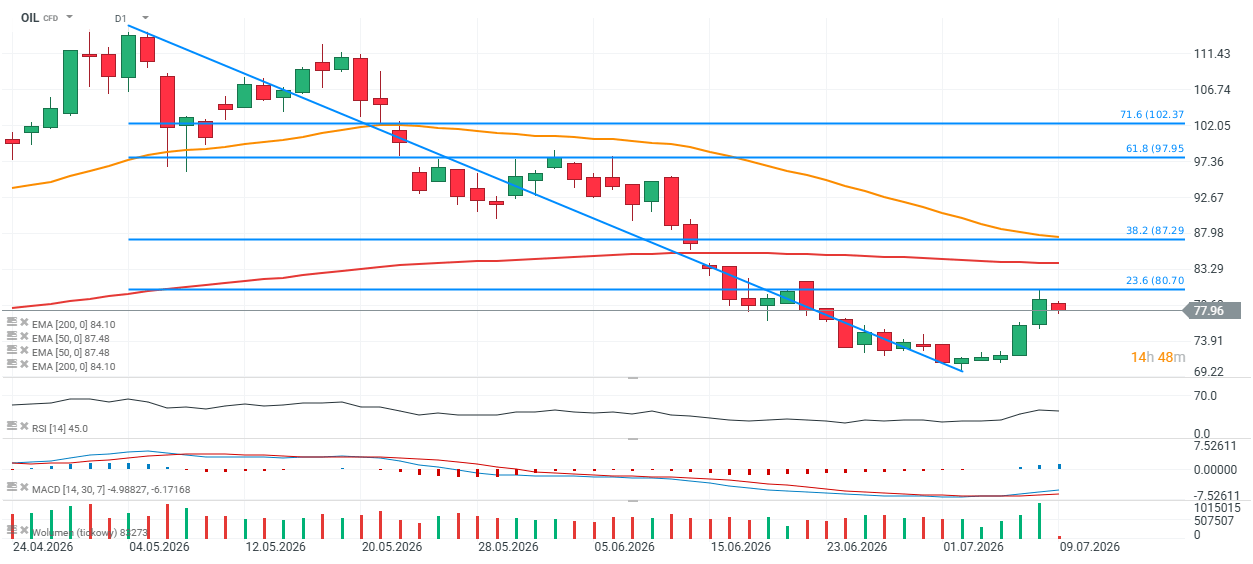

Brent crude (OIL) rallied on the back of the latest escalation in the Middle East, but despite strikes on Iranian military facilities and Tehran's retaliation against U.S. bases in the region, the oil market has remained relatively calm. The contract has rebounded more than 10% from its recent low, but the advance stalled almost precisely at the 23.6% Fibonacci retracement of this year's May decline, around USD 80.7 per barrel. From a technical perspective, this level could trigger another downward move, with the USD 73–75 area emerging as the next key support zone. On the other hand, a decisive breakout higher would increase the probability of a move toward USD 84–87 per barrel, where the 200-day exponential moving average (EMA200) and the 38.2% Fibonacci retracement converge.

OIL (D1 chart)

