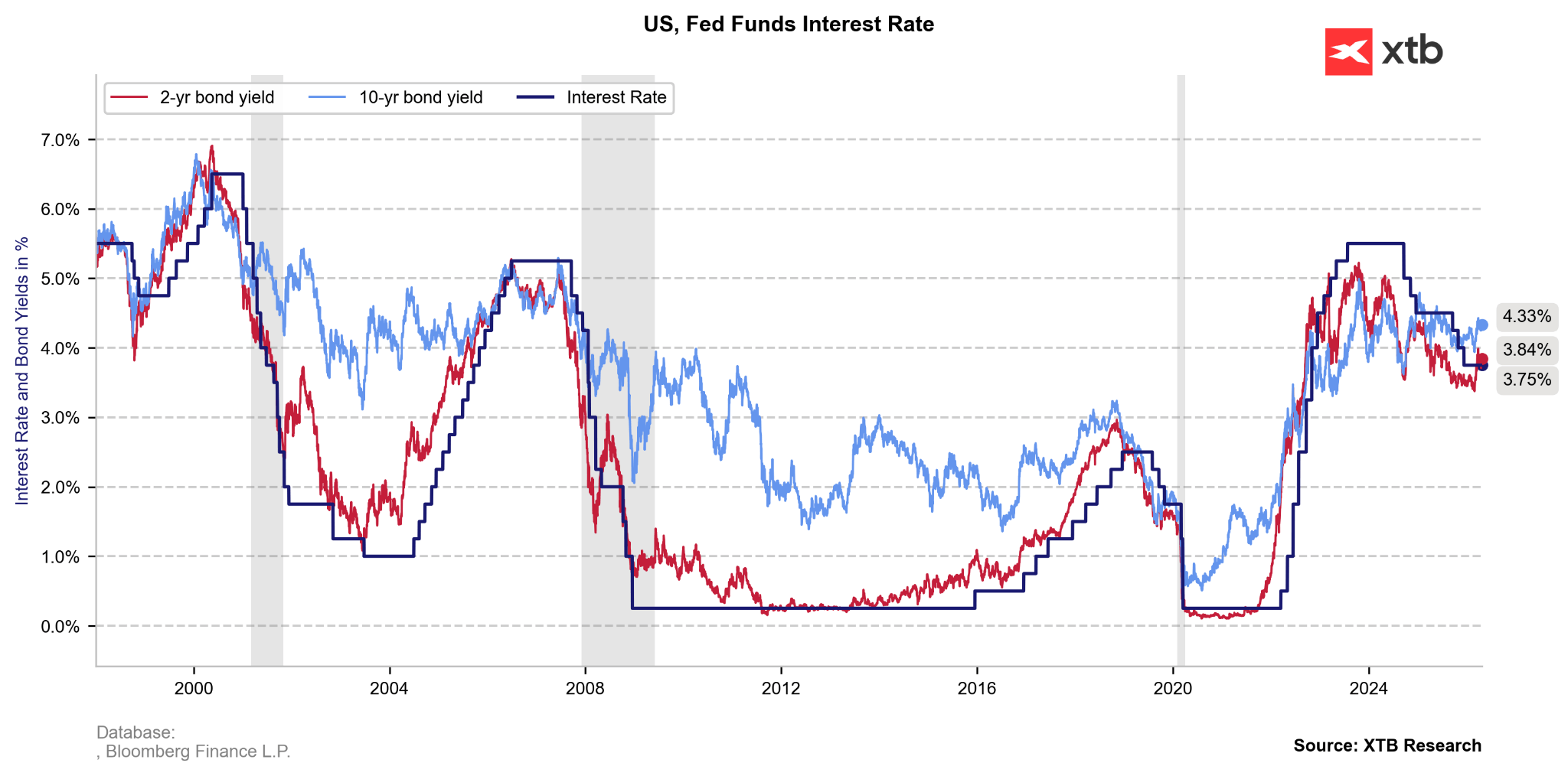

Bond yields remain elevated due to uncertainty regarding the Middle East. It is worth noting, however, that a yield premium over interest rates was historically normal. Interest rates are simply not excessively high right now, as was the case at the turn of 2023/2024. Source: Bloomberg Finance LP, XTB

Bond yields remain elevated due to uncertainty regarding the Middle East. It is worth noting, however, that a yield premium over interest rates was historically normal. Interest rates are simply not excessively high right now, as was the case at the turn of 2023/2024. Source: Bloomberg Finance LP, XTB

