Geopolitics and a heavy slate of event risks collide today, as investors grapple with rising geopolitical tensions, the June US CPI report, new Fed chair Kevin Warsh’s testimony to Congress, alongside some key banking earnings.

The oil price has risen another 3% this morning and is currently above $86 per barrel for Brent crude. It is higher by nearly 9% in the past 5 days and it does not look like the oil price rise will slow down any time soon. Risk aversion is high on Tuesday, and European stocks are lower, after US equities sunk at the start of the week, led lower by large declines for SanDisk, Marvell and Arm Holdings, and bond yields surged.

Time for the Nasdaq to recover?

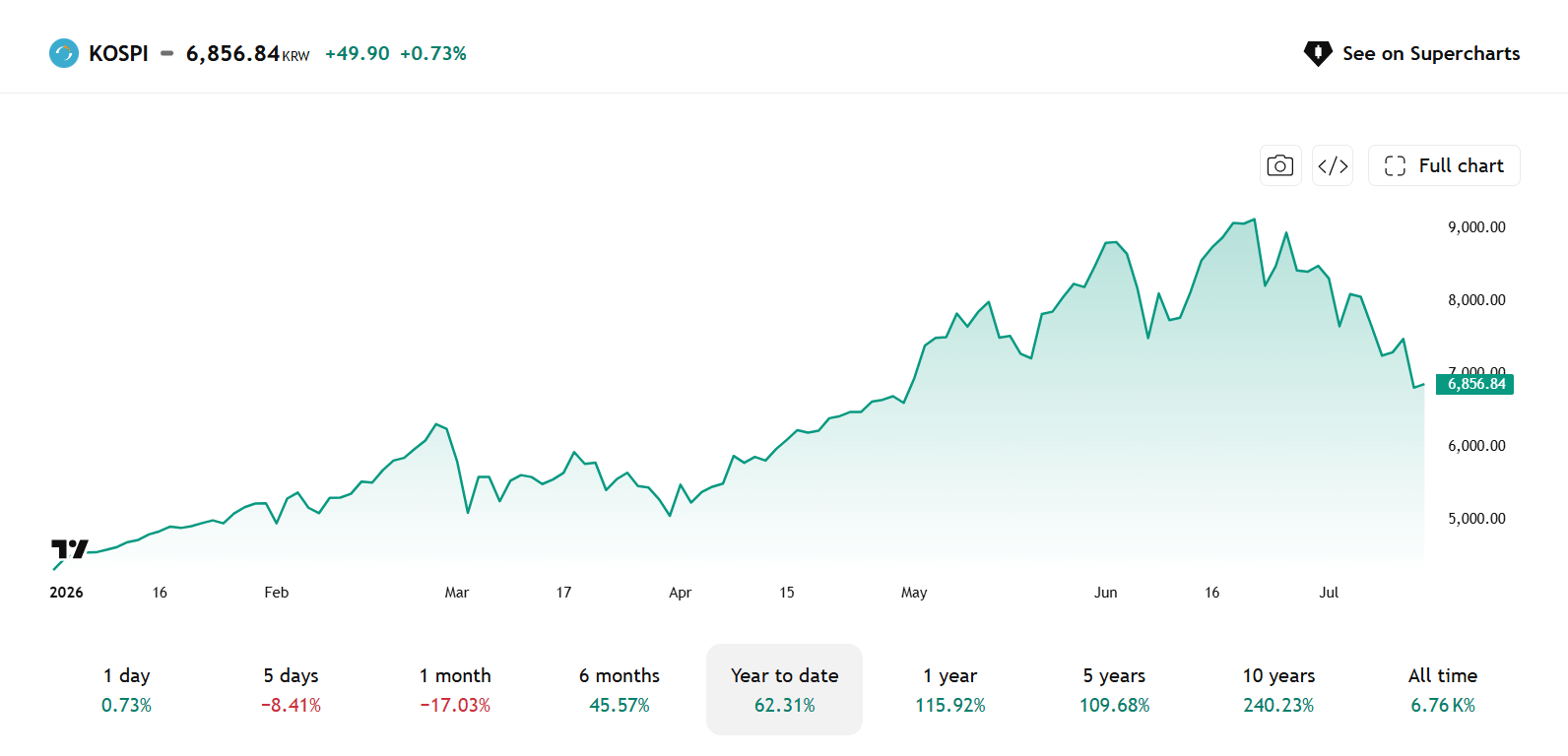

Interestingly, the Kospi and the Nikkei both posted gains overnight, and SK Hynix stabilized and rose by 3%, after suffering its steepest ever sell off on Monday. This is bolstering the chip trade across the Atlantic, and Nasdaq futures are pointing to a higher open later today. This suggests that the Nasdaq could break its short-term negative correlation with the oil price, and rise alongside energy prices if this continues.

More rate hikes expected

The energy price spike means that the market is also rushing to price in more interest rate hikes. There is now a full hike priced in from the BOE by year end. The market also sees the Fed hiking rates this year, there is a 40% chance of a hike at this month’s Fed meeting. The gold price is getting dragged lower by a rising dollar and rising bond yields, the yellow metal is now down for the 5th consecutive month and is 7% lower so far this year.

US/ Iran tensions enter Dangerous new territory

The latest news from the Middle East does not suggest that a quick resolution is available at this time, and so far, there has been no TACO from Trump. The US launched a third straight night of attacks on Iran, and Trump said the attacks would continue on Tuesday. The President also said that US forces would target Pickaxe Mountain, a fortified underground nuclear site. If this happens it would be a major escalation of the war that would suggest a new phase of attacks. It would also be another nail in the coffin for the peace process.

