Asian equity markets finished the quarter with strong gains, supported by improving sentiment on Wall Street, where semiconductor stocks once again led the advance. The MSCI Asia Pacific Index climbed nearly 1.5%, capping its strongest quarterly performance in almost 17 years. Optimism also spread to futures markets, pointing to further gains in both U.S. equities—after the Dow Jones Industrial Average closed at another record high on Monday—and European stocks.

Key highlights

- South Korea remained the world's best-performing major equity market this year, with the Kospi Index rising 2.9% during the session. AI-related semiconductor stocks continued to dominate the rally. Samsung gained more than 5%, lifting its year-to-date return above 100%, while SK Hynix finished the quarter with an extraordinary gain of nearly 240%.

- Currency markets focused on the Japanese yen, which weakened beyond 162 against the U.S. dollar, reaching its weakest level since 1986 and falling below levels that previously triggered official intervention in 2024.

- A weaker yen continues to support Japanese exporters and helps keep domestic equities near record highs, but it also raises import costs, weighs on household purchasing power, and increases political pressure on the government.

- Verbal intervention from Japanese officials, including Chief Cabinet Secretary Yoshimasa Kihara and Minister Katayama, failed to halt the currency's decline.

- Brent crude traded near $72.50 per barrel and remains on track for its largest quarterly decline since the pandemic. The market continues to react to higher oil flows through the Strait of Hormuz following progress in regional peace negotiations.

- Morgan Stanley added to the bearish outlook for crude, warning that the global oil market could face oversupply in the coming months.

- Bitcoin is edging lower and trading near $59,500, while gold has pulled back to around $3,980 per ounce and silver has slipped to just below $58 per ounce. Both precious metals and cryptocurrencies are under pressure today, as the U.S. dollar posts gains across the market.

- China's official manufacturing PMI in June rose to 50.3, beating both the previous reading of 50.1 and the market consensus of 50.0, indicating that the manufacturing sector remained in expansion territory. Meanwhile, the services PMI increased to 50.2 from 49.9, while the Composite PMI climbed to 50.6, pointing to continued, albeit moderate, improvement across the broader Chinese economy. Australia's private sector credit and housing credit data came in broadly in line with or slightly below market expectations.

- Today's key macroeconomic events for investors include Germany's inflation report at 1 PM GMT, followed by the U.S. JOLTS job openings data at 3 PM GMT PM and the Conference Board Consumer Confidence Index at 6 PM GMT. Investors will also closely watch speeches from ECB policymakers, with Philip Lane speaking at 12:30 PM GMT and Piero Cipollone at 1 PM GMT.

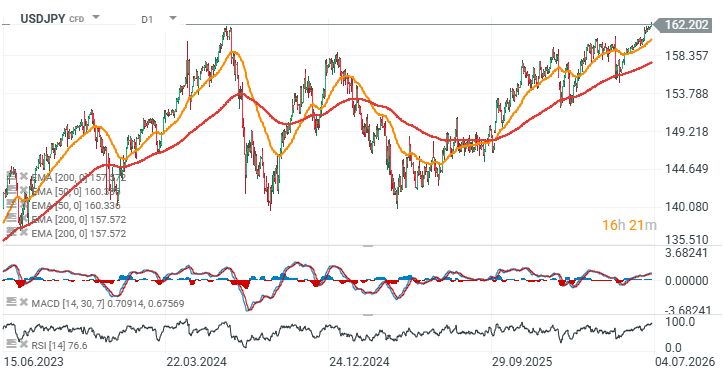

USDJPY Technical Outlook (D1, W1)

For several years, markets have anticipated a shift away from the Bank of Japan's ultra-dovish monetary policy. While the BoJ has implemented modest rate hikes, its overall stance remains highly accommodative. The central bank still shows little determination to meaningfully reduce bond purchases or aggressively tighten policy despite weakening economic conditions. A weaker yen continues to support Japan's export-driven economy and provides an important tailwind for the country's largest listed companies.

Source: xStation5

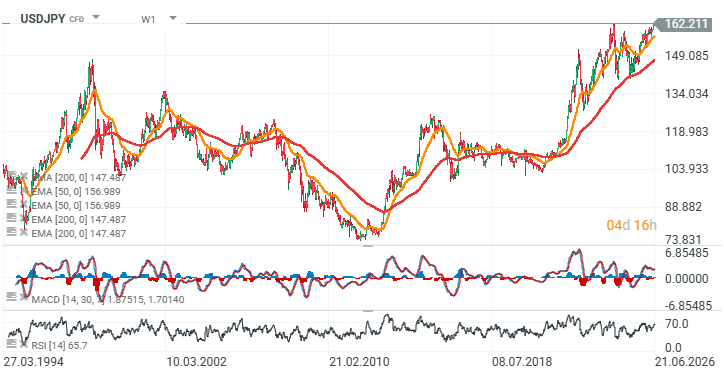

Although USD/JPY is trading close to multi-decade highs, the weekly RSI remains around 65, suggesting there is still room for further upside before technical conditions become overbought. In 2025, the pair successfully held support around the 200-week EMA near 147.5 before resuming its long-term uptrend. A decisive breakout above 163 could pave the way for another strong bullish impulse.

Source: xStation5

Oil Pulls Back After Strong Gains 🚩 Markets Assess the Strait of Hormuz Impasse

Market Wrap: Energy Leads Gains in Europe, ASML Rebounds 🔼 Alcon Rises 4% After Earnings

Will the Wall Street Rally Gain Momentum? 🗽 A Recap of the US Earnings Season

Chart of the Day: USDJPY Rises Again. Intervention Is Not Enough — Markets Await BoJ Action

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.