The latest results from Alibaba (BABA.US) do not inspire optimism, and the market is reacting nervously (with share prices falling by 1–3%). Although the company is trying to argue that its huge expenditure on artificial intelligence (AI) will eventually pay off, the figures for the quarter ending in March 2026 paint a picture of stagnation. Revenue for the entire group grew by a mere 3%, falling short of analysts’ forecasts, and worse still, Alibaba recorded its first operating loss in five years (i.e. since the pandemic). This is a direct result of the drastic increase in spending on AI development and the aggressive battle for new users.

The main problem lies at the heart of Alibaba’s business, namely domestic e-commerce (Taobao/Tmall). This segment has been the biggest disappointment, growing only marginally. Chinese consumers seem to have ‘burned out’ – no one else in the world is bombarded with so many discounts and promotions, and China’s economy does not encourage the purchase of more expensive products, which is holding back growth in transaction values. At the other end of the spectrum is the Cloud Intelligence segment. Here, there is a light at the end of the tunnel: revenue from external customers jumped by 40%, and AI-related products already account for 30% of this figure. This shows that demand for AI services is real. Unfortunately, the dynamic cloud segment is still too small a part of the business to pull the entire, sluggish group along with it.

The long-term outlook raises concerns about the company’s financial health. Alibaba finds itself in a difficult predicament. Firstly, it is hard to make money from AI software in China, as companies there are not in the habit of paying for software as they are in the West – they need to be ‘educated’ and encouraged over a long period. Secondly, Alibaba is burning through cash at an alarming rate: negative free cash flow this quarter amounted to as much as $2.5 billion. This is due to a costly price war in fast e-commerce (e.g. Ele.me) and expenditure on promoting the Qwen AI app (the battle with ByteDance). As a result, investors are left with the same dividend and no news of a share buyback. At the moment, the market sees primarily rising costs, rather than the promised profits from the AI transformation.

RESULTS FOR THE FOURTH QUARTER

- Revenue: 243.38 billion yuan, +2.9% year-on-year, forecast: 246.51 billion yuan

- Alibaba International Digital Commerce Group revenue: 35.43 billion yuan, up 5.5% year-on-year; forecast: 35.93 billion yuan

- Cloud Intelligence Group’s revenue stood at 41.63 billion yuan, up 38% year-on-year, against a forecast of 41.44 billion yuan

- Revenue for the China E-commerce Business Group stood at 122.22 billion yuan, compared with a forecast of 126.03 billion yuan

- Adjusted earnings per American Depositary Receipt (ADR) stood at 62 cents, compared with 12.52 yuan year-on-year; the forecast was 6.04 yuan

- Adjusted EBITDA stood at 16.44 billion yuan, representing a 61% year-on-year decline; the forecast was 24.06 billion yuan

- Adjusted net profit stood at 86 million yuan, compared with 29.85 billion yuan year-on-year; the forecast was 15.08 billion yuan

- Revenue from other activities amounted to 65.46 billion yuan; the forecast was 64.61 billion yuan

The company has been recording a historical loss that has gone unnoticed for several quarters. Source: Bloomberg Financial Lp