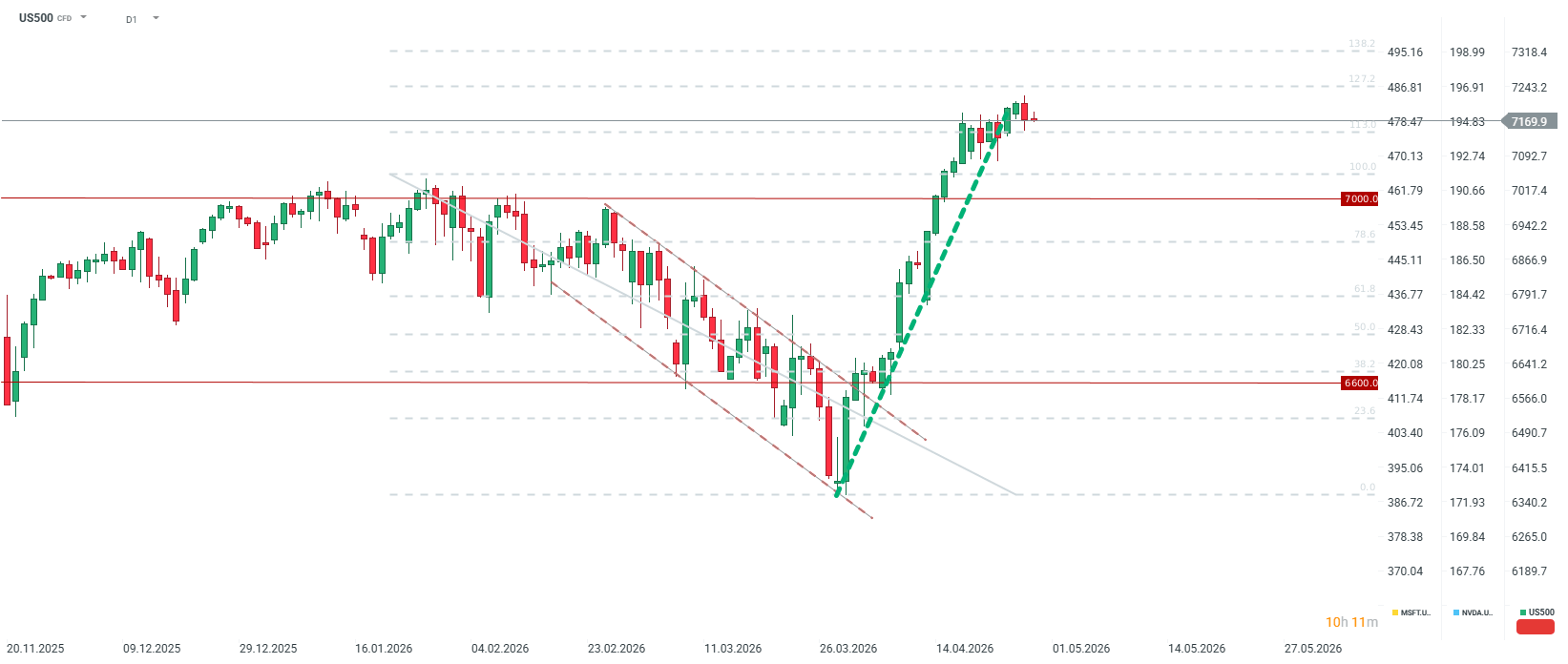

The US500 is undergoing a sharp correction during the April 28 session. Today, volatility will be fueled not only by the Fed's decision but also by US corporate earnings. After the Wall Street session today, we will see results from Microsoft, Alphabet, Amazon, and Meta. Disappointment in these results could send the S&P 500 index contract below the 7,000-point level, whereas showing a real, strong return on AI investment could send the US500 not only above 7,200 but toward the 7,300 area at the 138.2 retracement. Nevertheless, it must also be remembered that sentiment on Wall Street may still depend on what Donald Trump says, even though investors have been focused on the future for a month now. Source: xStation5

The US500 is undergoing a sharp correction during the April 28 session. Today, volatility will be fueled not only by the Fed's decision but also by US corporate earnings. After the Wall Street session today, we will see results from Microsoft, Alphabet, Amazon, and Meta. Disappointment in these results could send the S&P 500 index contract below the 7,000-point level, whereas showing a real, strong return on AI investment could send the US500 not only above 7,200 but toward the 7,300 area at the 138.2 retracement. Nevertheless, it must also be remembered that sentiment on Wall Street may still depend on what Donald Trump says, even though investors have been focused on the future for a month now. Source: xStation5

Did SaaS lost too much? Morgan Stanley says yes.

Red Sea, but not the indices : The effects of the Bab al-Mandab blockade.

Daily Summary: A sell-off with a spin-off

Iran Escalation: What to Watch and What to Expect

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.