Source: xStation 5

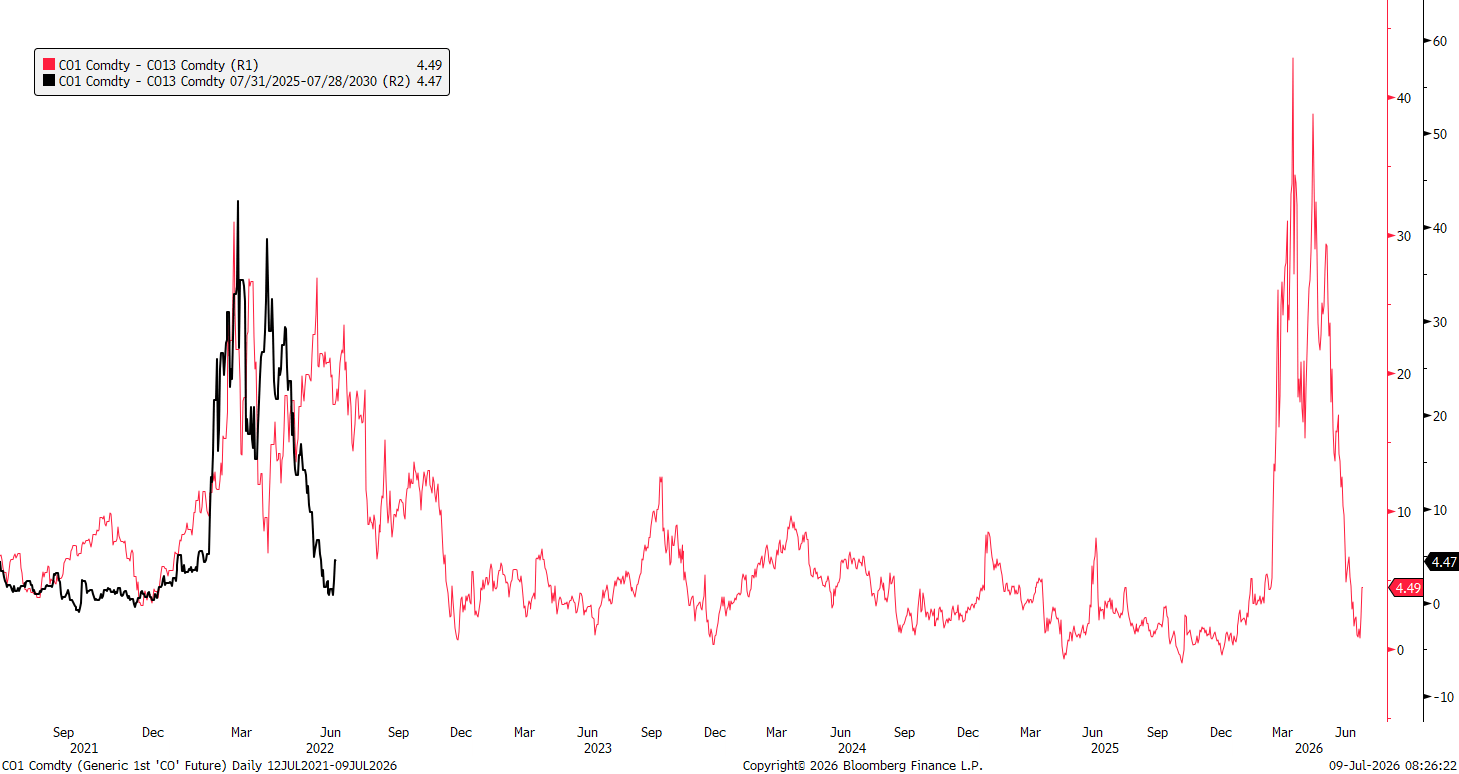

The chart below illustrates the Brent crude oil futures term structure, specifically the spread between the front-month futures contract (C01) and a much longer-dated contract (C013). The current spread of around USD 4.5 per barrel suggests that, despite a sharp decline from this year's highs, the market is still pricing in meaningful short-term supply tightness.

The red line represents the price difference between the front-month futures contract and the longer-dated contract. The current spread stands at approximately USD 4.49 per barrel. A positive spread means the front-month contract trades above the deferred contract, indicating a market in backwardation. This typically reflects tight physical supply or exceptionally strong near-term demand for crude oil.

The wider the spread, the larger the premium traders are willing to pay for immediate delivery. This explains the sharp spikes seen after Russia's invasion of Ukraine in 2022 and again during the escalation of geopolitical tensions involving Iran in 2026.

When the spread falls to zero or turns negative, the market shifts into contango, meaning longer-dated contracts trade above the front-month contract. Such a structure usually signals comfortable supply conditions, elevated inventories, or expectations of weaker demand. That is not the case at present.

Source: Bloomberg Finance L.P.