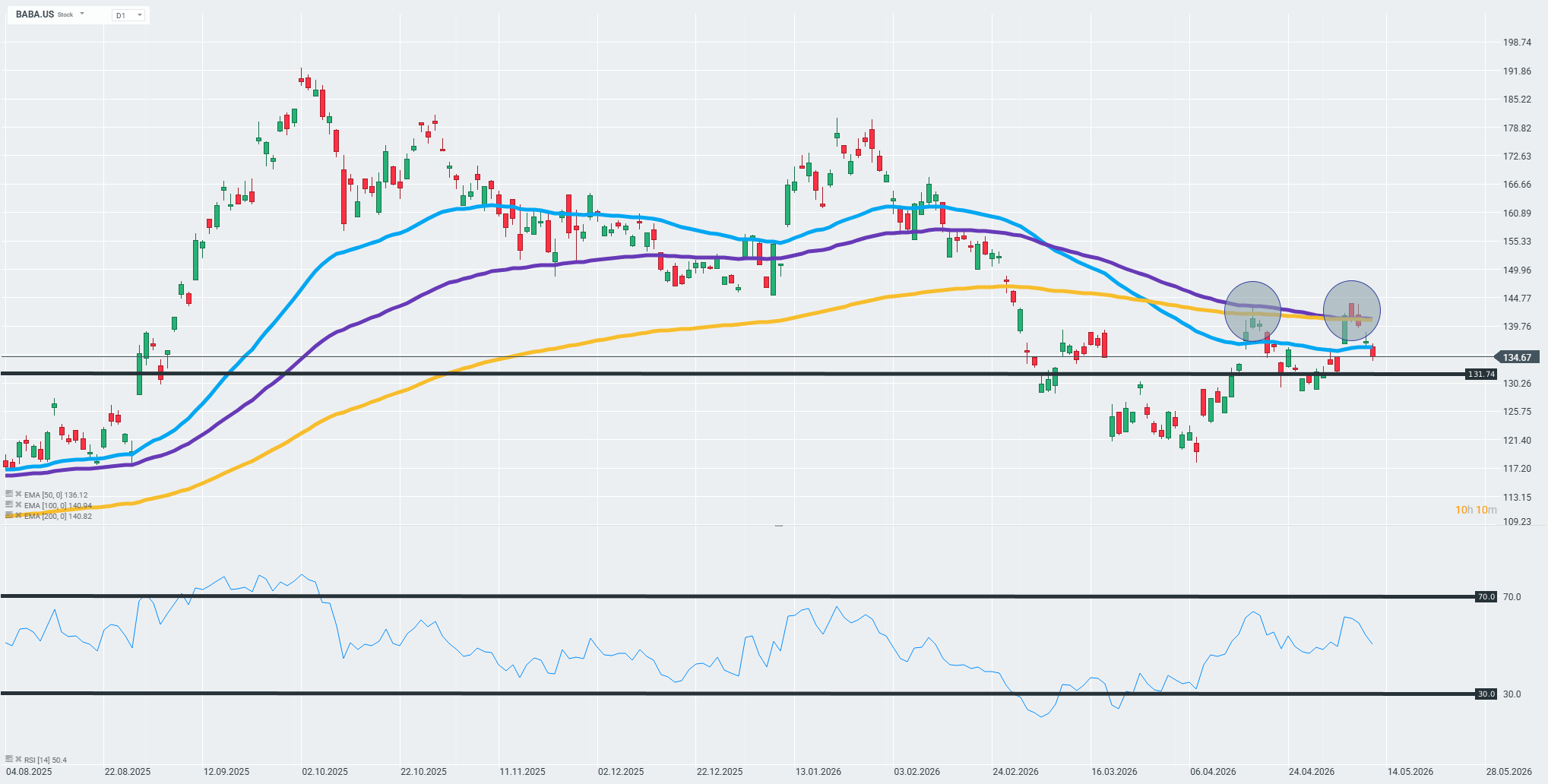

The daily chart for Alibaba (BABA.US) continues its long-term downtrend, remaining consistently below the key 200-day EMA. A local rebound was brutally halted in the ‘resistance zone’ (EMA 50 and 100), which pushed the price in pre-market trading straight down to the key support level at $131.74. Defending this horizontal level at the opening of the main session will be critical to avoiding a capitulation of demand and a test of the psychological barrier at $130. Source: xStation

SpaceX Preview: It's Time to See How Much of Its Valuation Is Based on Business and How Much on Promise

Economic Calendar: What Could Move the Market This Week? (03.08.2026)

Market Wrap: European equities at 3-week highs! Apple dips in US premarket!

Morning Wrap: AI Fuels the Rebound. Technology Makes a Strong Comeback

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.