The private credit market is off to a weak start to the year. After Blue Owl restricted withdrawals from one of its private credit funds a few weeks ago, the market began openly questioning the solvency and valuations of many funds.

This weekend, BlackRock joins the list of firms fueling investors’ concerns.

Source: Bloomberg Finance LP

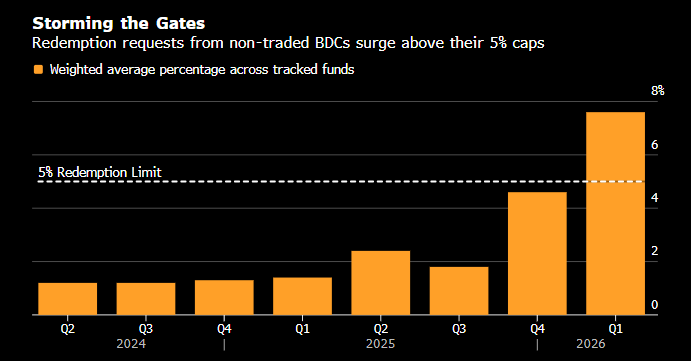

Capital outflows from the private credit market are reaching unprecedented levels. Given the nature of this market and its lack of liquidity, this puts funds in a difficult position.

Source: Bloomberg Finance LP

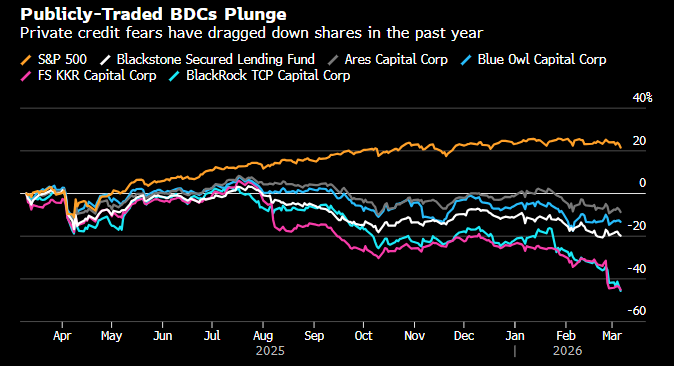

This difficult situation is also clearly reflected in valuations.

Companies such as BlackRock and Blue Owl are now paying the price for flaws in their own strategy. The idea behind the growth of private credit was to expand the offering to retail investors, but they have a very different risk profile and a much lower tolerance for having their capital locked up for the long term. Investors’ concerns are not unfounded either: the private credit market plays a fundamental role in financing the build-out of AI infrastructure, an area whose promised returns are increasingly being called into question.

What are funds hiding?

The lack of liquidity in the private credit market is not, in itself, a reason to panic. Illiquidity is a fundamental feature of this market, not something extraordinary. What could be a major problem, evoking memories of 2007, is that, according to a Bloomberg investigation, many funds and positions in the private credit market have greater exposure to the software sector than they report.

In practice, this means that many funds may be masking their full exposure to software in order to obtain financing without paying the appropriate risk premium. The very existence of such a premium—and evidence of attempts to conceal exposure to avoid it, suggests that the situation of tech companies and the private credit market may be worse than the financial metrics of many of these firms would imply.

BLK.US (D1)

Source: xStation5

While the problems in the private credit market will not disappear overnight, and may, over time, prove worse than expected, this does not change the fact that, as of today, the chart action looks more like an emotionally driven, temporary correction. An RSI around ~25 signaled a “bottom” in previous sell-off episodes.

Economic Calendar: JOLTS Report and Key U.S. Data Take Center Stage

Morning Wrap: Wall Street Returns to the Offensive as Palantir Fuels AI Optimism

Daily summary: Sense of relief to global markets🎢 OIL prices dip 8%🚨

SpaceX Preview: It's Time to See How Much of Its Valuation Is Based on Business and How Much on Promise

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.