The new blockade starts today

From a market perspective, all eyes are on the Strait of Hormuz. The US will begin its naval blockade later today, and the President is apparently mulling a 20% toll on all cargo that traverses the Strait. The prospect of more fighting and a fresh blockade has meant that traffic through the Strait has slowed to a near halt. Only 6 cargo ships traversed the Strait on Sunday, which is a trickle compared to previous flows in recent weeks. When the supply chain gets gummed up, this is what keeps upward pressure on the oil price. It is worth noting that the last blockade lasted for more than 60 days.

Waller hints that Fed may raise rates in July

Another large rise in the oil price could see the price of crude march back towards $100 per barrel, which is a key concern for central bankers. There already seems to be a regime shift at the Fed, Kevin Warsh is more hawkish than expected. Now, FOMC governor Chris Waller, said that he would raise interest rates if today’s US CPI report comes in hot.

This had a damaging impact on chip stocks at the start of the week. This has been one of the most profitable trades this year, but as the macro environment shifts, profits are getting booked, and positions sold. While the market did not sell in May, July is proving to be too hot to handle for some traders.

Stocks to watch in the coming 24 hours include SK Hynix. After its sharp slide on the Nasdaq on Monday, it has stabilised on Tuesday as buyers are willing to buy the dip. The same could happen in the US, even if we expect chip stocks to remain bumpy in the coming days and weeks. After a volatile week for some sectors of the US market, especially tech, it makes sense for markets to take a breather here.

SpaceX is also worth watching, after its stock price plunged 4% on Monday. The stock is now trading below $140 per share, in the immediate aftermath of its IPO, the share price surged to $201. The company is still highly valued, but it has taken a knock, and if there are more declines on Tuesday, it could lead to the postponement of other AI IPOs like Anthropic and OpenAI.

What to watch today

1, US CPI

After comments from the Fed’s Chris Waller, a decision on whether to hike rates at the next FOMC meeting could hinge on this CPI report. CPI is expected to moderate to 3.9% from 4.2% last month, however, if it does not moderate at a fast enough pace, then near term rate hikes from the Fed are back on the table. Added to this, even if inflation does moderate to the 3.9% level, this is still well above the Fed’s target rate of 2%. Added to this, the oil price is surging once more, which means a June moderation in price pressures could be short lived.

Overall, it is very hard to see how this report can deliver a dovish surprise, unless it comes in well below expectations. The market is pricing in Fed rate hikes in the near term, and this could mean more weakness for stocks and government bonds if the inflation data points to more pressure ahead.

2, Warsh testimony

The Fed governor is preparing for his first ever Congressional testimony today. He is likely to stick to a similar message as Waller and say that inflation is too high and the Fed will act to get CPI back to the 2% target rate.

There is a chance that Waller may have stolen Warsh’s thunder, but we expect the sentiment from both men to be similar. This testimony is likely to show his true colours: is he a dove or a hawk? If Warsh puts the same amount of weight on the CPI report as Waller, then it could set the tone for the rest of the week. Risky assets may struggle and gold could sell off sharpy. It could be a double whammy of bad news for bond yields, which are already rising due to the increase in the oil price. It will also be worth watching out for Trump’s reaction if we get a hawkish Warsh later today.

3, Bank earnings

After repeated quarters of strong earnings growth, some analysts are worried that the bar is set too high for the major US banks this earnings season. While we expect banking results not remain resilient in Q2, the focus will shift to the outlook: what does net interest income look like, what does the M&A and IPO pipeline look like? The Q2 earnings reports could show how important the AI theme is to banking results these days. AI is likely to dominate M&A transactions, and the IPO market, with Anthropic set to list later this year. Anything that disrupts this pipeline of lucrative activity for the banks is a big risk for banking stocks.

The KBW banking index in the US has been more resilient than chip stocks and some big tech names during this period of volatility. It is higher by 5% in the past month, and 13% YTD. Thus, if banks can post another record quarter for earnings, this could help the rotation story, with investors reversing their chip and AI positions in favour of more traditional sectors in the US stock market like banks.

However, there is a longer term threat to banking stocks. AI is now an important customer for banks through M&A, IPO activity and lending. This means that a prolonged period of weakness for AI stocks and any scaling back in investment in AI could eventually tickly down and hurt the banks. Something to watch this earnings season.

Chart 1: South Korean Kospi takes a knock

Source: XTB

Stock of the Week: Arista Networks—A Second-Tier Technology with Top-Tier Results

📉 Natural gas tumbles as US EIA inventories rise

Oil climbs back above $80 per barrel 🔼

US Open: S&P 500 shows strength as semiconductor lags 🚩 Western Digital down 12%

This content has been created by XTB S.A. This service is provided by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, entered in the register of entrepreneurs of the National Court Register (Krajowy Rejestr Sądowy) conducted by District Court for the Capital City of Warsaw, XII Commercial Division of the National Court Register under KRS number 0000217580, REGON number 015803782 and Tax Identification Number (NIP) 527-24-43-955, with the fully paid up share capital in the amount of PLN 5.869.181,75. XTB S.A. conducts brokerage activities on the basis of the license granted by Polish Securities and Exchange Commission on 8th November 2005 No. DDM-M-4021-57-1/2005 and is supervised by Polish Supervision Authority.