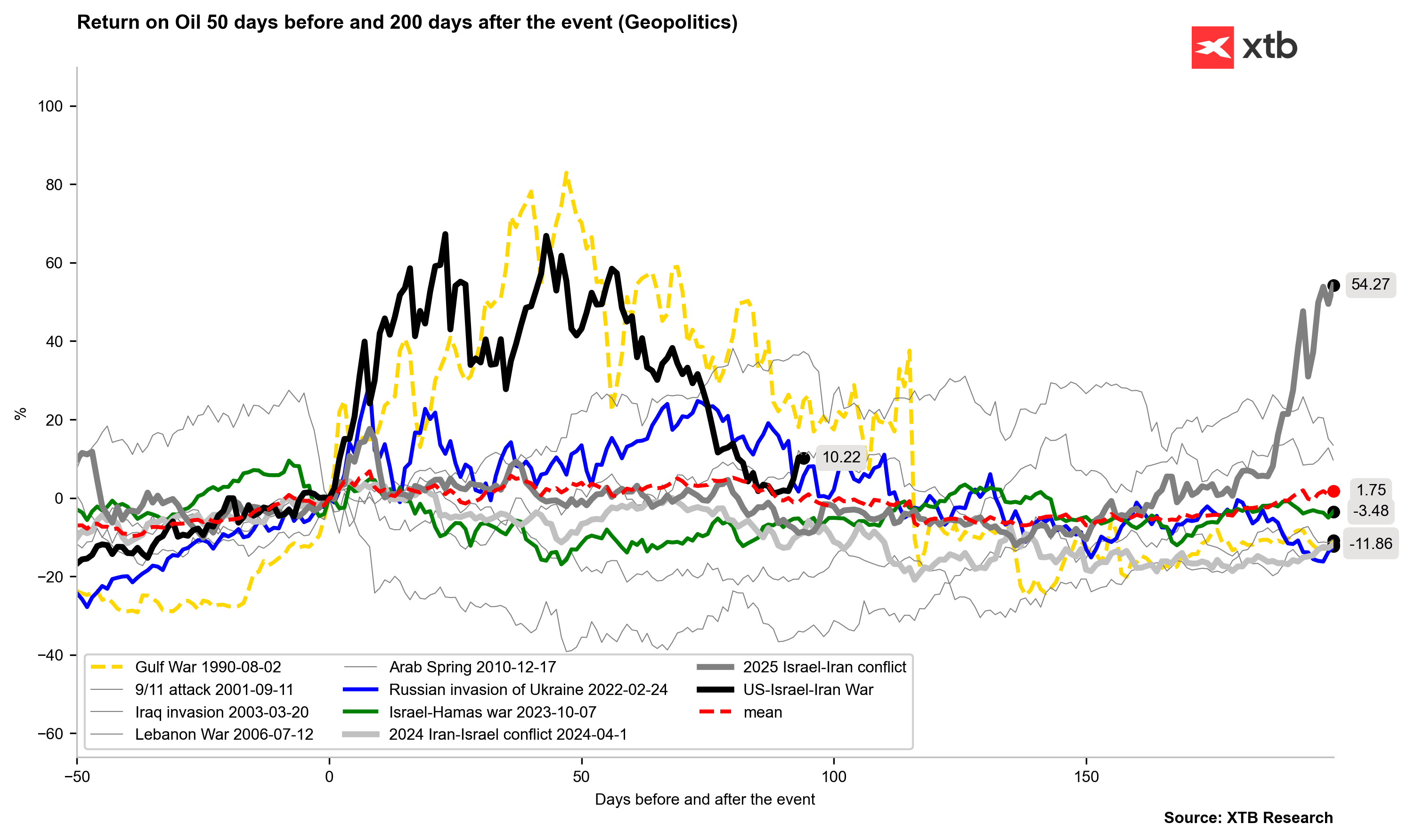

The chart compares Brent crude oil performance across major geopolitical events, showing returns from 50 days before to 200 days after each event. While some conflicts, such as the Gulf War and Russia's invasion of Ukraine, triggered prolonged oil rallies, many others resulted in only temporary price spikes that faded over time. The current Israel-Iran conflict has so far produced a moderate increase compared with previous major geopolitical shocks. On average, geopolitical events have generated only limited long-term gains in oil prices, as illustrated by the relatively flat mean return. This suggests that unless supply disruptions become prolonged, geopolitical risk alone is often insufficient to sustain a lasting bull market in crude oil.

Source: Bloomberg Finance L.P., XTB Research

Morning Wrap: Markets Are Trying to Rebound Following Big Tech Earnings and the Fed's Decision

Daily Summary - The market starts to doubt rate hikes after Warsh, but Trump destroys the rebound

Not so hawkish words, dovish dodges. EURUSD at 1.1450 during Kevin Warsh's Q&A

Fed Press Conference: Warsh Praises CapEx and Improves Market Sentiment

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.